Yield Maintenance: How to Estimate Costs

Yield maintenance is a prepayment penalty designed to protect lenders when borrowers pay off loans early, particularly in commercial real estate. It compensates for the lender's lost interest income by calculating the penalty based on the loan's original interest rate, current Treasury yields, and the remaining loan balance. Here’s a quick breakdown:

Key Components Needed:

Unpaid Principal Balance (UPB): The remaining loan amount.

Original Loan Interest Rate: The fixed rate agreed upon during loan origination.

Current Treasury Yield: The benchmark rate tied to the loan's remaining term.

Remaining Loan Term: Time left until loan maturity.

Present Value (PV): Discounted value of future loan payments.

Formula:

Yield Maintenance = PV × (Original Rate − Treasury Yield)

If the calculated penalty is below 1% of the UPB, a minimum penalty (often 1%) applies.

Example: For a $1M loan with a 5% rate, 60 months left, and a 3.6% Treasury yield:

Present Value ≈ $581,600

Rate Differential = 1.4%

Penalty = $8,143 (but subject to a $10,000 minimum floor).

Understanding these costs is critical for refinancing or property sales. Planning ahead - like timing prepayments during higher Treasury yields or negotiating favorable terms upfront - can help manage penalties effectively.

Transform Your Real Estate Strategy

Access expert financial analysis, custom models, and tailored insights to drive your commercial real estate success. Simplify decision-making with our flexible, scalable solutions.

Required Inputs for Calculating Yield Maintenance

To figure out a yield maintenance penalty, you'll need several critical pieces of information. These details are typically found in your loan documents, current loan statements, and publicly available Treasury data. Accurate inputs are essential because even small errors can throw off your calculations. Here's a breakdown of the key elements needed for an accurate calculation.

Unpaid Principal Balance and Remaining Loan Term

The unpaid principal balance (UPB) is the amount you still owe on your loan at the time of prepayment. This figure is usually listed on your current loan statement or can be obtained through a payoff quote request from your lender or Master Servicer [8][5]. This number forms the foundation for determining the lender’s potential loss of interest income.

The remaining loan term refers to the time left between your prepayment date and the original loan maturity date, typically measured in months. For example, if your loan matures in three years, your remaining term would be 36 months. This is important because the longer the remaining term, the greater the interest income the lender misses out on, which directly impacts the penalty amount [2]. You can find the maturity date in your original loan agreement.

Next, you’ll need to identify your loan’s interest rate and the applicable Treasury yield.

Original Loan Interest Rate and Current Treasury Yield

The original loan interest rate is the fixed interest rate you agreed to when you first took out the loan. This rate is detailed in your promissory note or loan agreement [2][1]. It’s crucial for calculating the interest rate differential - the difference between what the lender expected to earn and what they can now earn by reinvesting your prepayment at current market rates.

The current Treasury yield acts as the benchmark discount rate. You’ll need to match the Treasury security’s maturity as closely as possible to your loan’s remaining term [6][8]. For instance, if you have five years left on your loan, you would use the 5-year Treasury note yield. On February 4, 2026, the 5-year Treasury yield was 3.67%, the 7-year yield was 3.87%, and the 10-year yield stood at 4.09% [4]. You can find up-to-date Treasury yields on the U.S. Department of the Treasury’s official website [5].

It's also important to confirm the discount rate specified in your loan documents. While many agreements use straight Treasury yields, some lenders may add a spread - such as 50 basis points - on top of the Treasury rate, which can significantly increase your penalty [2]. Verifying these details ensures your calculations align with the terms of your loan.

Present Value of Remaining Loan Payments

The present value (PV) represents the current worth of all your future loan payments, discounted at the current Treasury yield. This calculation determines how much your lender would need to reinvest your prepayment to match the income stream they would have received if you had continued making payments until the loan matured.

The PV is a central component of the yield maintenance formula, ensuring the lender achieves the same financial outcome as if the loan had run its full term [10][3]. The formula for calculating the PV factor is: (1 - (1 + r)^-n/12) / r, where r is the Treasury yield and n is the number of remaining months [8][3].

The Yield Maintenance Formula

Understanding the Formula

The standard yield maintenance formula is expressed as: Yield Maintenance = Present Value of Remaining Payments × (Interest Rate − Treasury Yield)[1][3][4]. Each part of this equation plays a role in protecting the lender's expected return.

