Debt Due Diligence: Loan Covenant Checklist

Loan covenants are critical rules in commercial real estate loans that protect lenders and guide borrowers. They can require specific actions (affirmative covenants) or restrict certain activities (negative covenants). Breaking these rules, even unintentionally, can trigger a technical default, leading to serious consequences like higher interest rates or foreclosure.

Here’s what you need to know:

- 20%-30% of companies breach loan covenants, often unknowingly.

- Financial metrics like DSCR (Debt Service Coverage Ratio) and LTV (Loan-to-Value) are common monitoring tools.

- Missing deadlines for reports or failing to maintain insurance can cause defaults.

- Borrowers must carefully track compliance to avoid penalties and maintain lender trust.

The solution? A structured approach to covenant management. This includes organizing loan documents, analyzing covenant terms, and using tools like CoreCast for automated tracking or expert support from The Fractional Analyst. These steps reduce risks and ensure smoother lender relations.

Debt Covenants Explained: Lender Protections in Loan Agreements | Credit Analysis

sbb-itb-df8a938

Categories of Loan Covenants

Commercial real estate loan agreements often include three main categories of covenants designed to protect lenders. These are financial covenants, operational covenants, and collateral/negative covenants. Each type serves a distinct purpose: financial covenants set measurable benchmarks to assess the borrower's ability to manage debt, operational covenants focus on property management and reporting requirements, and collateral/negative covenants impose restrictions to safeguard the lender's security interest. Let’s break these down further.

Financial Covenants

Financial covenants are all about numbers. They set measurable standards to monitor the borrower's financial health and act as early warning systems for potential issues.

One of the most common metrics is the Debt Service Coverage Ratio (DSCR). This ratio measures whether the property's net operating income (NOI) is sufficient to cover its debt payments. For example, a DSCR of 1.25 means the property generates $1.25 in NOI for every $1.00 in debt service. Lenders typically require a DSCR between 1.20 and 1.40, with 1.25 being a standard benchmark [1]. This helps lenders detect financial trouble before it escalates into a default.

Another key metric is the Loan-to-Value (LTV) ratio, which limits the loan amount relative to the property's appraised value. Generally, lenders prefer an LTV of 80% or less, while anything above 95% is usually unacceptable [1]. These thresholds can vary depending on the property type. For instance, multifamily properties might qualify for an LTV of 75% to 80%, whereas hospitality assets often have stricter limits, typically between 55% and 65%.

Lenders may also impose guarantor requirements, mandating that borrowers maintain a net worth equal to or greater than the loan amount. Additionally, borrowers might need to hold liquidity - such as cash or marketable securities - equal to at least 10% of the loan value [1].

Operational Covenants

Operational covenants focus on the daily management of the property and regular reporting to the lender. One critical requirement is consistent reporting, which often includes submitting rent rolls, tax returns, and financial statements on a quarterly or annual basis. Missing these deadlines can result in a technical default, which carries penalties similar to missing a loan payment. For example, in the financing of the Greenbrook Village Center project by Bluegrass Capital Partners, the lender required quarterly financial statements to closely monitor the property's performance [1].

Borrowers are also required to maintain adequate insurance coverage, such as property, liability, and casualty insurance, with the lender named as the loss payee. Additionally, compliance with property tax obligations, zoning laws, and other regulations is mandatory. Borrowers may even need to prove that no significant adverse changes have occurred in the property's operations or financial condition.

Collateral and Negative Covenants

Collateral and negative covenants are designed to restrict actions that could increase the lender's risk or weaken their security interest in the property.

A common restriction involves incurring additional debt. Borrowers are generally prohibited from taking on new secured or subordinated debt without the lender's written consent. For example, a similar restriction prevented a borrower from acquiring additional secured debt, ensuring the lender maintained its first-position priority [1]. This type of covenant helps avoid situations like the infamous J. Crew case, where transferring intellectual property to secure new debt led to the company's financial collapse and inspired "J. Crew blocker" covenants [1].

Other restrictions include limits on asset transfers and ownership changes. Borrowers typically cannot sell, lease, or transfer core collateral without lender approval. Similarly, changes to the ownership structure of the borrowing entity are often tightly controlled. The Serta Simmons Bedding case highlights the risks of violating such provisions. The company engaged in an "uptier" debt restructuring that prioritized certain lenders over others, a move later ruled as a breach of its credit agreement by the U.S. Court of Appeals for the Fifth Circuit [1].

