Escrow Agreements in CRE Transactions

Escrow agreements are essential in commercial real estate (CRE) deals. They ensure a neutral third party, the escrow agent, holds and manages funds or documents until all sale conditions are met. This protects buyers and sellers from unnecessary risks and ensures a smooth transaction. Here's what you need to know:

- Buyer’s Role: Deposit earnest money (1%-3% of the purchase price), conduct due diligence (inspections, financing, etc.), and finalize closing documents.

- Seller’s Role: Provide a clear title, resolve liens, and maintain the property until closing.

- Escrow Agent’s Role: Safeguard funds, verify conditions, manage prorations (taxes, rent, utilities), and handle fund disbursement and deed recording.

Key elements of escrow agreements include:

- Clear party identification and deposit details.

- Specific conditions for fund release (e.g., title clearance, inspections).

- Dispute resolution processes, such as mediation or interpleader.

The escrow process unfolds in three phases:

- Opening Escrow: Deposit earnest money and appoint an escrow agent.

- Due Diligence: Conduct property investigations and waive contingencies.

- Closing: Finalize documents, disburse funds, and record the deed.

Properly drafted escrow agreements ensure transactions proceed efficiently and minimize disputes. Clear timelines, objective release conditions, and financial planning are critical for success.

Why is Escrow Involved in Commercial Real Estate?

sbb-itb-df8a938

Parties Involved and Their Responsibilities

Every commercial real estate escrow agreement involves three key parties, each with specific responsibilities. Understanding these roles is essential to avoid delays and ensure all obligations are met for a smooth transaction.

What the Buyer Must Do

The buyer plays a pivotal role in meeting the terms of the escrow agreement. One of their first tasks is depositing earnest money into escrow, which is typically 1% to 3% of the purchase price in New York transactions [6]. This deposit serves as a good faith gesture, showing their commitment to completing the deal.

During the due diligence period, the buyer must conduct property inspections, evaluate zoning and environmental factors, and review financial documents, tenant estoppels, and title reports. Securing financing is another critical step, which includes ensuring that their lender deposits the necessary funds into escrow before closing.

Once due diligence is complete, the buyer usually makes a non-refundable deposit, except in cases of seller default or property damage. Up until this point, they can terminate the deal for any reason and receive a full refund. To finalize the transaction, the buyer must sign and deposit all required closing documents, including loan agreements, with the escrow agent.

These steps pave the way for the seller to fulfill their obligations.

What the Seller Must Do

The seller's primary responsibility is to provide a clear title and deliver all required documents. This includes resolving any liens, judgments, or encumbrances discovered during the title search. The seller must also maintain the property in its agreed-upon condition throughout the escrow period.

During due diligence, the seller is required to provide the buyer with disclosures, financial records, and legal documents. These may include tenant estoppels, service contracts, and property operating statements. At closing, the seller must deposit the executed deed and other necessary transfer documents - such as tax forms and affidavits - into escrow. They are also responsible for addressing any seller-side contingencies or completing agreed-upon property repairs within the specified timeline.

"By designating a portion of the deposit as non-refundable, the buyer is deemed to have paid for the option to purchase the property, thereby preventing the seller from terminating it at will." - Hollander Real Estate Law [5]

Once the seller fulfills their duties, the escrow agent takes over to complete the transaction.

What the Escrow Agent Does

The escrow agent acts as a neutral third party, ensuring that funds and documents are handled according to the escrow agreement. Often a title company or attorney, the agent safeguards earnest money deposits and purchase funds in separate accounts to avoid commingling and follows the agreement's explicit terms [1][6].

"The escrow agent acts as a neutral intermediary, ensuring that neither party can access the funds or property until all contractual obligations are met." - Hollander Real Estate Law [1]

The agent is responsible for preparing and verifying all necessary closing documents, such as the deed, loan papers, and local tax forms. They also calculate prorations for rent, taxes, utilities, and interest to ensure fair distribution. Once both parties provide written instructions, the agent disburses funds to pay off the seller's mortgage, compensate brokers and vendors, and distribute the remaining proceeds to the seller. Finally, they send the deed and other recordable documents to the appropriate municipal office for official recording [1][7].

In cases of disputes over fund release, the escrow agent remains neutral and may file an interpleader action, depositing the funds with a court for resolution [6]. This legal step protects the agent from liability while allowing the court to decide who is entitled to the disputed funds.

| Party | Primary Focus | Key Deliverables |

|---|---|---|

| Buyer | Funding and Verification | Earnest money, loan approval, inspection reports, closing documents |

| Seller | Performance and Delivery | Clear title, executed deed, property disclosures, repair completions |

| Escrow Agent | Neutral Oversight | Settlement statement, prorations, fund disbursement, deed recording |

What's Included in Escrow Agreements

A commercial real estate escrow agreement lays out the specifics of what assets are held, who has control over them, and the circumstances under which they can be released. These agreements are built around key elements designed to protect everyone involved.

