State of the Class B/C Multifamily Market in Central Florida

Focus geography: Orlando–Kissimmee–Sanford MSA / core Central Florida submarkets in Orange, Seminole, Osceola and Lake counties

Executive Summary

The Central Florida Class B/C apartment story is still attractive, but it is no longer a pure growth story. Over the last decade, the market benefited from strong in-migration, job growth, renter household formation and a widening affordability gap versus homeownership. That supported occupancy and rents across all vintages, with Class B/C generally outperforming Class A on occupancy because workforce renters had fewer alternatives.

The current market is in a late-supply-cycle reset. New deliveries have weighed on metro-wide occupancy and rent growth since 2023, especially in Class A lease-up product. Class B/C has held up better because it remains the relative-affordability option, but its cash flow is being pressured by three expense line items: insurance, property taxes and capital expenditures.

For the next 2–3 years, the setup looks better than the last 24 months. Construction starts are slowing, absorption is improving, and the market appears to be moving from oversupply toward balance. That should help stabilize Class B/C occupancy and return modest asking-rent growth. The main underwriting risk is not demand; it is expense growth and the ability to maintain collections from renters who are still highly payment-sensitive.

What "Class B/C" means in this market

In Central Florida, Class B/C usually means 1980s–2000s vintage garden product and older suburban assets serving workforce renters. These properties tend to compete on:

monthly affordability versus new Class A product

location near jobs, schools and transportation corridors

unit functionality rather than luxury amenity packages

operational execution, safety, cleanliness and resident service

This segment has been more resilient on occupancy than luxury product, but it also faces the heaviest burden from:

older roofs, plumbing, electrical and HVAC systems

rising insurance deductibles and tighter underwriting

reassessments after cap-rate compression and value growth

deferred maintenance and code/life-safety upgrades

Decade in review: 2015 to 2025

1) Occupancy

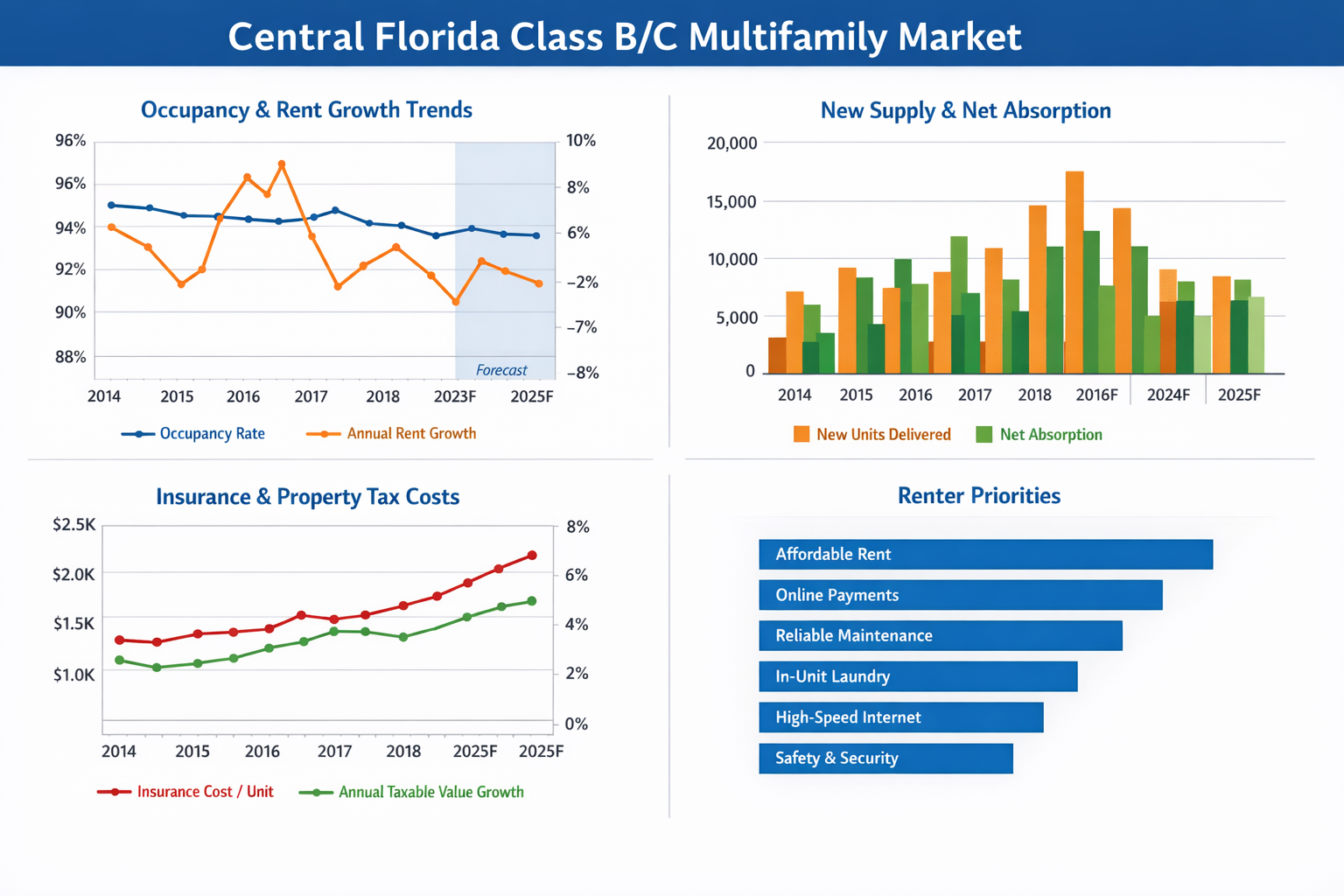

Over most of the last decade, Central Florida multifamily occupancy was healthy by national standards. The strongest period was the post-pandemic run-up in 2021–2022, when migration, wage growth and limited for-sale affordability tightened apartment demand.

The reset began in 2023 and continued through 2025 as a large wave of completions hit the Orlando metro. Metro-wide stabilized occupancy fell to the low-92% to low-93% range in 2025, the softest reading in years.

Important for Class B/C: lower-tier product still outperformed luxury. One useful benchmark from Berkadia: over the last 10 years, average Orlando Class C occupancy ran about 170 basis points above Class A. That is the core B/C thesis in Central Florida: when affordability is strained, older workforce product stays fuller.

2) Asking rents

The decade can be split into three phases:

2015–2019: steady, fundamentals-driven rent growth

2020–2022: accelerated rent growth during the migration and inflation boom

2023–2025: deceleration to flat or slightly negative growth because of supply pressure

By late 2025, most Orlando metro reports showed advertised/effective rents roughly flat to down modestly year over year. That reflects market-level averages; Class B/C generally held pricing better than top-of-market new product because it remained the affordable substitute.

3) Supply

Supply is the biggest reason fundamentals softened.

Central Florida was one of the nation’s most active multifamily development markets. Orlando ended 2025 with a very large pipeline still under construction, though materially below peak underway counts seen earlier in the cycle. Deliveries outpaced absorption for stretches in 2024–2025, which pushed concessions higher and pressured occupancies.

For B/C owners, the supply issue is indirect as much as direct. New Class A lease-ups often steal the top of the B renter pool through concessions. That creates a chain reaction: Class A competes with B, B competes with C, and operators across the stack become more aggressive on pricing and screening.

4) Absorption

Demand has been better than many feared. Central Florida continues to benefit from population growth, tourism, logistics, healthcare and broad service-sector employment.

Even during the recent soft patch, absorption remained solid enough to prevent a more severe correction. The market’s challenge was that demand was good while supply was extraordinary.