Here’s a breakdown of the terms:

Yield Maintenance (YM): This is the total prepayment penalty you’ll owe the lender [1].

Interest Rate (IR): This refers to the original fixed rate from your loan agreement - the return the lender anticipated over the full loan term [1][3].

Treasury Yield (TY): This represents the current rate on U.S. Treasury securities with a maturity that matches the remaining term of your loan [3][4]. It illustrates what the lender could earn by reinvesting your prepayment in today’s market.

The formula revolves around the rate differential - the difference between the lender’s agreed-upon return and what they can now earn. Yield maintenance ensures the lender receives the same yield they would have had if the loan reached its full term. When you prepay, the lender loses out on the higher interest income they were expecting. The penalty compensates for this loss by calculating the extra funds they need upfront to replicate that income at current, often lower, rates.

Here’s an important detail: if Treasury rates rise above your original loan rate, the differential becomes negative. In such cases, most loan agreements include a minimum penalty floor, often set at 1% of the remaining principal. This ensures a baseline penalty even when the calculated differential would otherwise favor the borrower [3]. Always review your loan documents for this provision, as it can override the formula’s calculated result.

Next, we’ll explore how to calculate the present value of future payments to estimate the penalty more accurately.

Calculating Present Value of Future Payments

The present value (PV) calculation quantifies the lender’s lost income in today’s dollars. It discounts the remaining loan payments using the current Treasury yield as the discount rate.

For interest-only loans, the PV factor formula is: $\frac{1-(1+r)^{-n/12}}{r}$, where:

r is the Treasury yield (expressed as a decimal).

n is the number of months left until the loan matures [1][3].

This formula accounts for the time value of money, ensuring the penalty reflects the lender’s lost earnings.

To match the Treasury yield with your loan’s remaining term, use the yield for the corresponding maturity period. For instance, if your loan has 36 months left, use the 3-year Treasury yield. If it’s 60 months, use the 5-year Treasury yield [3][11].

Some loan agreements may add complexity by requiring a Treasury yield plus a spread - for example, Treasury + 50 basis points - as the discount rate [2][7]. This adjustment can lower your penalty compared to using the flat Treasury yield. Be sure to check your loan documents for the exact discount rate methodology before performing any calculations.