Party Identification and Deposit Amounts

At the start, the agreement clearly identifies the buyer, seller, and escrow agent. It includes their full legal names, entity types, jurisdictions of formation, and contact information. This clarity ensures that only authorized individuals can provide instructions to the escrow agent [2].

Next, the agreement defines the deposit details, such as the earnest money amount, the payment method, and the designated holding account [3][2]. For acquisitions, escrow amounts typically hover around 8% of the purchase price for non-insured transactions and about 1% for insured ones [2].

Many agreements also include a small, non-refundable deposit - commonly $100 - as independent consideration. This amount is essential for making the Purchase and Sale Agreement legally binding and prevents the seller from unilaterally canceling the deal [5].

Once these foundational details are set, the agreement outlines the specific conditions under which funds can be released.

Conditions for Releasing Funds

Release conditions are clear and verifiable requirements that must be met before funds are disbursed [2]. Instead of vague language like "when concerns are resolved", well-drafted agreements specify exact triggers, such as "upon receipt of a signed regulatory approval letter", to avoid potential disputes [2].

Common triggers for releasing funds include clearing the property title, completing physical inspections, obtaining regulatory approvals, and the expiration of indemnity claim periods [3][2]. Escrow agents often require joint written instructions from both parties before disbursing funds, which helps limit their liability [5].

For more intricate transactions, a multi-tranche schedule can be included, detailing specific release dates and conditions tied to each disbursement [2]. The agreement should also specify whether disputes result in a hold on all funds or just the contested portion [2].

If disagreements arise over these conditions, the agreement provides a framework for resolving disputes.

How Disputes Are Resolved and Agreements Terminated

When disputes occur, the agreement lays out resolution methods such as mediation, arbitration, or an interpleader action. In an interpleader, the escrow agent deposits disputed funds with a court to avoid liability [3][2]. However, these processes can take time - arbitration or litigation over escrow disputes often spans 6 to 24 months [2].

Automatic termination provisions are also included, setting firm deadlines for action. If specific conditions aren't met by a given date, funds are returned to the buyer or sent to the seller [2]. In cases where the buyer defaults after the due diligence period and the deposit has "gone hard", the seller is typically allowed to terminate the escrow and claim the deposit as liquidated damages [2].

| Element | What It Covers |

|---|---|

| Parties | Full legal names and contact information for the buyer, seller, and escrow agent [2] |

| Assets Held | Items such as cash, stock certificates, deeds, intellectual property assignments, or earnest money [2] |

| Release Conditions | Triggers like completed inspections, obtained approvals, or expired claim periods [2] |

| Dispute Resolution | Steps for arbitration, mediation, or interpleader actions [2][3] |

| Indemnification | Protections for the agent when acting in good faith on instructions [2] |

| Fees and Costs | Details on the agent's compensation and which party is responsible for payment [2][3] |