5) Debt terms over the decade

Debt has moved through three eras:

2015–2021: low-rate, high-liquidity period with aggressive leverage available

2022–2024: sharp rate shock, wider spreads, lower proceeds, higher DSCR sensitivity, floating-rate pain

2025–2026: improving but still disciplined lending environment

For B/C assets today, debt is available, but lenders are more conservative on:

insurance assumptions

replacement reserves

roof age and remaining useful life

T12 collections quality

delinquency and bad-debt trends

near-term tax reassessment risk

Current market snapshot: where Central Florida stands now

Occupancy

Central Florida occupancy looks close to a cyclical bottom rather than the start of a deeper deterioration. Market reports through late 2025 and early 2026 point to stabilization around the low-90s, with better performance in affordable/well-located workforce assets than in brand-new luxury product still fighting for lease-up.

B/C read-through: expect stronger physical occupancy than the market average, but often with more management friction, slower turns and tighter resident payment capacity.

Asking rents

Rents have reset from peak-growth years. Owners should not underwrite 2021–2022 style rent growth. The near-term story is stabilization, selective increases on renovated units, and better retention economics than aggressive mark-to-market pushes.

What is working in B/C:

smaller, frequent increases instead of large renewals

preserving occupancy and collections over headline asking-rent gains

using unit upgrades selectively where the rent premium is truly proven

Supply

Supply is still elevated, but the construction pipeline is now moving in the right direction. Starts have slowed because financing, insurance, labor and construction costs remain high. That matters because the market does not need demand to surge; it mainly needs the pipeline to normalize.

Absorption

Absorption should stay positive because Central Florida still attracts households priced out of homeownership and other higher-cost metros. Workforce demand is intact. The key operating issue is not whether there are renters; it is whether they qualify, pay on time and stay.

Forecast: next 2–3 years

Base case: 2026–2028

Occupancy

Likely path: gradual improvement from current levels as the delivery wave fades. Class B/C should continue to outperform Class A on occupancy because affordability remains the market’s defining theme.

Asking rents

Likely path: modest positive growth rather than another boom. Expect low-single-digit rent growth in better-located B product, with C product more dependent on collections discipline and submarket employment conditions.

Supply

Likely path: starts remain muted, completions roll down, lease-up pressure eases by late 2026 into 2027. This is the biggest support for the forecast.

Absorption

Likely path: steady. Migration may moderate from prior extremes, but the region still has enough demographic support to absorb normalized supply.

Debt terms

Likely path: better than 2023–2024, but not loose. More lender appetite should improve execution for agency and bank debt, yet underwriting will stay conservative because insurers and tax burdens remain volatile.

Practical debt expectations for B/C deals today

Typical financing themes for stabilized B/C assets in Florida:

lower leverage than peak-cycle lending

more stress on replacement reserves and capex escrows

stronger preference for fixed-rate agency executions on durable workforce deals

floating-rate debt usually reserved for high-conviction value-add with substantial liquidity support

wider lender differentiation based on roof age, claims history, flood/wind exposure, and sponsor insurance strategy

In plain English: debt is more available than it was in the freeze period, but it rewards clean stories. The clean story is: durable collections, low delinquency, no major deferred maintenance, recent roofs, proven insurance placement, and a credible tax posture.

Insurance market: property-level and portfolio-level

Florida insurance remains one of the biggest reasons Class B/C underwriting feels harder than the topline rent story would suggest.

Property-level insurance

The property-level market has improved from crisis conditions, but it is still expensive and underwriting-heavy. Owners of older Central Florida apartments continue to face scrutiny on:

roof age and type

prior claims history

plumbing and electrical systems

wind mitigation features

flood zone exposure and water intrusion history

update history by building and by line (roof/HVAC/plumbing/electrical)

What has changed: the state insurance market has shown signs of stabilization after reforms, and Citizens is moving back toward being an insurer of last resort rather than the dominant carrier. That is positive.

What has not changed enough: many apartment owners still face high premiums, higher deductibles, layered wind coverage, and greater demand for engineering reports and loss-control documentation.

For Class B/C, the gap between "insurable" and "financeable at acceptable economics" can be meaningful. A property may obtain coverage but at a deductible structure or premium load that destroys debt yield and cash flow.

