How Projection Horizons Impact Valuations

Projection horizons are the timeframes used to forecast a property's income and expenses, typically spanning 5 to 15 years. These horizons are critical in real estate valuation, influencing risk assessment, expected returns, and decision-making. Here's what you need to know:

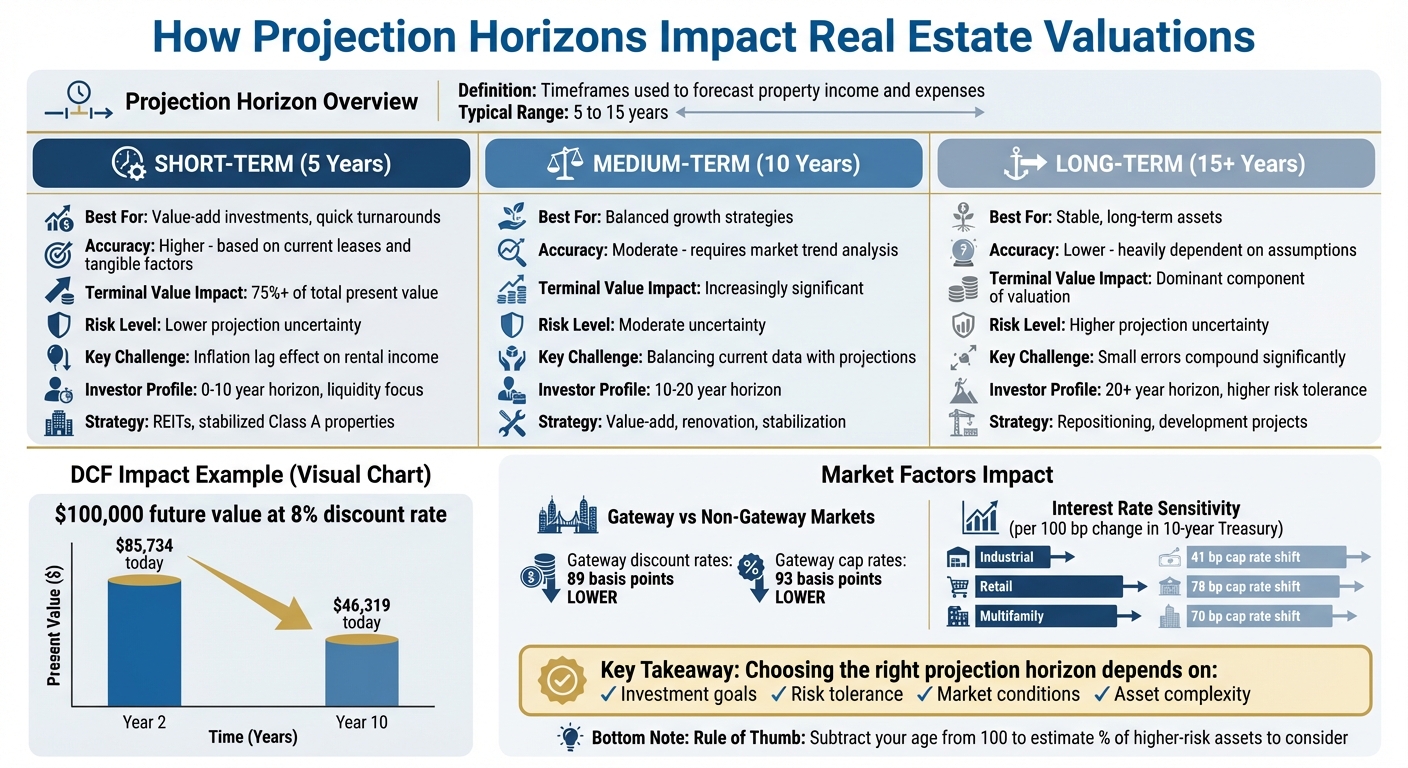

- Shorter horizons (5 years) suit quick-turnaround strategies like value-add investments.

- Longer horizons (10–15 years) are better for stable, long-term assets.

- The horizon length impacts Discounted Cash Flow (DCF) models, with longer horizons placing more weight on terminal value assumptions.

- External factors like interest rates, inflation, and market volatility affect valuations differently depending on the horizon.

