How to Estimate Defeasance Costs

When exiting a commercial real estate loan early, defeasance often becomes necessary. Instead of paying off the loan directly, you replace the property lien with government securities (like U.S. Treasuries). This process can be costly and depends heavily on factors like interest rates, loan terms, and third-party fees. Here's what you need to know:

- Defeasance Costs: Includes the price of securities (based on Treasury yields), third-party fees (e.g., legal, accounting, custodian), and potential administrative expenses.

- Interest Rates Matter: Higher Treasury yields can reduce costs, while lower yields increase them. Small rate changes can have a big impact.

- Third-Party Fees: These can range from $50,000 to $150,000 and include legal, servicer, and custodian charges.

- Timing: The process takes 30–45 days, and market fluctuations during this period can alter costs.

Accurate cost estimation requires understanding your loan details, current market rates, and potential fees. Use tools like financial calculators or consult experts to avoid surprises and make informed decisions.

Prepayment Penalties - Yield Maintenance, Defeasance, Step-Down Prepayment Penalties Explained

sbb-itb-df8a938

What Is Defeasance and Why Does It Matter?

Defeasance is a process where, instead of paying off your loan directly, you replace the property securing the loan with a portfolio of U.S. Treasury or Agency securities. A successor entity then formally takes over the debt obligations [1][9].

Why does this matter? It allows you to release the mortgage lien on your property, enabling you to sell or refinance even when direct prepayment isn’t an option [1][11]. For lenders and investors in Commercial Mortgage-Backed Securities (CMBS), defeasance ensures they continue receiving the anticipated income stream. As CMBS Loans explains:

Defeasance ensures that even if a borrower wants to exit early, the bondholders continue to receive their scheduled payments from the substitute collateral, maintaining the integrity and ratings of the securitized debt [11].

How Defeasance Works

The process involves purchasing government securities - such as U.S. Treasuries or Fannie Mae/Freddie Mac Agency bonds - that align with your loan’s remaining payment schedule [2][11]. These securities are managed by a custodian bank, which ensures monthly payments are directed to the loan servicer [1][9]. Additionally, a bankruptcy-remote Special Purpose Entity (SPE) is created to assume the loan, guaranteeing that payments continue uninterrupted [11].

This process generally takes 30 to 45 days to complete [9][12]. During this time, you’ll work with a defeasance consultant, accountants, lawyers, and rating agencies to confirm that the bond portfolio meets the loan’s requirements and doesn’t negatively impact the CMBS pool’s credit rating [9][12]. Once everything is finalized, your property is released from the mortgage, allowing you to proceed with your plans to sell or refinance.

Knowing how defeasance works helps you understand its purpose and when it’s necessary.

When Defeasance Is Required

Defeasance is typically required for securitized loans, particularly CMBS loans and Freddie Mac or Fannie Mae Agency loans, where early repayment would disrupt cash flows for investors [1][3]. These loans often come with a two-year lockout period after securitization, during which prepayment - including defeasance - is not permitted [10].

You’ll encounter the need for defeasance in situations like selling a property during the lockout period, refinancing to take advantage of better interest rates or increased property value, or restructuring your portfolio to offload underperforming assets [1][11]. Between the 2014 conduit vintage and late 2024, the total outstanding defeased balance exceeded $21.0 billion, with the average loan balance for defeasance typically around $10 million [13].

Next, we’ll break down how to calculate the costs involved in this process.

Components of Defeasance Costs

Understanding the costs associated with defeasance involves breaking them into three main categories. Each plays an essential role in determining your overall budget, and together, they form the total cost of defeasance.

Securities Purchase Costs

The securities portfolio is typically the largest expense in a defeasance transaction. This cost is calculated as the present value of all remaining loan payments - both principal and interest - through the loan's maturity date or the early prepayment window. The calculation uses current U.S. Treasury yield rates as the discount factor [7][9].

When Treasury yields are lower than your loan's interest rate, the cost of the securities exceeds your loan balance, resulting in a premium. On the other hand, if Treasury yields are higher than your loan rate, you may experience a discount - or even receive a payment instead of facing a penalty [8][17]. This difference is referred to as the defeasance premium (or discount) [8][11].

The formula for securities cost is as follows:

Securities Cost = Σ [ PMT / (1 + treasuryRate)^i ] [7].