Portfolio-level insurance

Portfolio strategies can still create value, but only when the schedule is curated.

Portfolio benefits may include:

more negotiating leverage with brokers/carriers

blending of stronger and weaker locations

centralized loss-control and maintenance reporting

captive or high-deductible strategy opportunities for sophisticated owners

Portfolio risks include:

one poor-loss property contaminating the entire schedule

concentration issues in wind-exposed counties

aggregate deductible exposure in storm years

lender-level complexity when different assets have different covenant packages

Insurance conclusions for B/C owners

The best operators in Central Florida are treating insurance as an operating discipline, not a once-a-year procurement event. Winning practices include:

pre-binding engineering and wind-mitigation review

roof replacement planning before renewal crises

standardized incident reporting and claim management

submetering / leak detection / shutoff controls where feasible

broker competition and early marketing of the account

very detailed property-condition records for older assets

Property taxes: trend and outlook

Property taxes have been a major NOI headwind.

The key pattern over the last decade has been:

values rose sharply during the 2021–2023 run-up

assessments followed with a lag

many buyers underwrote based on in-place taxes and then got hit by reset risk after acquisition

even where millage is flat or only modestly changed, taxable value growth still increases tax bills

That dynamic especially hurts B/C acquisitions bought for a value-add business plan, because the buyer can get hit three ways at once:

reassessment after sale

rising insurance

capex to keep the property insurable and competitive

Local tax trends in core Central Florida counties

Recent county-level tax-roll data show that taxable values are still growing in core Central Florida, even as the apartment market has cooled from its peak. Seminole County’s 2025 taxable value, for example, increased meaningfully year over year, and Orange County continues to publish annual tax roll growth and final millage schedules showing how tax burdens can rise even without a dramatic millage jump.

Bottom line: for apartment underwriting, assume tax pressure remains real. The tax issue is less about a sudden spike in nominal millage and more about steadily rising assessed values, especially after sale or major renovation.

What the state and local governments are doing

State of Florida

The state remains active on both insurance and property taxes.

Insurance

The 2022–2025 reform cycle was intended to stabilize Florida’s property insurance market through litigation, reinsurance, claims and Citizens-related changes. The latest official updates continue to frame the market as stabilizing, with Citizens shrinking and private market participation improving.

For apartment owners, that does not mean cheap insurance. It means the market is becoming more functional, but underwriting discipline remains strict.

Property taxes / multifamily-specific exemptions

Florida has expanded and clarified affordable-housing-related ad valorem exemptions for qualifying multifamily projects through Live Local and later bulletins/statutory changes. Those changes matter most for income-restricted or mixed-income deals that can qualify under the applicable affordability rules.

That is a real opportunity for workforce and missing-middle strategies, but it is not a universal solution for conventional B/C owners. Operators need property-tax counsel and appraiser-level review to determine whether any affordability component or land structure qualifies.

Local governments and municipalities

At the local level, Central Florida jurisdictions are mostly focused on:

affordable housing production and preservation

trust funds and local subsidy programs

zoning / land-use flexibility for housing supply

redevelopment in targeted corridors

Examples include Orange County’s Housing for All initiative and local housing action plans in Orlando and surrounding jurisdictions. These efforts are supportive of long-term rental demand and affordable housing production, but they do not remove the current expense pressure on conventional workforce assets.

The average renter in this market and what they want

There is no single renter profile, but the median Central Florida Class B/C renter is generally more payment-sensitive than the renter targeted by new luxury deliveries.

Typical characteristics of the workforce renter pool in this market:

higher sensitivity to total monthly housing cost than to amenity prestige

strong interest in convenience, safety and reliability

willingness to pay for practical features if they clearly improve daily life

less tolerance for surprise fees, poor maintenance response and friction in payments or move-in

The broader Orlando housing market also remains meaningfully cost-burdened, which explains why affordability and payment flexibility matter so much.

