U.S. Multifamily Real Estate in 2026 and Beyond: An Investor Guide to Cycles, Strategy, and Opportunity

Introduction: A Market Reset, Not a Collapse

The U.S. multifamily real estate sector is undergoing one of the most misunderstood transitions in modern market history. Headlines often frame the current environment as one of weakness—rising concessions, muted rent growth, and capital market dislocation. But beneath the surface, the data tells a far more nuanced and ultimately bullish story.

The sector is finding its footing, moving through a late-cycle reset into an early-stage expansion phase. In this environment, success is no longer driven by cheap capital or rapid rent appreciation. Instead, it is driven by disciplined underwriting, operational execution, and—above all—basis.

This article provides a comprehensive, deep dive into the current state and future trajectory of multifamily real estate in the United States, designed for investors, operators, and decision-makers.

Table of Contents

The Evolution of Multifamily Cycles

2026 Market Overview: Where We Stand Today

Supply Shock: The Largest Delivery Wave in Decades

Demand Drivers: Why Renters Aren’t Going Anywhere

Regional Divergence: Winners and Losers by Market

Capital Markets & Debt Dynamics

Rent Growth Forecasts and NOI Implications

The 5-Year Investment Thesis (2026–2031)

High-Conviction Investment Strategies

Risks Every Investor Must Underwrite

Multifamily vs. Other Asset Classes

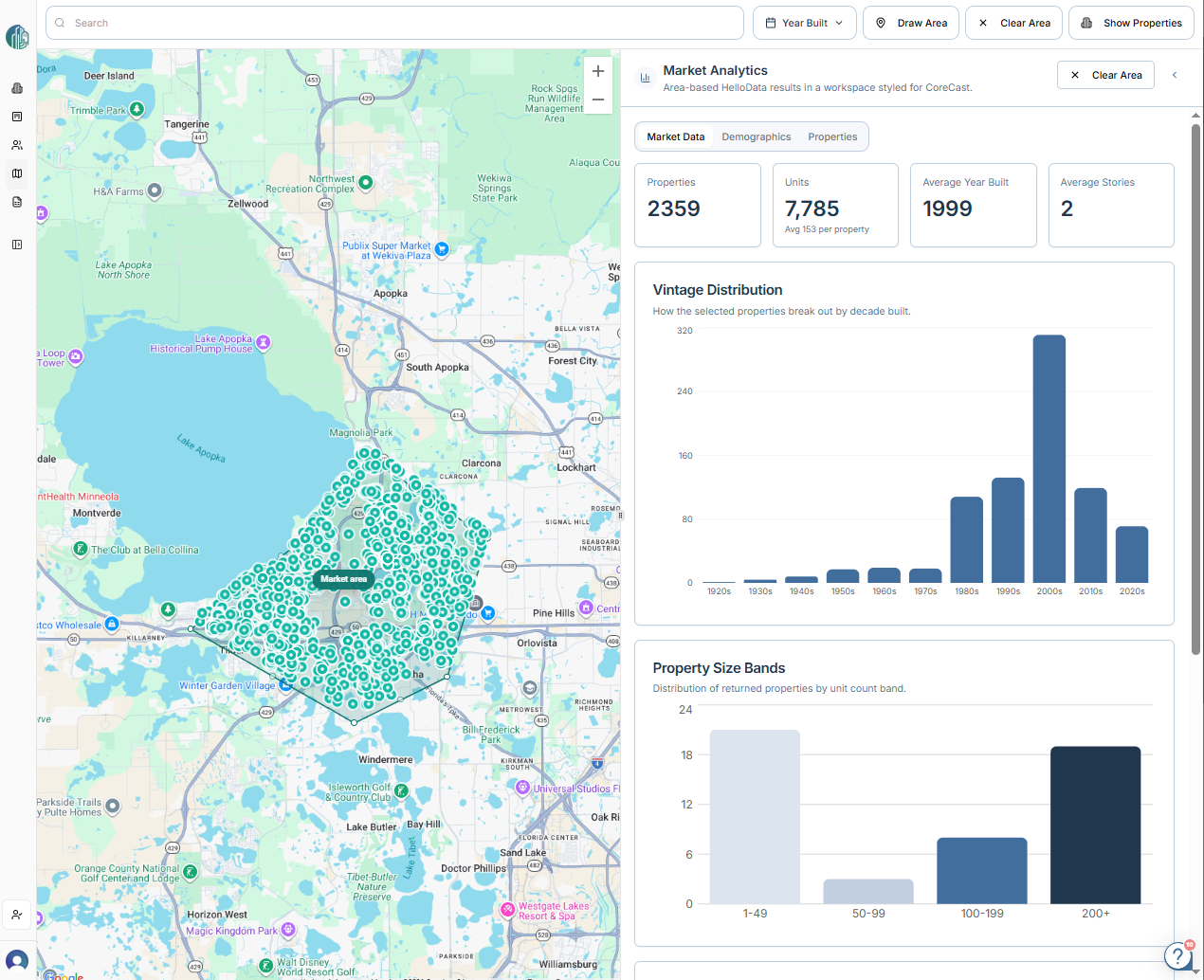

How Technology Is Changing Multifamily Investing

The Role of Platforms Like CoreCast and Fractional Analysts

Conclusion: The Next Golden Window

1. The Evolution of Multifamily Cycles

To understand where multifamily is headed, it’s critical to understand where it has been.

The Liquidity Era (2015–2019)

This period was defined by:

Historically low interest rates

Aggressive lending environments

Cap rate compression

Rapid rent growth driven by pandemic migration

Capital—not operations—drove returns.

The Correction Phase (2020–2025)

The market shifted dramatically due to:

Interest rate hikes

Financing constraints

Declining transaction volume

Negative leverage in many deals

This phase exposed weak underwriting and overleveraged capital stacks.

The Reset & Repricing Phase (2025–2027)

We are now here.

Key characteristics include:

Cap rates expanding but stabilizing

Increased transaction activity from distressed sellers

Focus on operational efficiency

The Next Expansion (2027+)

As supply declines and rent growth returns, multifamily enters a new expansion cycle—but with more disciplined fundamentals.

2. 2026 Market Overview: Where We Stand Today

The current multifamily market is defined by contradiction:

Occupancy remains relatively high