Negative covenants may also cap dividend distributions and capital expenditures. By limiting dividend payments, lenders ensure there’s enough cash flow to cover debt obligations. Similarly, restricting large capital expenditures prevents the borrower from making significant purchases that could strain liquidity or alter the property's risk profile.

Loan Covenant Review Checklist

5-Step Loan Covenant Review Process for Commercial Real Estate

Follow these structured steps to thoroughly review loan covenants.

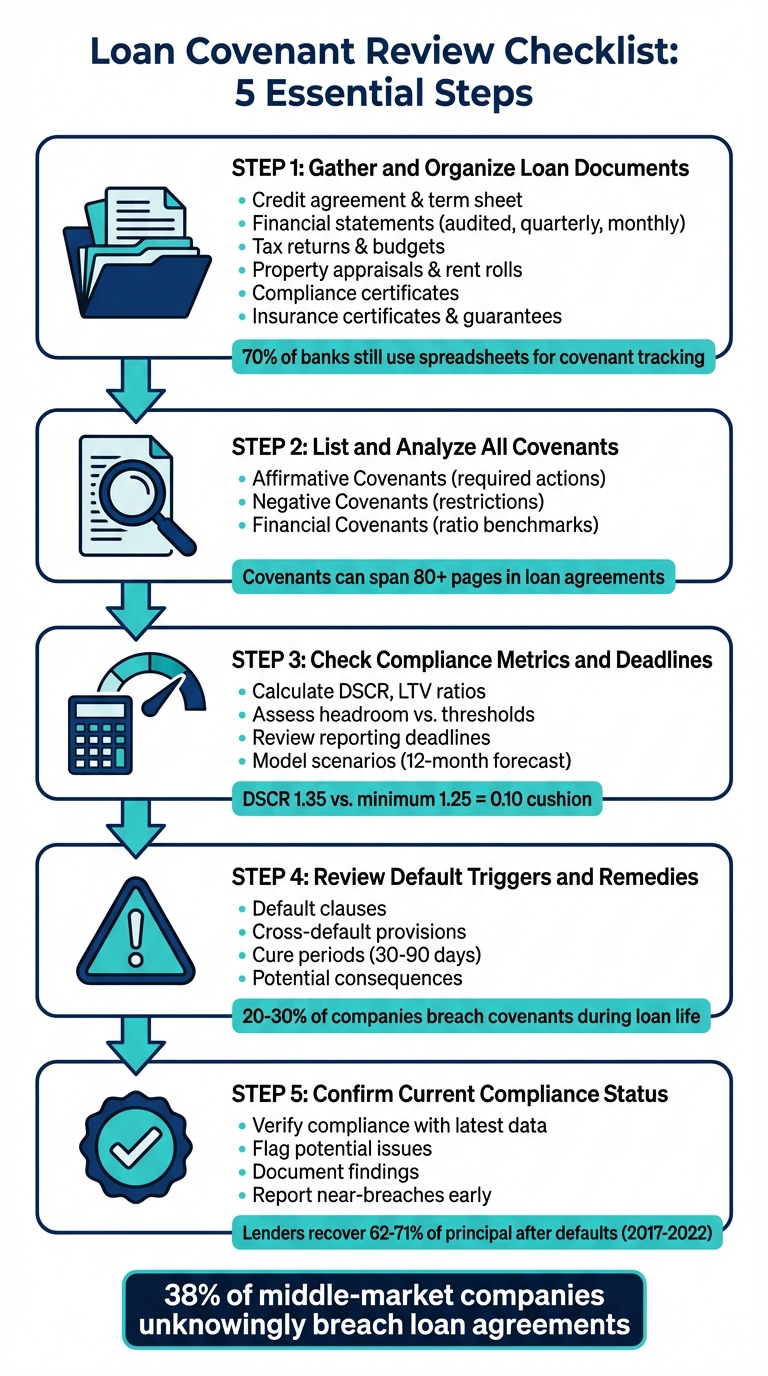

Step 1: Gather and Organize Loan Documents

Start by collecting all essential loan-related documents. Key agreements include the credit agreement (or loan contract), the term sheet, and any amendments or waivers. Financial records like audited, quarterly, and monthly financial statements - such as balance sheets, income statements, and cash flow statements - are equally important. Don’t forget tax returns and internal budgets or projections.