How to Calculate Yield Maintenance: Step-by-Step

How to Calculate Yield Maintenance Penalty: 3-Step Process with Formula

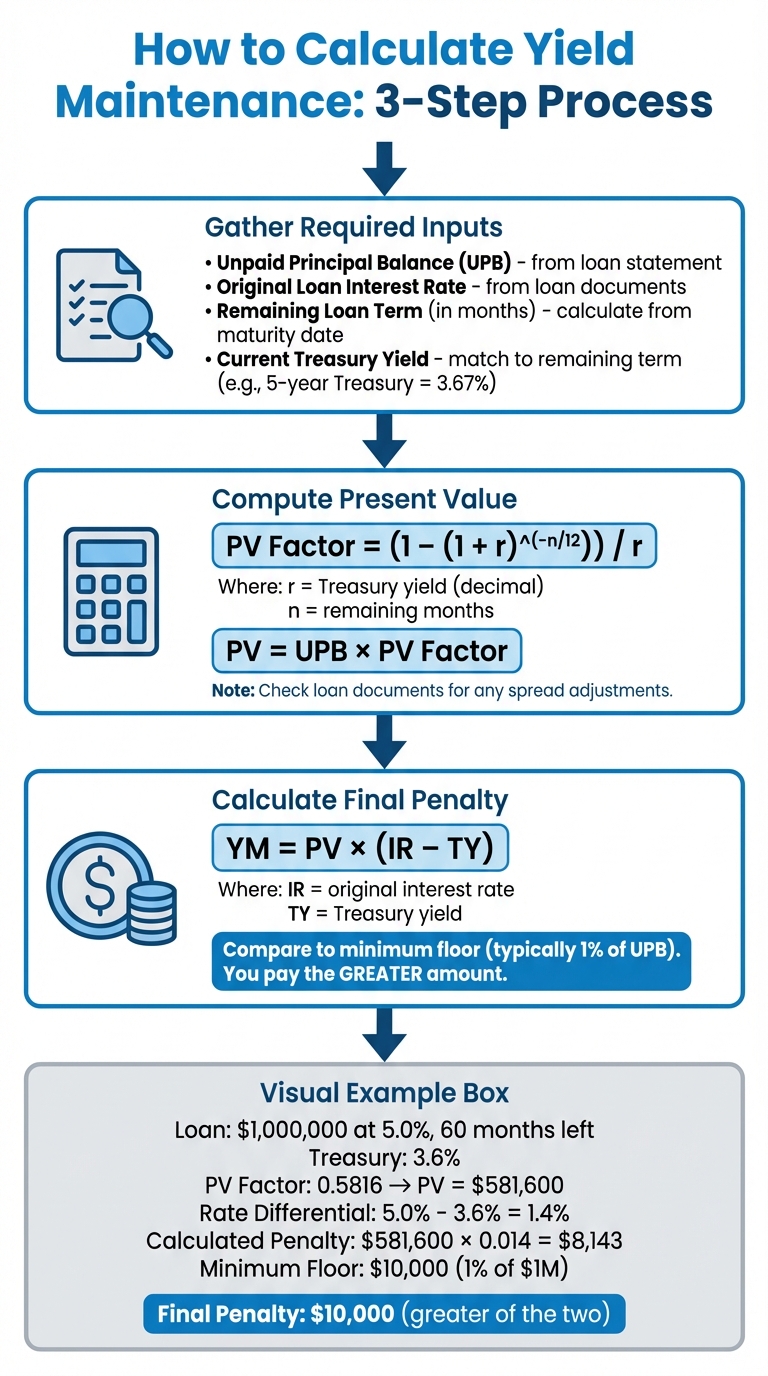

Step 1: Gather All Required Inputs

Start by collecting the necessary inputs:

Unpaid Principal Balance (UPB): You can find this on your loan statement or by requesting a payoff quote from your lender.

Original Loan Interest Rate: Check your loan documents for this information. For agency loans, refer to your loan agreement, such as Fannie Mae's Schedule 2 or Freddie Mac's Note, to confirm the yield maintenance terms [12].

Remaining Loan Term: Calculate the number of months left from your prepayment date to the loan's maturity date or the "YM Period End" date, if specified [8].

Current Treasury Yield: Match the Treasury yield to your remaining loan term. For example, as of February 4, 2026, the 5-year Treasury yield is 3.67%, and the 7-year Treasury yield is 3.87% [4]. For agency loans, the replacement Treasury rate is usually determined 25 business days before your prepayment date [12].

Once you've gathered these inputs, you'll be ready to calculate the present value.

Step 2: Compute Present Value of Remaining Payments

To calculate the present value (PV) of your remaining payments, use this formula:

PV Factor = (1 – (1 + r)^(-n/12)) / r

Here:

r is the Treasury yield expressed as a decimal.

n is the number of remaining months.

Multiply the PV factor by your unpaid principal balance to determine the present value of the remaining payments [1]. This step gives you the current value of your future loan payments, discounted at the current Treasury rate.

Check your loan documents to see if there’s any spread adjustment applied to the Treasury yield [2]. Once you have the present value, you can proceed to calculate the final penalty.

Step 3: Calculate the Rate Differential and Final Penalty

Using the present value from Step 2, calculate the penalty by determining the rate differential. Use the formula:

YM = PV × (IR − TY)

In this formula:

IR is your original loan interest rate.

TY is the current Treasury yield [1].

After calculating the penalty, compare it to the minimum floor, which is typically 1.00% of the outstanding principal balance [12]. Even if Treasury rates have risen above your original rate - resulting in a penalty calculation of zero or less - you’ll still owe the minimum 1% [3]. The actual prepayment penalty will be the greater of the calculated yield maintenance amount or the 1% floor.

Example Calculation

Loan Scenario

Imagine a commercial property loan with these details: a remaining unpaid principal balance of $1,000,000, an original interest rate of 5.0%, and 60 months (5 years) left on the term. The current 5-year Treasury yield is 3.6%, and you're considering a prepayment option that involves a yield maintenance penalty. This example reflects a common situation where interest rates have dropped since the loan's origination, leading to a penalty designed to offset the lender's potential loss in future income. Below is a step-by-step walkthrough of how to estimate that penalty.

Working Through the Calculation

Calculate the Present Value Factor

Start with the formula:

PV Factor = (1 – (1 + 0.036)^(-60/12)) / 0.036 Plugging in the numbers gives:

PV Factor ≈ 0.5816 Multiply this factor by the loan's unpaid balance to find the present value of future payments:

$1,000,000 × 0.5816 ≈ $581,600

Determine the Rate Differential

Subtract the current Treasury yield from the loan's original interest rate:

5.0% – 3.6% = 1.4% (or 0.014 in decimal form).