What renters say they prefer

Across current renter-preference surveys, the most durable priorities are practical rather than flashy:

in-unit laundry or laundry convenience

air conditioning and reliable HVAC

strong mobile/internet connectivity

transparent fees and pricing

easy online leasing and resident communication

digital rent payment options

secure package handling and access control

well-maintained parking and lighting

responsive maintenance

Surveys also continue to show strong renter interest in flexible payment options and a smoother digital experience.

How owners and developers can attract higher-quality residents and lower collection risk

The strongest playbook for Central Florida B/C is not "amenitize like Class A." It is "remove friction, improve trust, and protect the resident’s budget."

High-ROI resident strategy

1) Win on reliability, not luxury

For workforce renters, clean common areas, safety, HVAC reliability, quick work orders and pest control often matter more than a clubhouse refresh.

2) Keep fee structures simple

Hidden fees damage conversion and renewal. Transparent all-in pricing attracts better applicants and reduces payment disputes.

3) Offer flexible payments carefully

Split-payment options, early engagement before delinquency, and digital autopay tools can reduce collections friction when paired with disciplined underwriting.

4) Tighten screening without becoming too narrow

Best practice is layered screening:

income verification

employment durability

rent-to-income analysis

prior housing behavior

nuanced use of credit rather than blunt score cutoffs alone

5) Invest in resident communication

B/C collections performance improves when management communicates early, clearly and digitally. Missed payments are often preceded by resident disengagement.

6) Focus capex on the daily-use items

The best B/C renovation dollars often go to:

lighting and security cameras

parking and curb appeal

laundry, package and access solutions

kitchen and bath refreshes with durable finishes

low-maintenance flooring

leak detection and water management

7) Protect school and commute convenience

In suburban Central Florida, location near schools, service employment, logistics corridors, healthcare jobs and daily retail matters more than luxury branding.

What owners should do now

For lenders

Underwrite insurance with real quotes, not generic assumptions

Recast taxes to post-sale levels immediately

Stress collections, not just physical occupancy

Differentiate between true workforce assets and "old Class A with deferred maintenance"

Reward sponsors that show documented roof/plumbing/electrical plans

For investors

Prefer submarkets with durable workforce demand and less near-term Class A delivery pressure

Buy collections quality and expense control, not only headline occupancy

Treat insurance engineering and tax appeal work as part of the business plan

Underwrite slower rent growth but better long-run durability in Class B/C than in commodity Class A lease-up competition

For operators

Run renewals to maximize retention and collections, not sticker rent

Use selective upgrades instead of broad luxury repositioning

Rebid insurance early and prepare renewal documentation months ahead

Appeal taxes aggressively where reassessments outpace income reality

Track delinquency, NSF activity, skip risk and service-ticket response times as leading indicators

Overall conclusion

The Central Florida Class B/C multifamily market is not distressed; it is being repriced around a more realistic operating model.

Demand remains real. Occupancy in workforce housing should stay relatively resilient. Supply pressure is fading. Those are positives.

But the winning B/C strategy for the next 2–3 years is operational excellence, not aggressive rent growth. The owners who outperform will be the ones who control insurance, challenge taxes, preserve collections, and deliver a dependable resident experience at a monthly cost that still feels attainable.

That combination should produce better risk-adjusted performance than chasing luxury competition in a market that is still digesting new supply.

Research and articles used for this report

Cushman & Wakefield Orlando Multifamily MarketBeat Q4 2025

https://www.cushmanwakefield.com/en/united-states/insights/us-marketbeats/orlando-marketbeatsOrlando Multifamily MarketBeat PDF Q4 2025

https://assets.cushmanwakefield.com/-/media/cw/marketbeat-pdfs/2025/q4/us-reports/multifamily/orlando_americas_marketbeat_multifamily_q42025.pdfNorthmarq: Orlando Multifamily Transaction Activity Accelerates

https://www.northmarq.com/insights/insights/transaction-activity-accelerates-second-halfMarcus & Millichap / IPA Orlando 1Q 2026 Multifamily Market Report

https://www.institutionalpropertyadvisors.com/research/market-report/multifamily/orlando/orlando-2026-investment-forecast-ipa-multifamily-market-reportYardi Matrix Orlando Multifamily Market Report December 2025