Choosing the right projection horizon depends on your investment goals, risk tolerance, and market conditions. Understanding this concept helps investors make informed decisions and align strategies with their financial objectives.

Real Estate Projection Horizons: Short-Term vs Long-Term Investment Strategies Comparison

[Valuations DCF] 2.5. DCF Forecast Years (5-Year vs 10-Year vs 20-Year DCF)

sbb-itb-df8a938

How Time Horizons Affect Valuation Models

The length of your projection horizon has a direct impact on how you value a property. A 5-year horizon will yield a different net present value (NPV) compared to a 15-year horizon. Longer timeframes magnify the effects of discounting and place greater emphasis on terminal assumptions.

Impact on Discounted Cash Flow (DCF) Modeling

In DCF modeling, each cash flow is divided by ( (1 + r)^n ), meaning the further into the future a cash flow occurs, the less valuable it becomes today. For instance, $100,000 received in year 10 at an 8% discount rate is worth about $46,319 today, whereas the same amount in year 2 is worth approximately $85,734.

As the projection horizon extends, the terminal value becomes a larger component of the total valuation. For example, in a 5-year appraisal, the sale proceeds represented over 75% of the total present value ($803,089 out of $1,046,501) [7]. This reliance on a single future assumption makes longer projections more susceptible to errors. As PropertyMetrics explains:

"DCF analysis isn't just helpful, it's essential... for scenarios involving fluctuating cash flows, such as renovations, lease-ups, or repositioning." [7]

Even small adjustments to the discount rate can significantly alter the NPV in long-term projections [8].

Capitalization Rates and Holding Periods

Beyond discounting, capitalization metrics also heavily influence valuation. Cap rates represent a single period’s income-to-value ratio, while discount rates account for the timing of cash flows. These two metrics align only when there is zero NOI growth [9].

Longer holding periods often correspond with lower cap rates in stable markets. For instance, in gateway markets, discount rates are on average 89 basis points lower than in non-gateway markets, while cap rates are about 93 basis points lower [3] [4]. This compression reflects lower perceived risk over extended horizons in high-demand locations. Between 2007 and 2020, transaction-based discount rates in Switzerland dropped by 2.1 percentage points (from 4.9% to 2.8%) as government bond yields declined [9].

Cash Flow Projection Challenges Across Different Horizons

As projection horizons stretch further, the complexity of variables increases, and the likelihood of errors grows. This makes it essential to rely on practical models and cautious assumptions. Building on earlier discussions about valuation models, this section explores how the accuracy of projections shifts between short- and long-term horizons.

Short-Term vs. Long-Term Projection Accuracy

Short-term projections, usually covering up to three years, are grounded in tangible factors like current lease agreements, tenant reliability, and documented rent rolls. One major hurdle in short-term forecasting is the "lag effect" of inflation on rental income[3][4]. When inflation rises, rental income doesn't immediately follow suit because lease rates are often locked for specific periods. Martin Hoesli, a Professor at the University of Geneva, explains:

"Inflation has an immediate negative impact on capitalisation and discount rates due to the delayed adjustment of the rental income, but the effect turns positive over time."[3]

On the other hand, long-term projections, which typically span 5 to 15 years, are heavily influenced by terminal value calculations. Small errors in assumptions, such as a minor 1% miscalculation in rental growth, can snowball over time and significantly affect outcomes. These projections are especially challenging in markets with limited comparable transactions or complex multi-tenant properties, where estimating terminal values becomes more speculative[1][5].

Key Variables in Projection Models

Several factors are critical to the reliability of cash flow projections:

- Lease Expirations: These can directly affect cash flow by causing vacancies and re-letting costs.

- Real Interest Rates: Higher borrowing costs typically push up both capitalization and discount rates across all timeframes[3][4].

- Economic Growth: While real GDP growth may have a minimal short-term effect, sustained growth can lower risk premiums over the long run[3][4].

The complexity increases for properties undergoing significant changes, such as renovations or repositioning. In these cases, traditional metrics like cap rates may not adequately reflect the timing and variability of cash flows during these capital-intensive phases. Since terminal value often represents a large portion of the overall valuation, even slight errors in exit cap rate assumptions can lead to major discrepancies. To improve accuracy, it’s recommended to validate terminal value estimates using both the perpetuity growth method and the exit multiple method.