In addition, an administrative fee - around 0.5% of your loan balance - typically covers the coordination and management of the process [7].

Third-Party Fees

Defeasance transactions also involve several third-party fees, which usually range from $50,000 to $150,000 depending on the complexity of the deal [11]. A defeasance consultant serves as the key coordinator, managing communication between accountants, lawyers, and servicers [18].

Here’s a breakdown of common third-party costs:

- Servicer legal fees: Typically between $12,000 and $25,000 [18].

- Flat legal and processing fees: Often starting at $25,000 [7].

- Independent accountant fees: Required for a "Sufficiency Report", which verifies that your securities portfolio generates enough cash flow to meet future debt obligations [15].

- Rating agency fees: For larger loans, agencies like Moody's or S&P may charge $15,000 to $25,000 to ensure the collateral substitution won't affect bond ratings [5][16].

- Custodian bank fees: A custodian bank manages the securities in a segregated account and handles monthly disbursements to the servicer [4][18].

Amber Martin from Thirty Capital emphasizes the importance of transparency in these costs:

"A standard defeasance quote should provide you with a clear breakdown of the costs and fees... Hidden fees and misrepresented quotes can quickly turn a seemingly straightforward transaction into a costly headache" [15].

Additional Expenses and Taxes

Some transactions may involve extra costs, such as expedite fees ranging from $5,000 to $10,000 for rapid closings [5]. If the transaction falls through, breakage costs of $20,000 to $30,000 may also apply [5].

On the tax side, defeasance expenses are generally deductible as interest expenses, similar to prepayment penalties [16]. However, there’s a key tax consideration, particularly for transactions tied to a 1031 exchange. Anthony Bakale, CPA at Cohen & Company Ltd., explains:

"The expense of a defeasance transaction is deductible as interest expense, so to the extent that proceeds of a sale are used to pay any expense associated with a defeasance (even transaction fees), those funds are likely considered taxable boot" [16].

This tax detail is crucial for anyone structuring their transaction as part of a 1031 exchange [16].