https://www.yardimatrix.com/blog/orlando-multifamily-market-report/MMG Real Estate Advisors 2026 Orlando Forecast

https://mmgrea.com/2026-orlando-forecast/MMG Orlando Q2 2025 Market Report

https://mmgrea.com/orlando-q2-2025-market-report/Berkadia Mid-Year 2024 Orlando Multifamily Report

https://www.berkadia.com/research/berkadia-mid-year-2024-multifamily-report-orlando/HUD Comprehensive Housing Market Analysis: Orlando-Kissimmee-Sanford HMA

https://www.huduser.gov/portal/publications/pdf/OrlandoKissimmeeSanfordFL-CHMA-24.pdfHUD Housing Market Profile: Orlando-Kissimmee-Sanford, July 2024

https://www.huduser.gov/portal/periodicals/USHMC/reg/OrlandoKissimmeeSanfordFL-HMP-July24.pdfFlorida Department of Financial Services: Property Insurance Changes

https://myfloridacfo.com/division/ica/propertyinsurancechangesFlorida Office of Insurance Regulation: Property Insurance Market Update

https://floir.com/docs-sf/property-casualty-libraries/property-insurance-market-overview/insurance-update-may-2024.pdfFlorida Department of Revenue PTO Bulletin 25-13

https://www.floridarevenue.com/TaxLaw/Documents/PTO%20BUL%2025-13%20-%20Exemption%20for%20Affordable%20Housing%20on%20Governmental%20Property.pdfFlorida Department of Revenue PTO Bulletin 25-11

https://floridarevenue.com/TaxLaw/Documents/PTO%20BUL%2025-11%20-%20Affordable%20Housing%20Property%20Exemption%20Land%20Leased%20From%20a%20Housing%20Finance%20Authority%20and%20From%20a%20Nonprofit.pdfFlorida Senate SB 1350 (2026)

https://www.flsenate.gov/Session/Bill/2026/1350/Orange County Property Appraiser Tax Roll & Millage Rates

https://ocpaweb.ocpafl.org/faqcontent/Taxroll_InfoOrange County 2025 Tax Roll Certification

https://ocpaimages.ocpafl.org/api/Content/GetContentDynamicFile?contentFileID=416714Seminole County Property Appraiser Tax Roll Facts

https://www.scpafl.org/information/tax-rollCity of Orlando Budget Documents 2024-2025

https://www.orlando.gov/Our-Government/Records-and-Documents/Financial/Budget-Documents/2024-2025Orange County Housing for All

https://www.orangecountyfl.net/NeighborsHousing/HousingForAll.aspxOrange County Housing Trust Fund Plan 2026-2028

https://www.orangecountyfl.net/Portals/0/Resource%20Library/neighbors%20-%20housing/Housing%20Trust%20Fund%20Plan%202026-2028.pdfCity of Orlando 2025 Annual Action Plan Draft

https://www.orlando.gov/files/sharedassets/public/v/1/departments/housing/draft_city_of_orlando_2025_annual_action_plan.pdfApartments.com renter search survey Q4 2025

https://www.apartments.com/grow/learning-center/renter-search-survey-q4-2025Zillow Consumer Housing Trends Report 2025 – Renters

https://www.zillow.com/research/renters-housing-trends-report-2025-35647/RealPage rental trends and resident experience findings

https://www.realpage.com/news/realpage-releases-new-multifamily-rental-trends/NMHC / Grace Hill Renter Preferences Survey

https://www.nmhc.org/research-insight/research-report/nmhc-grace-hill-renter-preferences-survey-report/MetroPlan Orlando Regional Indicators Report 2025

https://metroplanorlando.gov/wp-content/uploads/CFMPOA-Regional-Indicators-Report-2025.pdfCity of Orlando Annual Action Plan 2023

https://www.orlando.gov/files/sharedassets/public/v/1/departments/housing/2023-annual-action-plan_final.pdf