Absorption is still positive

Yet rent growth is muted

This dynamic reflects a supply-driven slowdown—not a demand collapse.

Key Takeaways

Multifamily fundamentals remain resilient

Short-term NOI pressure is real

Long-term demand drivers remain intact

The most important takeaway: this is not 2008. There is no systemic demand collapse—only temporary oversupply.

3. Supply Shock: The Largest Delivery Wave in 40+ Years

One of the defining features of the current cycle is an unprecedented supply surge.

The Numbers

Peak deliveries: ~690,000 units in 2024

Delivery window: 2024–2026

Largest supply wave in over four decades

Impact on the Market

This surge has led to:

Rent stagnation or declines in oversupplied markets

Increased concessions (free rent, discounts)

Elevated lease-up risk for new developments

Why This Happened

Low interest rates incentivized development starts in 2020–2022

Pandemic migration fueled optimistic demand assumptions

Construction pipelines lagged demand signals

The Key Insight

Supply shocks are temporary—but their effects create opportunity.

4. Demand Drivers: Why Renters Aren’t Going Anywhere

Despite short-term headwinds, the demand side of the equation remains structurally strong.

1. Homeownership Affordability Crisis

Rising mortgage rates and home prices have pushed ownership out of reach for many Americans.

Result: renters stay renters longer.

2. Demographic Tailwinds

Millennials are in peak renting years

Gen Z is entering the rental market

This creates a sustained demand floor for multifamily housing.

3. Household Formation

Even in a high-rate environment, household formation remains positive.

4. Migration Patterns

Population shifts continue to reshape demand across regions, creating localized opportunities.

5. Regional Divergence: Winners and Losers by Market

Perhaps the most important theme in multifamily today is regional divergence.

Oversupplied Markets (Short-Term Weakness)

These markets experienced aggressive development pipelines:

Austin

Phoenix

Dallas

Denver

Las Vegas

Drivers of weakness include:

Overbuilding

Pandemic-era migration overshoot

Slowing inbound demand

Supply-Constrained Markets (Outperformers)

These markets benefit from limited new construction:

New York City

Chicago

Midwest metros (Indianapolis, Columbus, Minneapolis)

Northeast secondary markets

Emerging Secondary Winners

Kansas City

Raleigh

Salt Lake City

Boise

These markets offer:

Lower supply pipelines

Affordability-driven migration

Growing job bases

Key Strategic Insight

Not all multifamily is equal. Market selection is now more important than asset selection.

6. Capital Markets & Debt Dynamics

The capital markets environment is one of the most critical factors shaping investment strategy.

