LTV in CRE Loans: Risk Assessment Guide

Loan-to-Value (LTV) ratio is critical in commercial real estate (CRE) loans. It measures the loan amount against the property’s value, expressed as a percentage. Lower LTVs mean less risk for lenders, while higher LTVs often lead to stricter terms or loan rejection. Here’s what you need to know:

- LTV Formula: Loan Amount ÷ Property Value × 100%

- Key Inputs: Loan amount and appraised property value (lower of appraisal or purchase price).

- Common LTV Ranges:

- ≤ 60%: Low risk, best terms.

- 60-75%: Moderate risk, standard terms.

- 75-80%: Elevated risk, stricter terms.

- > 80%: High risk, limited financing options.

Lenders use LTV alongside metrics like Debt Service Coverage Ratio (DSCR) and Loan-to-Cost (LTC) to size loans and manage risk. Changes in property values can impact LTV over time, requiring ongoing monitoring. For example, LTVs originally at 65% in 2021 may now exceed 80% due to declining property values.

Pro Tip: Always confirm the valuation method (current, stabilized, or completed value) with your lender, as it directly affects loan terms. For construction and value-add projects, expect a shift from LTC to LTV as the property stabilizes.

Understanding LTV helps borrowers secure better terms and prepare for potential market shifts. Keep reading for detailed examples, thresholds, and tips to navigate LTV in CRE loans.

How to Calculate LTV for CRE Loans

The LTV Formula and Key Inputs

The formula for Loan-to-Value (LTV) is straightforward:

LTV = Loan Amount ÷ Property Value × 100%

Getting this calculation right depends on two critical inputs: the loan amount and the property value. The loan amount refers to the total principal being requested or currently outstanding. For the property value, precision is key - this is generally the lower of the appraised market value or the purchase price. A third-party institutional appraisal typically determines this value, rather than a broker's opinion of value (BPO). Why does this matter? Because BPOs tend to be 5–15% higher than formal appraisals, which could skew the numbers [2].

The choice of property value has a direct impact on lender risk management. The specific value used - whether it's based on current or projected conditions - can significantly influence the loan terms and proceeds.

LTV Adjustments by Loan Type

The "value" in the LTV formula depends on the type of loan and its purpose. Here’s how it varies:

- As-is value: Represents the property’s current condition and occupancy. This is the standard metric for stabilized acquisitions and refinances.

- As-stabilized value: Reflects the projected value once the property achieves target occupancy and income. This is often used by bridge lenders to assess the viability of future takeout loans.

- As-completed value: Applies to construction loans and represents the projected value of the property upon completion, before it reaches full lease-up.

For construction or value-add projects, lenders typically use Loan-to-Cost (LTC) during the construction phase. Once the property stabilizes, they switch to LTV. A helpful rule of thumb: LTC governs when costs exceed value, while LTV takes over when value exceeds costs [2].

It’s also worth noting that while amortization can improve LTV over time, falling property values - such as the 10–25% declines seen since 2021 - can push LTV higher despite regular principal payments [2].

Worked Example: LTV Calculation for a CRE Loan

Here’s a practical example to illustrate how LTV and LTC calculations work across the lifecycle of a commercial real estate (CRE) loan [2]:

| Stage | Input | Amount |

|---|---|---|

| Acquisition price (as-is value) | Purchase price | $30,000,000 |

| Renovation budget | Hard + soft costs | $5,000,000 |

| Total project cost (TDC) | Sum of above | $35,000,000 |

| Projected as-stabilized value | Post-renovation appraisal | $40,000,000 |

| Bridge loan at 75% LTC | $35M × 0.75 | $26,250,000 |

| Permanent takeout at 70% LTV | $40M × 0.70 | $28,000,000 |

In this value-add multifamily example, the bridge loan is sized using LTC during the renovation phase. Once the property stabilizes, the permanent lender re-evaluates the loan using LTV based on the as-stabilized value. The difference - $1,750,000 - represents the "lift", or the extra proceeds unlocked by completing the business plan.

Before moving forward, always confirm with your lender which valuation approach applies. This can make or break the deal’s feasibility.