These challenges highlight the need to align cash flow projections with realistic market conditions to support sound investment decisions.

External Factors That Affect Valuations by Horizon

Macroeconomic conditions influence investment valuations differently depending on the timeframe. Whether you're looking at a three-year hold or a fifteen-year horizon, the timing and scale of these effects vary. Understanding these nuances is key to accurate valuation.

Interest Rates and Cap Rate Sensitivity

Projection horizons play a significant role in how interest rates impact valuations. Changes in rates, driven by Federal Reserve policies, directly affect the 10-year Treasury yield - a key benchmark for real estate cap rates[10]. However, the effects differ by property type and investment horizon.

In the short term, rising interest rates immediately increase borrowing costs. Yet, cap rates take time to adjust, often lagging behind[10]. Over longer horizons, higher real interest rates steadily push up capitalization and discount rates. This happens as institutional investors shift their portfolios in response to these changes[3][4]. According to Martin Hoesli, Professor at the University of Geneva:

"Real interest rates consistently increase capitalisation, discount and growth rates through higher borrowing costs and portfolio reallocations."[3]

Different property sectors react uniquely to interest rate fluctuations. For instance, a 100-basis-point change in the 10-year Treasury yield results in varying cap rate adjustments: industrial properties see a 41-basis-point shift, retail properties experience a 78-basis-point change, while multifamily and office properties fall in between at 75 and 70 basis points, respectively[10].

Looking ahead, CBRE predicts cap rate compression by the end of 2025: industrial cap rates may decline by 40 basis points, retail by 35, multifamily by 25, and office by 20[10]. However, all long-term stabilized cap rates are expected to remain higher than pre-COVID levels, with industrial and multifamily at around 4.5%, office at 5.0%, and retail at 4.6%[10].

Location also matters. Gateway markets consistently show lower rates, with discount rates averaging 89 basis points lower and cap rates 93 basis points lower than non-gateway markets[3][4]. This reflects the greater liquidity and lower perceived risk in these areas. CBRE Research advises investors to focus on broader macroeconomic indicators like inflation, GDP growth, and risk premiums, rather than relying solely on Federal Reserve rate adjustments[10]. As they explain:

"Conditions that facilitate changes in short-term policy rates influence the long-end of the yield curve, which in turn most influences real estate investment activity."[10]

These interest rate dynamics set the foundation for understanding how market volatility impacts valuations over different timeframes.

Market Volatility and Horizon Risk

Market volatility affects valuations in distinct ways depending on the projection horizon. While short-term valuations are more sensitive to immediate policy changes and economic uncertainty, long-term projections capture broader trends and gradual shifts.

Short-term projections often feel the brunt of volatility caused by sudden economic changes. For example, while real GDP growth can reduce risk premiums and discount rates over time, these effects take longer to materialize as economic expectations stabilize[3][4].

For longer horizons, incorporating time-varying discount rates into valuation models provides a more accurate reflection of historical market values compared to models that assume constant returns[6]. Inflation further complicates the picture. Initially, inflation negatively impacts cap rates due to delayed rental income adjustments. However, over time, as leases reset and rental income catches up, this effect reverses[3][4].

This creates a divergence between short-term and long-term valuations during periods of high volatility. For investors with extended horizons, it's essential to account for these shifts rather than simply projecting current conditions forward[6]. By doing so, they can better navigate the complexities of market cycles and economic changes.

Using Projection Horizons in Investment Decisions

When making investment decisions, understanding projection horizons is crucial. The right horizon isn’t a one-size-fits-all choice - it depends on your financial goals, risk tolerance, and personal circumstances. Aligning these factors with your projection horizon can significantly influence the success of your investments.

Matching Horizons to Investor Profiles

Your investment horizon should reflect your financial situation and how much risk you’re comfortable taking on. As Feldman Equities explains:

"The longer an investor's time horizon, the more risk they can take on. The opposite is true for those with a short-term time horizon." [12]

For short-term horizons (0–10 years), liquidity and stable income are often priorities. These goals are typically achieved through investments like REITs or fully stabilized Class A properties. Medium-term horizons (10–20 years) allow for value-add strategies, such as acquiring properties, renovating them, and stabilizing occupancy before refinancing. Long-term horizons (20+ years) provide the flexibility to pursue higher-risk, higher-reward opportunities, like repositioning a property over an extended period.