The Debt Maturity Wall

~$875 billion in CRE loans maturing by year-end 2026

This creates significant pressure across the market.

Lending Environment

Banks are pulling back

Private credit is filling the gap

Debt is more expensive and less available

What This Means for Investors

Increased distress

More recapitalization opportunities

Greater negotiating power for buyers

"Extend and Pretend" vs. Forced Sales

Lenders are:

Extending loans in some cases

Forcing recapitalizations in others

Selling discounted notes when necessary

Transform Your Real Estate Strategy

Access expert financial analysis, custom models, and tailored insights to drive your commercial real estate success. Simplify decision-making with our flexible, scalable solutions.

7. Rent Growth Forecasts and NOI Implications

Short-Term Outlook

2026: ~0.5% rent growth

2027: ~1% rent growth

Medium-Term Outlook

2028+: 2–3% rent growth as supply clears

Implications for NOI

Near-term compression

Mid-term expansion

Investor Interpretation

This is a timing arbitrage opportunity:

Buy when NOI is weak → benefit when NOI recovers.

8. The 5-Year Investment Thesis (2026–2031)

The next five years can be broken into three distinct phases.

Phase 1: Dislocation (2025–2027)

Distress increases

Pricing dislocates

Best buying opportunities emerge

Target:

10–30% discounts to replacement cost fileciteturn0file0

Phase 2: Recovery (2027–2029)

Supply declines

Rent growth accelerates

NOI expands

Phase 3: Stabilization & Exit (2029–2031)

Cap rates compress

Institutional capital returns

Exit window opens

9. High-Conviction Investment Strategies

1. Basis-Driven Investing

The most important principle in today’s market:

Basis is everything.

Investors should:

Buy below replacement cost

Avoid overpaying for stabilized assets

2. Distressed Opportunities

Focus on:

Overleveraged sponsors

Broken capital stacks

Loan sales

3. Sun Belt Repricing Plays

Markets like Austin and Phoenix offer long-term upside—but only at discounted entry points.

4. Midwest & Northeast Overweight

These regions offer:

Stronger rent growth potential

Limited supply

5. Workforce Housing Focus

1–2 star assets outperforming

Less competition from new supply

6. Preferred Equity & Mezzanine Debt

Provides:

Higher yields

Better downside protection

7. Office-to-Multifamily Conversions

90,000+ units in pipeline

10. Risks Every Investor Must Underwrite

1. Prolonged High Interest Rates

Delays recovery

Pressures valuations

2. Policy Risk

Rent control

Zoning changes

3. Consumer Weakness

Wage stagnation limits rent growth

11. Multifamily vs. Other Asset Classes

Compared to office and retail, multifamily remains:

More stable

More liquid

More institutionally favored

Unlike office, multifamily demand is not structurally impaired.

12. How Technology Is Changing Multifamily Investing

Modern multifamily investing increasingly relies on data-driven decision-making.

Key trends include:

Real-time rent analytics

Predictive occupancy modeling

Automated underwriting tools

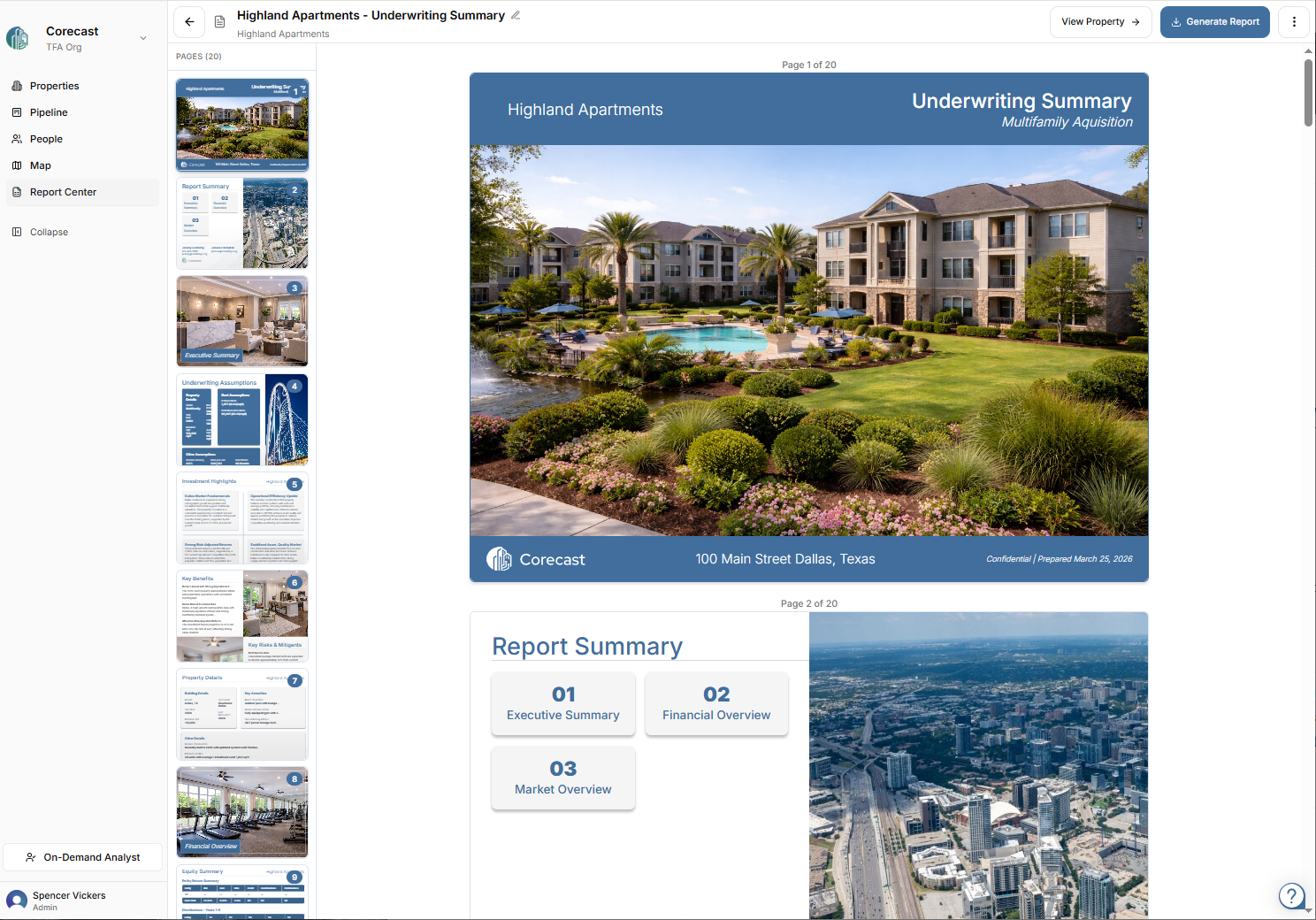

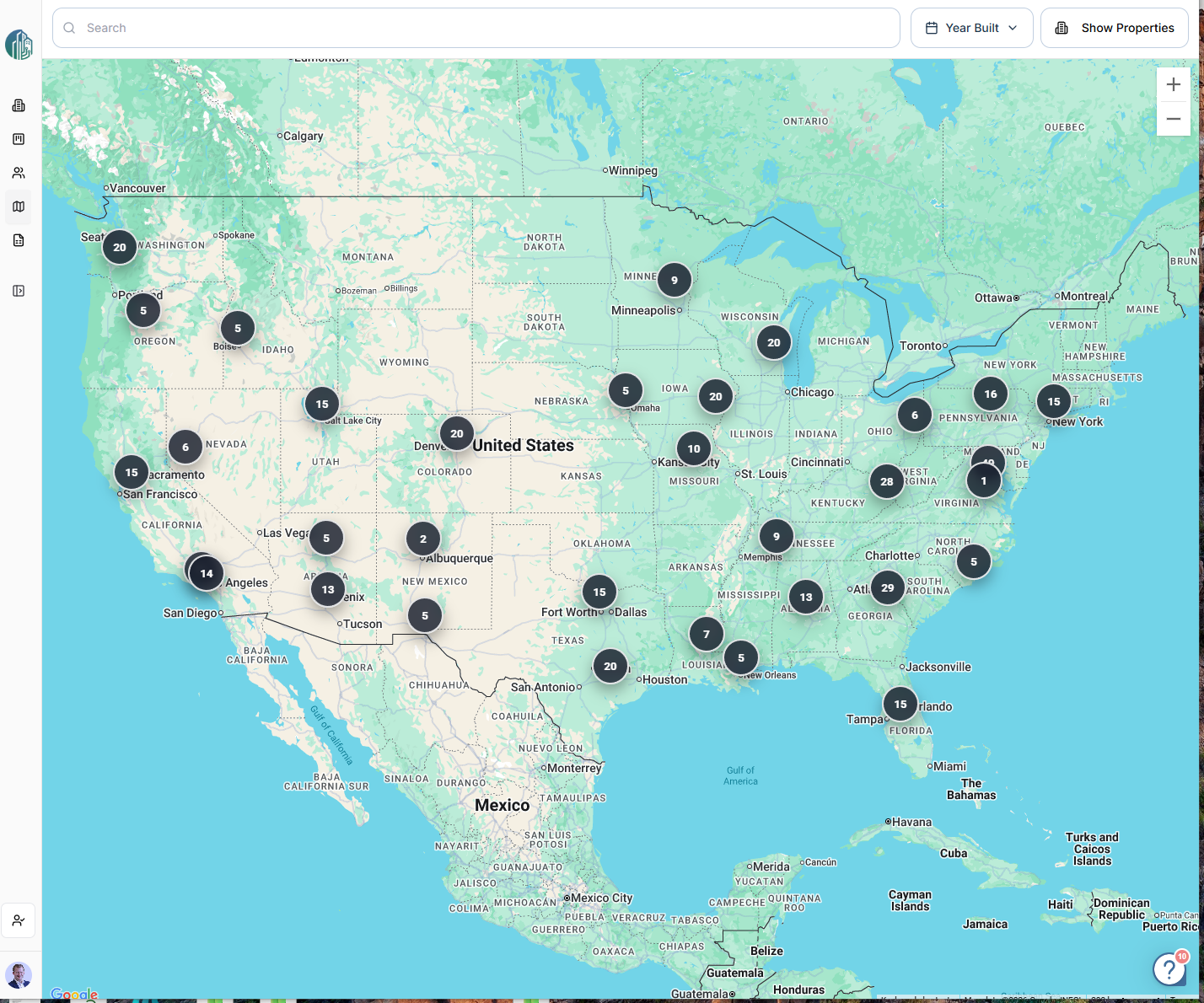

13. The Role of Platforms Like CoreCast and TFA

As markets become more complex, investors are turning to hybrid models that combine human expertise with technology.

Direct Servicing (TFA)

On-demand underwriting

Market research

Deal support

Self-Servicing (CoreCast Platform)

Scalable analytics

Faster decision-making

Standardized insights

These models enable investors to operate more efficiently in a margin-compressed environment.

14. Conclusion: The Next Golden Window

Multifamily real estate is not broken—it is repricing.

Short-term challenges include:

Supply glut

NOI pressure

But long-term fundamentals remain intact:

Structural housing shortage

Strong demographic demand

The next 24 months represent one of the most compelling buying windows since the post-GFC era.

Final Takeaway

Be aggressive—but selective

Prioritize basis over yield

Think in cycles, not headlines

Looking to navigate the multifamily market with institutional-grade insights?

Explore how The Fractional Analyst can support your investment strategy through on-demand expertise or leverage CoreCast to scale your underwriting process.