You’ll also need collateral and operational documents, such as property appraisals, rent rolls, and borrowing base certificates. Compliance and monitoring records, like previously submitted compliance certificates, covenant registers, and property monitoring reports, are critical for a complete picture. Lastly, gather legal documents, including personal or corporate guarantees, insurance certificates, and intercreditor agreements if multiple lenders are involved.

"The cornerstone of effective debt management is the consistent monitoring of loan covenants." - Laura Pop-Badiu, Senior Creative Writer, CommercialEdge

Surprisingly, nearly 70% of banks still rely on spreadsheets and manual tracking for loan covenants, increasing the likelihood of missed deadlines or thresholds. A centralized, well-organized repository of all these documents can help avoid such risks. Once everything is in place, you’re ready to list and analyze the covenants.

Step 2: List and Analyze All Covenants

Go through the loan agreement thoroughly. Covenants are usually detailed in the "terms and conditions" section, which can span over 80 pages and may be scattered throughout the document. To simplify, create a covenant register summarizing each facility or bond agreement, tracking definitions, thresholds, test dates, and exceptions.

Covenants generally fall into three categories:

- Affirmative Covenants: Actions the borrower is required to take, such as maintaining insurance or submitting financial statements.

- Negative Covenants: Restrictions on actions like taking on additional debt or selling assets without lender approval.

- Financial Covenants: Ratio-based benchmarks such as Debt Service Coverage Ratio (DSCR) or Loan-to-Value (LTV).

Pay close attention to how key terms like "EBITDA" or "Net Debt" are defined, as they often include specific adjustments. Look out for springing provisions that activate under certain conditions, such as deteriorating credit metrics or drawing down a specific portion of a credit line. Also, distinguish between maintenance covenants (tested periodically) and incurrence covenants (tested only when specific actions are taken, like issuing new debt).

Step 3: Check Compliance Metrics and Deadlines

Using your covenant register, gather the borrower’s financial data and calculate compliance metrics as defined in the agreement. For example, verify DSCR compliance using the property’s Net Operating Income (NOI) and scheduled debt service.

Assess the headroom between the current metrics and covenant thresholds. This shows how much room exists before a breach occurs. For instance, a DSCR of 1.35 compared to a minimum requirement of 1.25 leaves a 0.10 cushion.

Review reporting deadlines carefully. Quarterly statements might be due within 21 days of quarter-end, while annual reports could have a 60- to 90-day deadline after the fiscal year-end. Missing these deadlines can lead to a technical default, which can be as serious as missing a payment. Scenario modeling, such as a 12-month rolling forecast with base, upside, and downside cases, can help anticipate how future trends might impact compliance.

Step 4: Review Default Triggers and Remedies

Identify all default clauses in the loan agreement. These clauses specify the conditions under which the lender can declare a default, such as failing to meet financial covenants, missing payments, or violating negative covenants. Be sure to check for cross-default provisions, which allow a lender to declare a default if the borrower defaults on another loan.

Understand the cure periods available to the borrower, which typically range from 30 to 90 days. During this time, the borrower can address violations before the lender takes further action.

"Waivers are fine, but they need to be time-bound and need to be very specific." - Kent Kirby, Director of Advisory Services, Abrigo

Data shows that 20% to 30% of companies breach covenants during the life of a loan, often requiring amendments or waivers. Knowing the potential consequences - like higher interest rates, immediate repayment demands, or foreclosure - can help assess the loan’s risk profile. With this knowledge, move on to confirming compliance in the next step.

Step 5: Confirm Current Compliance Status

Using the borrower’s latest financial statements and operational records, verify compliance with all covenants. Compare the data against the thresholds and deadlines outlined in your covenant register and flag any potential issues for further review.

If a borrower is nearing a covenant threshold, it’s crucial to have escalation procedures in place. Reporting near-breaches to the CFO or Board early on allows for proactive negotiations with lenders, potentially avoiding a technical default. Between March 2017 and March 2022, lenders of North American first-lien debt recovered 62% to 71% of the original principal after defaults, highlighting the importance of timely intervention.

Document your findings clearly and systematically. This will not only support ongoing covenant monitoring but also help pinpoint recurring issues that might require renegotiation with the lender.

Tools for Covenant Analysis

Using specialized platforms can simplify covenant tracking and compliance reporting by automating key processes. These tools help reduce manual errors and offer real-time insights into compliance, making it easier to stay on top of covenant requirements.