A simple rule of thumb: subtract your age from 100 to estimate the percentage of higher-risk assets you might consider. For first-time investors, starting with short-term, fully stabilized investments can provide a solid foundation while building experience [12].

These individual considerations naturally inform how to select the right projection horizon.

Best Practices for Selecting Horizons

Choosing the right horizon requires balancing projection accuracy with your investment timeline, asset complexity, and market conditions. For example, real estate discounted cash flow (DCF) analyses often assume holding periods of 5 to 15 years [1]. Shorter horizons work well for stable properties with ample comparables, while more complex assets, like multi-tenant properties, require longer and more detailed DCF models [5].

Market conditions are another critical factor. Gateway markets, known for their stability, can support longer projection horizons.

Your discount rate should also align with your risk profile. Core investors tend to use rates close to benchmark yields, such as the 10-year Treasury. On the other hand, value-add and opportunistic strategies often require higher risk premiums to account for uncertainties specific to the property [11]. In volatile market conditions, increasing your discount rate can help account for potential downturns during the projection period.

Finally, running sensitivity analyses can provide a clearer picture of potential outcomes. By modeling best-case and worst-case scenarios for variables like rental rates, vacancy, and operating expenses, you can better understand how changes might impact your returns. Some experienced investors even set hurdle rates above their actual cost of capital to guard against overly optimistic cash flow projections [13].

Conclusion

Projection horizons play a crucial role in shaping discount rates and interpreting market risks. Studies indicate that shifts in property market values are largely driven by changes in expected returns rather than fluctuations in operating cash flows [6]. In other words, the horizon you choose directly influences how you balance risk and return.

Explicit DCF modeling builds clarity when valuing complex assets [2]. External factors, like inflation and interest rates, influence valuations differently over time. For example, inflation initially lowers cap and discount rates due to rental lags, but this trend reverses over longer periods. Meanwhile, real interest rates tend to drive rates higher, and gateway markets typically show discount rates about 89 basis points lower than non-gateway markets [3].

Adapting your modeling approach to suit your asset type and timeline is essential. For properties with limited comparable transactions, explicit DCF modeling is especially useful [5]. During periods of market volatility, incorporating appraisal smoothing can be advantageous, as it helps account for discount rates lagging behind current conditions [9]. Aligning these strategies with your investment profile strengthens decision-making.

For professionals aiming to refine their underwriting and valuation processes, The Fractional Analyst offers customized financial analysis and expert tools. From DCF modeling to market research and investor reporting, their resources - like the CoreCast platform - equip you to apply these projection horizon principles effectively, ensuring more confident valuation and underwriting choices.

FAQs

How do I choose the right projection horizon for my deal?

Selecting the right projection horizon is all about aligning it with your investment goals and the type of property you're dealing with. If you're in it for the long haul, a longer timeframe might make sense since risks often level out over time. On the other hand, shorter horizons are better suited for situations where you need a quick valuation.

Don't forget to factor in things like market trends, economic conditions, and the unique characteristics of the property itself. These elements can significantly influence cash flow projections and how accurate your valuations turn out to be. Choosing the right timeframe is key to ensuring your financial goals are properly supported.

How much should terminal value influence my DCF valuation?

Terminal value often represents 60-80% of a Discounted Cash Flow (DCF) valuation, making it a critical component to estimate with care. The accuracy of this figure can significantly impact the reliability of your entire analysis.

To get it right, ensure your method for calculating terminal value aligns seamlessly with the broader valuation context. This means selecting an approach that reflects the specific characteristics of the business and its industry while maintaining consistency in your assumptions.

What assumptions matter most when extending a model to 10–15 years?

Key assumptions involve practical cash flow projections, accounting for market trends, and factoring in economic elements such as interest rates and inflation. These factors play a major role in shaping discount rates and ensuring precise valuations over extended periods, making them essential for dependable long-term modeling.