How the Escrow Process Works

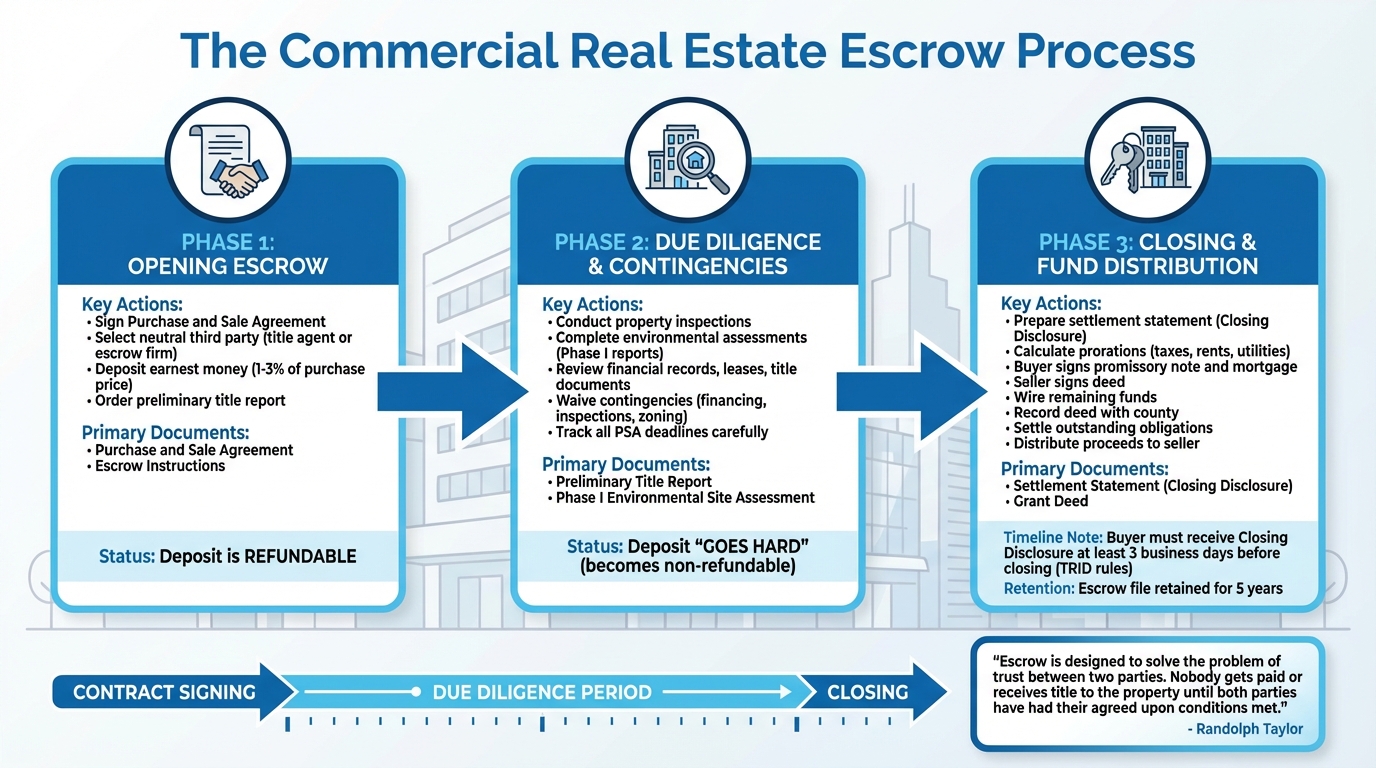

The 3-Phase Commercial Real Estate Escrow Process

The escrow process unfolds in three main phases, each with specific tasks and deadlines to ensure the transaction progresses smoothly. These steps reflect the responsibilities of buyers, sellers, and escrow agents, as previously outlined. Each phase builds on the last, moving from the initial deposit through due diligence and, finally, to closing.

Opening Escrow

Once the Purchase and Sale Agreement is signed, the buyer selects a neutral third party - usually a title agent or independent escrow firm - to oversee the transaction [12][9]. The buyer then wires the earnest money deposit into a secure trust account [9][5]. This deposit, typically 1% to 3% of the purchase price, signals the buyer's financial commitment [6].

"Escrow is designed to solve the problem of trust between two parties. Nobody gets paid or receives title to the property until both parties have had their agreed upon conditions met." - Randolph Taylor, Seller Guidance [12]

During this phase, the escrow agent orders a preliminary title report to uncover any liens or issues that might impact the property transfer [9]. It's crucial to double-check wire instructions with the escrow holder to guard against wire fraud, which has become increasingly sophisticated [5]. For commercial transactions involving entities like LLCs or corporations, verifying signing authority early is essential to avoid delays [10].

Due Diligence and Meeting Contingencies

The due diligence phase gives the buyer the opportunity to thoroughly investigate the property. This includes physical inspections, environmental assessments (such as Phase I reports), and a review of financial records, leases, and title documents [5][1]. During this time, the deposit remains refundable if the buyer decides to back out of the agreement [5]. Buyers should prioritize obtaining Property Condition Assessments and Phase I reports to avoid delays [11].

As deadlines approach, buyers are required to formally waive contingencies, such as those related to financing, inspections, and zoning compliance [12][9]. Once the due diligence period ends, the deposit usually becomes non-refundable, or "goes hard" [5]. Carefully track all deadlines in the Purchase and Sale Agreement (PSA) - missing even one can jeopardize the deal or lead to complicated renegotiations [11].

After completing due diligence and waiving all contingencies, the process moves to the closing phase.

Closing and Distributing Funds

At this stage, the escrow agent prepares a settlement statement, often referred to as the Closing Disclosure. This document details prorations for property taxes, rents, and utility payments [9][1]. Under federal TILA-RESPA Integrated Disclosure (TRID) rules, the buyer must receive this document at least three business days before closing [9]. A pre-closing audit ensures all loan conditions are met and documents are properly executed [8].