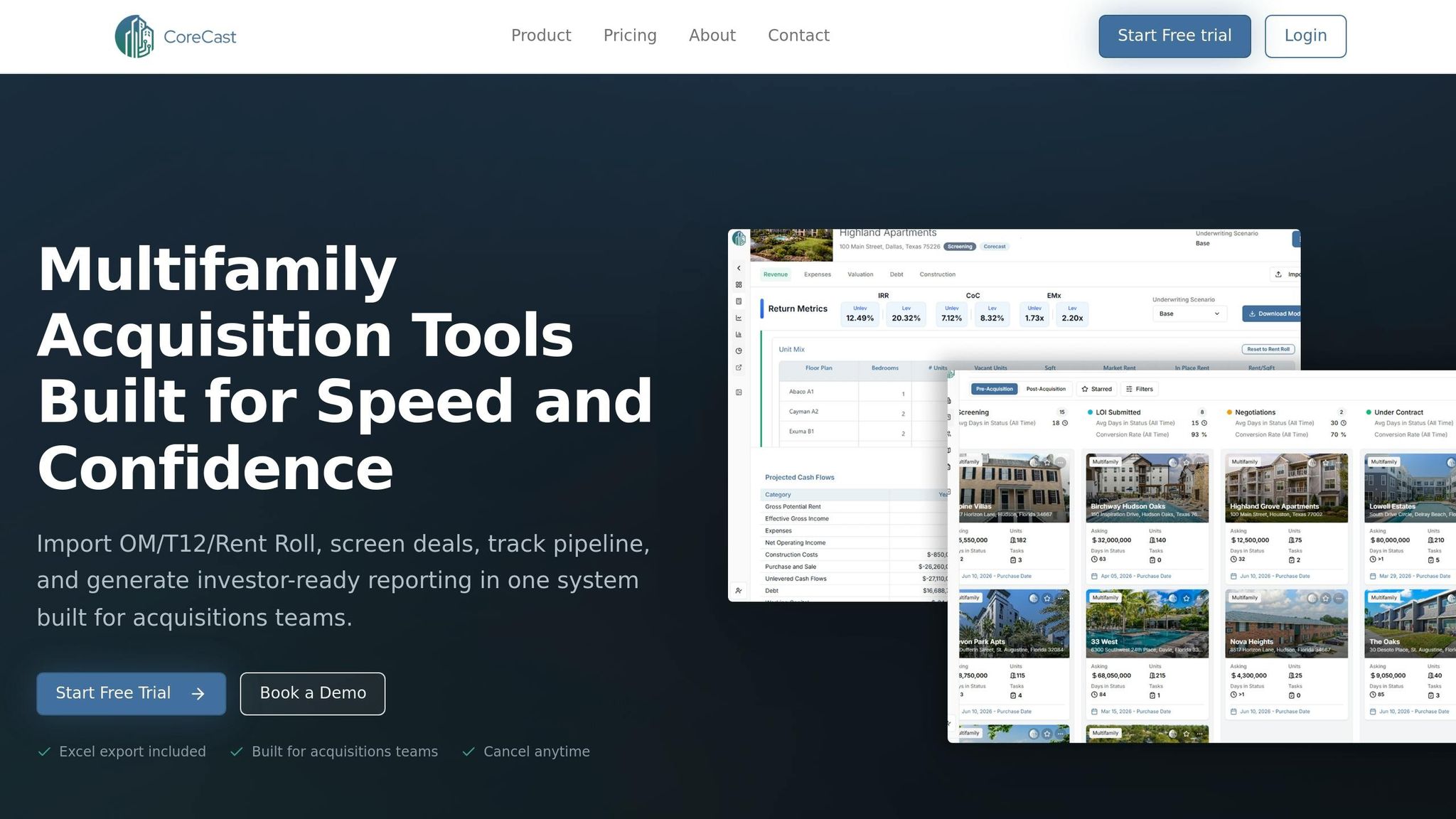

CoreCast for Self-Service Covenant Tracking

CoreCast is a real estate intelligence platform designed to centralize covenant tracking and automate compliance monitoring. It pulls data from multiple sources, standardizes it, and ensures consistency in financial reporting [1][3]. Its live dashboard provides real-time updates on critical metrics like DSCR and LTV ratios, allowing users to monitor compliance proactively. Automated alerts notify users of potential breaches, enabling timely communication with lenders.