Sources

Yardi Matrix – U.S. Multifamily Market Report

https://www.yardimatrix.com/publications/us-multifamily-market-reportCBRE – U.S. Multifamily Figures & Forecast

https://www.cbre.com/insights/books/us-real-estate-market-outlook/multifamilyJLL – U.S. Multifamily Outlook

https://www.us.jll.com/en/trends-and-insights/research/multifamily-market-reportMarcus & Millichap – Multifamily Investment Forecast

https://www.marcusmillichap.com/research/market-forecastFreddie Mac – Multifamily Outlook

https://www.freddiemac.com/research/multifamilyFannie Mae – Multifamily Economic & Market Commentary

https://www.fanniemae.com/research-and-insightsNational Multifamily Housing Council (NMHC) – Industry Data & Research

https://www.nmhc.org/research-insightU.S. Census Bureau – Housing & Construction Data

https://www.census.gov/construction/nrc/index.htmlBureau of Labor Statistics (BLS) – Inflation & Wage Data

https://www.bls.govMoody’s Analytics – CRE & Multifamily Research

https://www.economy.comPwC & Urban Land Institute – Emerging Trends in Real Estate

https://www.pwc.com/us/en/industries/asset-wealth-management/real-estate/emerging-trends-in-real-estate.htmlMBA (Mortgage Bankers Association) – Commercial Real Estate Finance Outlook

https://www.mba.org/news-and-research/research-and-economics