sbb-itb-df8a938

How to Calculate LTV and LTC - 30 Second CRE Tutorials

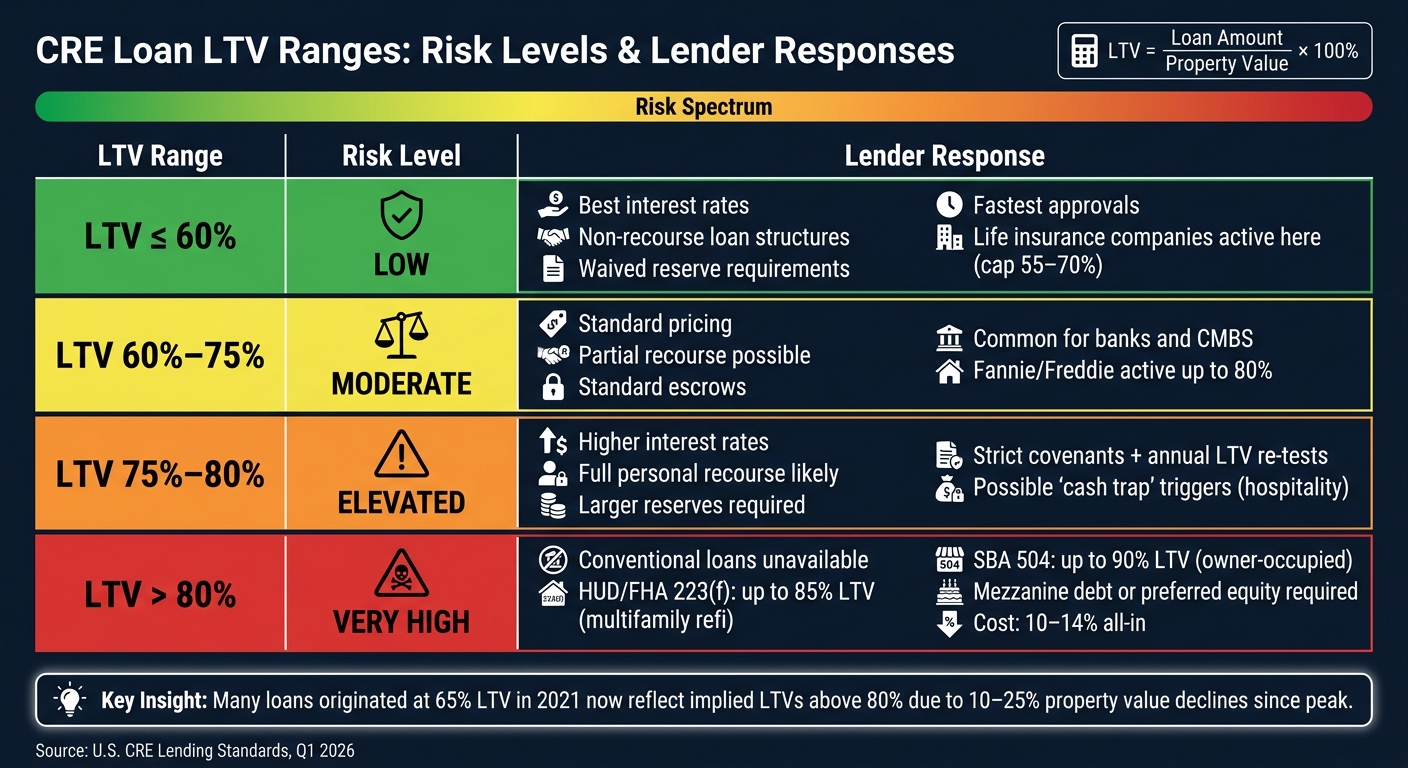

LTV Ranges and What They Mean for Risk

CRE Loan LTV Ranges: Risk Levels & Lender Responses

Common LTV Thresholds in U.S. CRE Lending

Once you've calculated the Loan-to-Value (LTV) ratio, the next step is understanding what it says about risk. In U.S. commercial real estate (CRE) lending, not all LTV ratios are treated equally. Different ranges send distinct signals to lenders, and their responses vary accordingly.

For most commercial loans, the general LTV benchmark falls between 65% and 80% [3]. However, this range isn't one-size-fits-all. By Q1 2026, institutional maximums have tightened by 5–10 percentage points compared to their 2021 peaks [2]. Sector-specific dynamics also play a major role. For example, multifamily properties typically average around 73% LTV, while office and hospitality assets are now capped at 50–60%, reflecting long-term shifts in demand rather than temporary market cycles [5].

"Office is no longer a cyclical recovery story. It is a capital reallocation story." - Spencer Vickers, The Fractional Analyst [5]

Other sectors, like industrial, retail, and self-storage, tend to hover in the 60–70% LTV range, offering a middle ground between the relative stability of multifamily and the heightened caution seen in office investments [5].

These LTV thresholds aren't just theoretical - they shape how lenders structure loans and assess risk.

How Lenders Adjust Decisions Based on LTV

LTV ratios directly influence the terms and conditions lenders attach to loans. At lower LTV levels (below 60%), borrowers usually benefit from the best terms. This includes lower interest rates, waived reserve requirements, and often non-recourse loan structures. The approval process is also faster because the lender's risk is minimal with such a significant equity cushion [8].

When LTV ratios approach the 75–80% range, things start to shift. Lenders respond by increasing interest rates, requiring larger reserves, and imposing stricter covenants. Full personal recourse becomes more common, and some lenders may add annual LTV re-test clauses. These clauses mean that if the property's value drops during the loan term, borrowers might have to pay down the principal or provide additional collateral [2][5]. In high-risk sectors like hospitality, lenders may even implement "cash traps", where property income is redirected into a lender-controlled reserve if performance falls short of agreed benchmarks [5].