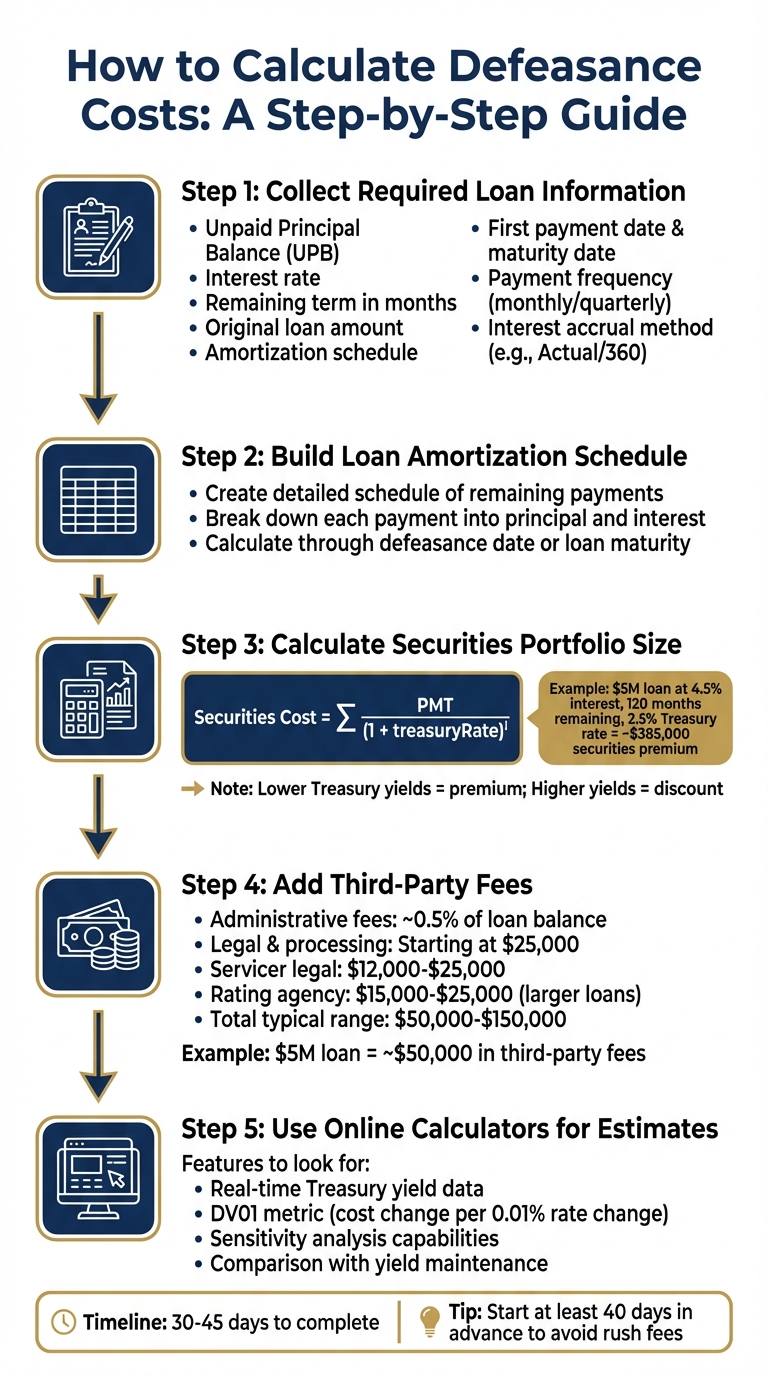

How to Calculate Defeasance Costs

5-Step Process to Calculate Defeasance Costs for Commercial Real Estate Loans

To determine your total defeasance expenses, you’ll need to combine loan details, market rates, and fee estimates. Here's a step-by-step guide to help you navigate the process.

Collect Required Loan Information

Start by gathering essential loan details from your promissory note and pooling and servicing agreement (PSA). Key data includes the unpaid principal balance (UPB), interest rate, and remaining term in months [7][8]. Also, note the original loan amount, amortization schedule, and any interest-only periods [8][19].

Pay attention to key dates like the first full payment date, loan maturity date, and your anticipated defeasance date [4][19]. Additionally, identify payment specifics such as frequency (monthly or quarterly), due dates, and the interest accrual method (e.g., "Actual/360") [7][8]. Review the PSA to confirm whether agency bonds like Fannie Mae or Freddie Mac are allowed as collateral, as they may offer better yields and lower costs than U.S. Treasuries [3][6].

With this data in hand, you can create an accurate payment schedule.

Build the Loan Amortization Schedule

Next, develop a detailed amortization schedule that outlines the remaining payments up to your defeasance date or loan maturity. This schedule will break down each payment into principal and interest amounts [7][8].

Calculate the Securities Portfolio Size

To estimate the cost of the securities portfolio, use the present value formula:

Securities Cost = Σ [ PMT / (1 + treasuryRate)^i ], where PMT represents each payment amount [7]. Discount each future payment using current U.S. Treasury yield rates that align with your loan’s remaining maturity [7][6].

For example, if you have a $5,000,000 loan at 4.5% interest with 120 months left and a 2.5% Treasury rate, you’d need about $385,000 in securities premium [7]. When Treasury yields are lower than your loan rate, you’ll pay a premium. If rates are higher, you might receive a discount - or even a residual payment if rates rise significantly (by 300 basis points or more) [8][3]. Conduct sensitivity analyses with different rate scenarios to understand potential impacts [8].

This portfolio cost serves as the foundation for your overall expense calculation.

Add Third-Party Fees

In addition to securities costs, account for fees charged by various third parties, including defeasance consultants, servicers, legal counsel, securities custodians, accountants, successor borrowers, and possibly a rating agency [19][4]. Administrative fees typically amount to around 0.5% of the loan balance, while legal and processing fees often start at $25,000 [7]. For a $5,000,000 loan, these fees can total approximately $50,000 [7].

Be aware that fees can vary depending on the master servicer. For instance, changes like Trimont’s acquisition of Wells Fargo’s servicing segments (effective March 1, 2025) may influence fee structures [21].

Use Online Calculators for Estimates

Many defeasance consultants offer free tools to help you determine whether defeasance is financially viable compared to yield maintenance [20]. Platforms like CoreCast by The Fractional Analyst provide advanced modeling tools, allowing commercial real estate professionals to refine cost projections with real-time market data. These calculators can also help you understand metrics like "DV01" (Dollar Value of 0.01), which shows how much the securities cost decreases for every 0.01% increase in interest rates [4].