During closing, the buyer signs the promissory note and mortgage, while the seller signs the deed [9]. Once the buyer wires the remaining funds, the escrow agent verifies them and records the deed with the county, officially transferring ownership [9][8]. After the deed is recorded, the escrow agent settles any outstanding obligations, such as the seller's mortgage, broker commissions, and vendor fees, before wiring the remaining proceeds to the seller [9][1]. The escrow file is then retained for five years as required by law [8].

| Phase | Key Actions | Primary Documents |

|---|---|---|

| Opening Escrow | Deposit earnest money; Appoint escrow agent; Order title report | Purchase and Sale Agreement; Escrow Instructions |

| Due Diligence | Property inspections; Environmental reports; Title/Zoning review | Preliminary Title Report; Phase I Environmental Site Assessment |

| Closing | Sign final documents; Wire remaining funds; Record deed | Settlement Statement (Closing Disclosure); Grant Deed |

How to Draft and Manage Escrow Agreements

Tailoring Escrow Instructions to Your Deal

Creating well-crafted escrow instructions is crucial to protect the interests of all parties involved. These instructions should align closely with the Purchase and Sale Agreement (PSA) while addressing any specific risks tied to the deal. A key tip is to rely on objective release conditions rather than vague or subjective terms. For example, specify "receipt of a signed inspection report" instead of something like "satisfactory completion of due diligence" [2][13]. This approach reduces ambiguity, avoids interpretation disputes, and removes the need for the escrow agent to make judgment calls.

To prevent a seller from arbitrarily terminating the PSA, include a nominal, non-refundable deposit, such as $100, as independent consideration [5]. This creates a legally enforceable option for the buyer. For risks that extend beyond closing - like unfinished repairs or unresolved permits - draft holdback agreements that clearly outline the amount, purpose, and a buffer for unexpected costs [14]. Additionally, attach exhibits like "Joint Written Instructions" or required legal opinions to the original agreement. This ensures both parties agree on the release documentation format upfront [13].

Avoiding Common Escrow Problems

Vague timelines and unclear conditions are often the root causes of escrow disputes. To avoid these pitfalls, define clear "going hard" dates and any exceptions, such as seller defaults or casualty events [5]. Requiring joint written instructions and including interpleader clauses can further reduce disputes and limit the escrow agent's liability [2][4].

Seyfarth's 2023/2024 M&A Survey notes that in acquisition deals, the typical escrow amount averages 8% of the purchase price for non-insured transactions and 1% for insured deals [2]. Considering that commercial disputes in arbitration take an average of 26 months to resolve [2], precise documentation is essential to sidestep lengthy and costly litigation. This level of detail also supports better financial planning and modeling throughout the transaction.

Using Financial Models for Escrow Planning

Financial models are a valuable tool for aligning escrow instructions with practical cash flow management. These models can help predict escrow needs and ensure they align with underwriting goals. For example, use them to calculate earnest money "going hard" dates, prorate taxes and utilities, and design multi-tranche release schedules for more complex deals [2][1]. This ensures the escrow timeline integrates seamlessly with cash flow requirements, especially for indemnity holdbacks that may extend over 12 to 24 months.

For those seeking additional support, The Fractional Analyst (https://thefractionalanalyst.com) provides free real estate financial models, including acquisition tools and IRR matrices. These resources can help you project escrow needs and align them with transaction goals. For more intricate scenarios, expert analysts can offer tailored assistance for underwriting and asset management.

Conclusion

Escrow agreements play a crucial role in commercial real estate (CRE) transactions by safeguarding funds until all agreed-upon conditions are met. This process protects both buyers and sellers, reduces risks, and ensures that financial details - like prorations for rent, taxes, and utilities - are handled accurately [1][2].

The key to a smooth escrow process lies in establishing clear, objective conditions and well-defined release triggers. Considering that commercial dispute arbitration can take an average of 26 months to resolve [2], having precise and thorough documentation is essential to avoid delays or costly litigation. Drafting escrow agreements that align seamlessly with your Purchase and Sale Agreement can help prevent conflicts and support detailed financial planning.

Strong financial planning is equally important for escrow success. Aligning cash flow with deposit timelines and release schedules ensures the process runs smoothly. For those looking to streamline this aspect, The Fractional Analyst (https://thefractionalanalyst.com) provides free financial tools, such as acquisition models and IRR matrices, to help forecast escrow requirements. Their team also offers tailored financial analysis for more complex transactions, making them a valuable resource for CRE professionals.

FAQs

When does an earnest money deposit “go hard” in a CRE deal?

When an earnest money deposit "goes hard" in a commercial real estate deal, it means the deposit becomes non-refundable and non-contingent. This usually occurs once the buyer either fulfills or waives certain contractual conditions or deadlines, signaling their firm commitment to move forward with the transaction.

What should escrow release conditions look like to avoid disputes?

To ensure smooth transactions, escrow release conditions must be clearly outlined. These should include specific legal triggers like verified completion of contractual milestones, adherence to regulatory requirements, and mutual agreement between the involved parties. It's crucial to have proper documentation that confirms these conditions have been fulfilled, as this helps prevent potential disputes down the line.

What happens if the buyer and seller disagree on releasing escrow funds?

If the buyer and seller can't agree on releasing escrow funds, the matter usually goes through mediation, arbitration, or litigation to reach a resolution. During this process, the escrow agent remains a neutral party, ensuring the funds are held securely and verifying that all conditions are met before releasing the money.