One notable success story comes from a Director of Acquisitions at a REIT, who shared that CoreCast's Pipeline Tracker cut deal slippage by 30% over two quarters. This was achieved by consolidating financial data and automating tasks that previously consumed hours [1][3]. CoreCast isn't limited to covenant monitoring; it also supports broader asset management tasks like underwriting, deal pipeline tracking, and variance analysis. Currently, the platform is priced at $50 per user per month during its beta phase, with pricing expected to rise to $105 per user per month once all features are fully implemented [3].

For more intricate covenant-related needs, however, customized analytical support may be required.

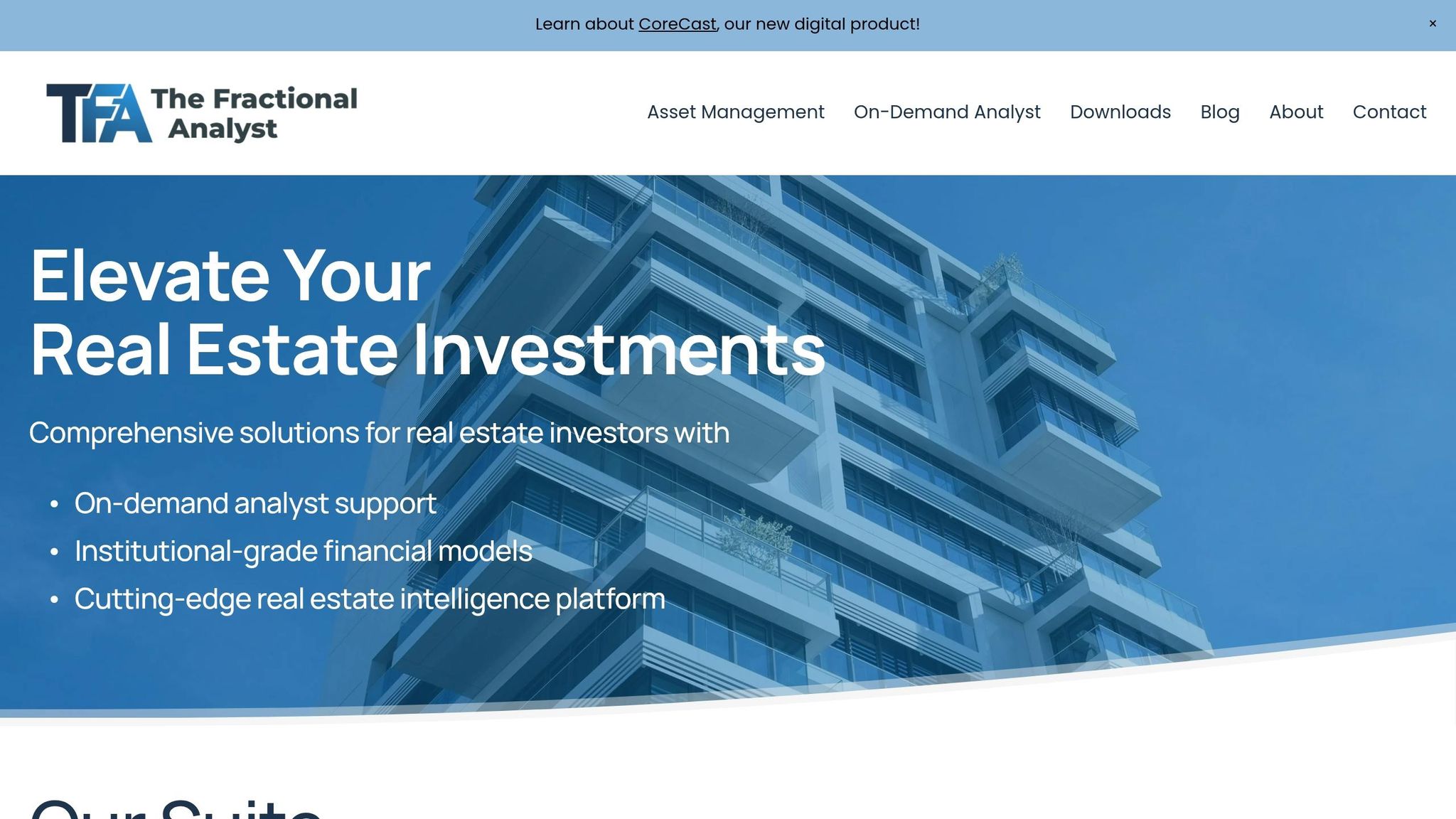

The Fractional Analyst for Custom Analysis

When dealing with complex loan structures, covenant negotiations, or modifications, The Fractional Analyst provides tailored financial analysis services. This is especially useful for firms working in specialized sectors like LIHTC affordable housing, data centers, or mixed-use developments, where advanced modeling is often necessary [2]. While CoreCast handles self-service tracking, The Fractional Analyst offers a hands-on approach, delivering expert insights for unique challenges.