What Affects Defeasance Costs

The cost of defeasance can range widely - sometimes tens of thousands, sometimes hundreds of thousands of dollars. Several factors influence this variation. By understanding these elements, you can better plan your transaction and steer clear of unexpected expenses.

Interest Rate Environment

The primary driver behind defeasance costs is the relationship between current U.S. Treasury yields and your loan's interest rate. When Treasury yields are lower than your loan rate, the cost increases due to a higher premium. On the flip side, higher Treasury rates can reduce costs, sometimes even leading to a discount[11][3].

"The cost of defeasance is highly sensitive to prevailing interest rates, particularly U.S. Treasury yields, and can be substantial, requiring careful financial modeling." – REI Prime[11]

For example, as of February 17, 2026, the 10-year Treasury yield was 4.058%, while the 2-year yield stood at 3.439%[22]. These rates fluctuate daily, and even minor changes can have a big impact. The DV01 metric (Dollar Value of 1 basis point) measures how much the cost of your securities decreases for every 0.01% increase in rates[4].

A real-world case from March 2023 illustrates this: Walker & Dunlop reviewed a $95 million loan from November 2020 with a 2.53% interest rate. Due to favorable Treasury yield conditions, the securities traded at a 6.5% discount, resulting in $6.1 million in savings for the borrower, who was then able to secure a new $135 million loan[24].

Loan Characteristics

While market rates set the foundation for defeasance costs, your loan's specific terms also play a significant role. For instance, loans with longer remaining terms require more securities to cover future payments, which increases costs. A $10 million loan with five years left will cost much more to defease than the same loan with only one year remaining[11].

The spread between your loan's interest rate and current Treasury yields is another key factor. A wider spread - say, a 5.00% loan versus 3.00% Treasury yields - can lead to significantly higher expenses[11]. Additionally, your amortization schedule matters. Loans with interest-only periods may have different cost dynamics compared to fully amortized loans. If your loan includes an early open prepayment window (often six months before maturity), costs can be reduced by limiting the securities needed to cover payments until that window opens.

Timing and Market Conditions

Defeasance costs aren't fixed - they're snapshots that reflect market conditions at a specific moment. Bond prices change constantly, so estimates can vary even within minutes. The 30- to 45-day period required to complete the transaction introduces another layer of uncertainty, as costs may shift during that time[9].

"Bond prices change constantly, so estimates that are compiled even a few minutes apart may show different costs. Costs will very likely change between the time of the estimate and the time of the defeasance closing." – Chatham Financial[9]

For instance, in early 2026, markets were volatile due to Federal Reserve leadership changes, including Kevin Warsh's nomination to replace Chair Powell[4]. Delays in economic data releases, like the personal consumption expenditures (PCE) index, further influenced Treasury yields[22]. In March 2023, a borrower with a $28.2 million loan (from December 2020, with a 2.51% rate and five-year term) refinanced when securities traded at a 3.2% discount. This resulted in $895,341 in savings and funded a new $40.2 million loan[24].

To navigate these fluctuations, it’s crucial to monitor Treasury yields that align with your loan’s remaining term. Using sensitivity calculators to model rate changes of 100 to 300 basis points can help you identify the best timing for your transaction[23][8]. Advanced tools and careful tracking can make a significant difference in managing these cost variables effectively.

Tools and Services for Defeasance Cost Estimation

Getting an accurate estimate for defeasance costs involves more than just basic math - it requires specialized tools and expertise. That’s where The Fractional Analyst comes in. They offer a range of resources, from free calculators to premium services, designed to simplify the process whether you’re a hands-on user or someone who prefers professional assistance.

Free Financial Models and Calculators

The Fractional Analyst provides free online tools to help you estimate costs quickly. These calculators allow you to input key details like loan balance, interest rate, remaining term, and current Treasury yields to generate instant results - no email required.

One standout feature is the inclusion of a DV01 metric, which shows how much the cost of securities decreases for every 0.01% increase in interest rates [4]. For those who want more control, downloadable financial models are also available. These templates include debt financing modules, enabling users to create custom amortization schedules and track interest, principal, and balances for even the most intricate debt structures.

It’s important to note, though, that Treasury yields fluctuate daily. If you’re using these tools, you’ll need to manually update them with the latest rates from reliable sources like the Federal Reserve or financial news outlets [7].

For more complex situations that require pinpoint accuracy, professional financial analysis is available.