Calculate the Penalty

Multiply the present value by the rate differential:

$581,600 × 0.014 ≈ $8,143

Compare to the Minimum Floor Provision

Many loans include a minimum penalty floor, often 1% of the outstanding balance. In this case:

$1,000,000 × 0.01 = $10,000 Since the calculated penalty ($8,143) is less than the minimum floor ($10,000), the final yield maintenance charge is $10,000[3].

Considerations for Borrowers and Investors

Impact on Refinancing and Exit Strategies

Yield maintenance penalties can significantly influence decisions around refinancing and selling properties. When interest rates fall, lenders face larger potential losses, which directly increases the penalty amount. As Assets America explains:

The lower that interest rates fall, the larger the lender's loss, and therefore the higher the yield maintenance penalty [3].

This means that while lower interest rates might present appealing refinancing opportunities, they often come with higher penalties.

For property sales, yield maintenance can be more straightforward than defeasance. It allows for a true prepayment, leaving your property free of any financial encumbrances. By paying the penalty, you can fully close the loan and hand over a clean title to the buyer - a critical advantage when timing matters. For instance, in a Boulder, Colorado retail center case, an owner with a $15 million mortgage at 6% faced a $3.24 million yield maintenance penalty to refinance at 5%. This scenario required a careful analysis to determine if the 1% rate reduction justified the penalty cost [6].

These examples underscore the importance of finding effective ways to manage and reduce yield maintenance costs.

How to Reduce Yield Maintenance Costs

Reducing the expense of yield maintenance penalties requires strategic planning. Start by negotiating favorable terms during loan origination. For example, you could shorten the yield maintenance period or adjust the penalty structure. Many lenders also offer an "open window" - usually the final 120 days before the loan's maturity - allowing penalty-free prepayment [5].

Timing your prepayment strategically can also minimize costs. When Treasury yields rise or stabilize, the gap between rates narrows, which lowers the penalty. If you're selling, consider targeting buyers willing to assume the existing debt, allowing you to avoid the penalty altogether [3].

Another option is to negotiate a step-down penalty structure if you foresee an early exit. For instance, a sliding scale - starting at 5% in the first year and declining to 1% by the fifth year - offers predictable costs regardless of rate fluctuations [3][13]. This approach provides a clearer path compared to penalties tied to unpredictable market conditions.

Conclusion

Understanding yield maintenance costs is crucial for making informed choices about refinancing or selling a property. These costs essentially represent your exit price, influenced by current market conditions. As the AccountingInsights Team explains:

The penalty serves as a key factor in weighing the costs and benefits of early repayment... refinancing at a lower interest rate or reallocating capital to higher-yielding investments could offset the penalty [2].

The process involves comparing your loan's interest rate to current Treasury yields, which highlights how shifts in the market directly impact your exit costs. This makes accurate calculations absolutely essential.

While Master Servicers provide the final numbers, it's always wise to double-check the math yourself [9]. Even small discrepancies in discount rates or benchmark choices can lead to significant differences in what you ultimately owe.

Securing better terms at the start of your loan - like shorter yield maintenance periods or step-down structures - can give you more flexibility when it comes time to exit [14]. Additionally, timing your prepayment during periods of higher Treasury yields or offering loan assumptions to buyers can help reduce or even avoid penalties [3].

If you're looking for additional guidance, The Fractional Analyst (https://thefractionalanalyst.com) offers resources like underwriting support, asset management advice, and free financial models to help you navigate prepayment decisions effectively.

FAQs

-

When determining yield maintenance, it's important to match your loan's remaining term with the corresponding Treasury yield. For instance, if your loan has three years left, use the 3-year Treasury rate. This method follows standard practices and helps provide a precise estimate of potential costs.

-

Yield maintenance is commonly associated with interest-only loans. It serves as a way to compensate lenders for the loss of interest income if a borrower pays off the loan early. This is particularly relevant for loans where the borrower makes regular interest payments without reducing the principal.

-

To manage and potentially lower yield maintenance costs, consider negotiating prepayment terms like yield maintenance, defeasance, or step-down provisions. These agreements outline how prepayment penalties are calculated and can provide greater flexibility, depending on your financial goals.