"My banker was appalled with my partner's model. When he saw what The Fractional Analyst team put together, the approval process was infinitely smoother."

– Robert Dew, Principal, Castello Divino [2]

The service provides institutional-grade underwriting and pitch decks, helping to streamline bank approvals and boost investor confidence. Clay Heighten, Principal at Caddis Partners, shared his experience:

"The Fractional Analyst team stepped in when we had a gap in our analyst pool... seamlessly provided the expertise and support we needed to streamline our operations and make smarter, data‑driven decisions" [2]

Pricing for these services is flexible: 1:1 training starts at $145 per hour, and a ready-to-use Debt Financing Module is available for $34.99 [2]. This blend of expert support and on-demand tools ensures firms can tackle even the most challenging covenant scenarios efficiently.

Conclusion

Reviewing loan covenants thoroughly is crucial for avoiding technical defaults that could lead to loan acceleration or foreclosure. Shockingly, over 38% of middle-market companies unknowingly breach their loan agreements [1]. This often happens because manual tracking methods fail to catch critical thresholds or missed reporting deadlines.

A structured checklist can help ensure no covenant is overlooked. From gathering loan documentation to verifying compliance status, this step-by-step approach helps uncover restrictions on activities like taking on new debt, selling assets, or changing ownership - restrictions that might otherwise hinder growth. The due diligence phase is a critical opportunity to negotiate cure periods, define terms like "Adjusted EBITDA", and establish clear remedies for breaches before finalizing the agreement. This foundation sets the stage for adopting automation tools that simplify compliance tracking.

Automation tools take covenant management to the next level. Platforms like CoreCast automate data collection and send real-time alerts when financial metrics are at risk of breaching thresholds. Meanwhile, The Fractional Analyst offers expert insights for navigating complex loan structures. Together, these tools shift covenant management from a tedious obligation to a strategic advantage, especially when paired with regular oversight.

Proactive tracking delivers lasting benefits. Consistent monitoring fosters trust with lenders, which can lead to improved loan terms over time. Transparent communication and diligent tracking not only help avoid defaults but also strengthen financial partnerships that align with your commercial real estate goals.

FAQs

What’s the fastest way to find every covenant in my loan documents?

To efficiently find covenants in your loan documents, focus on sections outlining terms, conditions, and compliance. Use the document's search feature to look for keywords such as "covenant" or "compliance". It’s helpful to create a checklist to ensure you’ve reviewed all relevant sections. For better organization, group covenants by type - like financial or operational. Highlighting key details can make the review process smoother and simplify ongoing monitoring.

How do I calculate DSCR and LTV exactly as the lender defines them?

To calculate the Debt Service Coverage Ratio (DSCR), divide the Net Operating Income (NOI) by the total annual debt service, which includes both principal and interest payments. The formula looks like this:

DSCR = NOI ÷ Debt Service

Lenders typically look for a DSCR between 1.20 and 1.40. This range indicates that the property generates enough income to comfortably cover its debt obligations.

Loan-to-Value (LTV)

The Loan-to-Value (LTV) ratio is calculated by dividing the loan amount by the appraised property value or purchase price, then multiplying the result by 100 to express it as a percentage. Here's the formula:

LTV = (Loan Amount ÷ Property Value) × 100%

This ratio helps lenders assess the risk of the loan, with lower LTV ratios generally being more favorable.

What should I do first if I’m close to breaching a covenant?

If you’re approaching a covenant breach, the first step is to carefully review your loan agreement. Understanding the specific terms and thresholds will give you a clear picture of the situation and help you pinpoint the potential issue.

Once you’ve assessed your financial position and identified the risk, reach out to your lender without delay. Open communication is key - discuss options such as waivers or amendments to address the breach. Acting quickly not only helps reduce potential consequences but also shows your dedication to meeting the agreement’s requirements.