Custom Financial Analysis Services

While free calculators are great for initial estimates, more complicated transactions often call for expert help. Professional defeasance consultants can replicate your loan’s amortization schedule and calculate costs using real-time market prices for securities - not just static formulas [26][7]. This level of detail can make a big difference, as even minor inaccuracies could lead to significant cost discrepancies.

"Defeasance is a complex financial strategy... calculating the total cost - including securities cost, administrative fees, and legal charges - can be daunting without the right tools." – Sage Calculator [7]

The Fractional Analyst’s team specializes in uncovering cost-saving opportunities and ensuring every component of your defeasance cost is calculated precisely. Their services include underwriting, asset management support, and detailed debt reviews, with pricing starting at $145 per hour. They also handle non-standard loan features like balloon payments and interest-only periods, which free calculators often can’t accommodate [7].

For those who prefer a more hands-on approach, The Fractional Analyst offers a self-service platform that blends flexibility with professional-grade capabilities.

CoreCast: Self-Service Platform for CRE Professionals

CoreCast, The Fractional Analyst’s real estate intelligence platform, fills the gap between free calculators and full-service consulting. It’s designed for commercial real estate (CRE) professionals who want to handle institutional-grade underwriting and debt modeling on their own [25].

Building on existing plug-and-play financial modules, CoreCast helps users calculate the Defeasance Premium - the difference between the cost of replacement securities and the current loan balance - to determine if an early exit is financially viable [7]. Users can also run sensitivity analyses by adjusting Treasury yield assumptions (e.g., shifting rates by 100 basis points) to see how market changes might impact overall costs [8].

Currently in beta testing at $50 per user per month, CoreCast’s full pricing will range up to $105 per user per month once fully launched. Doug Taylor, Owner of Safe Haven Homes, LLC, shared his experience:

"I needed a model for single family development. The mixed-use development from The Fractional Analyst was a good start. Really looking forward to CoreCast!" [25]

This platform is especially useful for CMBS loans, where defeasance is the standard prepayment method. It also lets users compare defeasance costs with alternatives like yield maintenance or waiting for the open window period [14][7].

Whether you’re using free tools, custom services, or CoreCast, these resources ensure you can calculate securities costs, third-party fees, and other transaction expenses with confidence.

Conclusion

Estimating defeasance costs accurately involves a mix of factors like interest rates, loan details, and third-party fees. Key elements such as present value calculations and changing Treasury yields play a significant role in determining the final expense[27][9].

Having expert guidance and reliable tools can make a big difference. Since 2000, professional defeasance consultants have helped clients recover over $225 million in residual value[9]. They excel at spotting cost-saving opportunities, such as structuring bonds to an "early open" prepayment date instead of waiting for full maturity[9].

"The role of defeasance consultant is unique because it is the only party with expert knowledge of the entire process that also acts as an advocate for the borrower." – Chatham Financial[9]

This specialized knowledge ensures every cost is thoroughly evaluated. Whether you're using free online calculators, hiring The Fractional Analyst for custom analysis at $145 per hour, or opting for CoreCast's self-service platform at $50 per user per month during beta, having precise tools helps you avoid surprises. Be proactive: ask for detailed fee breakdowns, use sensitivity calculators to understand how rate changes affect costs, and start the process at least 40 days in advance to steer clear of rush fees[15][9].

FAQs

How do I know if defeasance or waiting for the open window is cheaper?

When deciding between defeasance and waiting for the open window, it's essential to weigh the total defeasance costs - this includes securities, legal fees, and administrative expenses - against any potential prepayment penalties. Keep a close eye on current interest rates and Treasury yields, as these play a major role in shaping defeasance costs. A thorough evaluation of market conditions will help you pinpoint the most cost-effective choice.

What loan details do I need to get an accurate defeasance estimate?

To calculate defeasance costs with precision, you'll need specific details about the loan. Key factors include the original loan amount, interest rate, remaining term or maturity, payment frequency, and the loan's amortization or payment schedule. These elements are crucial for making accurate calculations and forecasts.

How can I reduce interest-rate risk during the 30–45 day defeasance process?

During the 30–45 day defeasance process, borrowers face potential interest-rate fluctuations that can pose risks. To manage this, they often turn to tools like interest rate swaps or interest rate caps. These financial instruments help either lock in current rates or limit exposure to rising rates, offering a layer of stability throughout the process.