For LTV ratios above 80%, traditional financing options become scarce. Borrowers in this range often turn to government-backed programs like HUD/FHA 223(f), which allows up to 85% LTV for multifamily refinances, or SBA 504 loans, which can go as high as 90% LTV for owner-occupied properties. Alternatively, borrowers may need to layer in mezzanine debt or preferred equity, which typically comes with much higher costs - 10–14% all-in [2][8].

Table: LTV Bands and Risk Profiles

Here’s a quick breakdown of LTV bands and how they influence risk and lender behavior:

| LTV Range | Risk Level | Typical Lender Response |

|---|---|---|

| ≤ 60% | Low | Best rates, non-recourse loans, waived reserves, faster approvals [2][5][8] |

| 60% – 75% | Moderate | Standard pricing, partial recourse possible, standard escrows; common for banks and CMBS [2][3][8] |

| 75% – 80% | Elevated | Higher rates, full recourse likely, larger reserves, strict covenants, LTV re-tests [2][5][8] |

| > 80% | Very High | Conventional loans unavailable; requires HUD, SBA, or mezzanine/preferred equity at higher costs [2][8] |

One key insight: the type of lender is just as important as the LTV ratio itself. For instance, life insurance companies typically cap LTV at 55–70% and offer the most favorable terms within that range. On the other hand, agency lenders like Fannie Mae and Freddie Mac are more aggressive, going up to 80%, and even 85% for affordable housing projects [2]. Understanding which lender aligns with your LTV can make a significant difference in securing the right terms.

Using LTV Within a Broader Loan Risk Framework

How LTV Interacts With Other Risk Metrics

Loan-to-Value (LTV) is a cornerstone of loan underwriting, working alongside metrics like Debt Service Coverage Ratio (DSCR) and exit cap rates. While LTV evaluates the equity buffer, DSCR ensures the property generates enough income to cover debt payments, and exit cap rates protect against potential declines in future property values. Lenders typically calculate the maximum loan amount using both LTV and DSCR, then proceed with the lower figure. For instance, a deal might meet the required 70% LTV threshold but still be capped by a stricter DSCR limit. This trend is especially pronounced as many lenders increasingly prioritize DSCR stability over appraised values, given the limited refinancing options available today. This layered approach allows risk assessments to adapt over time, reflecting ongoing performance metrics.

"Underwriting is no longer a static exercise built on historical averages and optimistic forward projections. It has become a forward-looking stress test." - Spencer Vickers, The Fractional Analyst[5]

In construction and value-add projects, LTV often works in tandem with Loan-to-Cost (LTC). While LTV measures debt against the anticipated market value, LTC evaluates debt relative to total project costs. For example, bridge loans use LTC during the draw phase and LTV based on stabilized appraisals to confirm the feasibility of the exit strategy. Together, these metrics create a more comprehensive risk management framework, ensuring both cost exposure and future value are assessed throughout the deal.

However, a high LTV paired with a DSCR at or below 1.0x is a warning sign. This combination suggests the property may struggle to generate enough income to cover its debt obligations without additional equity injections[9].

Using LTV to Structure and Monitor Loans

LTV isn’t just a tool for initial underwriting - it plays a crucial role in ongoing loan oversight. Lenders often set LTV-based covenants, monitor performance, and even trigger reserves based on LTV fluctuations. For example, commercial banks frequently require annual LTV reviews, often paired with appraisal re-tests. If a re-test shows a drop in property value, borrowers may need to provide additional equity to restore the LTV to acceptable levels. In sectors like hospitality, where metrics such as RevPAR or NOI can be volatile, a drop in performance might lead to cash traps - redirecting property income into lender-controlled reserves until benchmarks are met again[5].

One emerging risk is the "LTV step-down" issue, which is expected to become more prominent by 2026. Many loans originated between 2017 and 2021 at 65–70% LTV now face implied LTVs of 80% or higher due to cap-rate expansion compressing appraised values by 10–25% since their 2021 peaks[2]. Borrowers looking to refinance are encountering funding gaps that didn’t exist when the loans were first issued. To address this, it’s vital to model LTV against current cap rates - rather than relying on original acquisition values - before approaching lenders.

Table: Loan Terms Across LTV Scenarios

| LTV Threshold | Loan Term Impact | Risk Profile |

|---|---|---|

| 65% or lower | Favorable interest rates; often non-recourse terms | Lowest risk; strong equity cushion[10] |

| Around 70% | Competitive rates with standard terms | Moderate risk; balanced financing[10] |

| Around 75% | Potential for higher interest premiums | Higher risk; may require additional collateral[10] |

| 80% or higher | Less favorable terms; may trigger additional covenants | Highest risk; increased probability of covenant triggers[10] |

How Lenders and Investors Apply LTV in Practice

LTV Workflow for Lenders

Lenders use LTV as part of a broader risk assessment strategy, combining it with other metrics to determine loan sizing. The process starts with the valuation baseline, where lenders take the lower of the appraised value or the purchase price to calculate LTV. This safeguards against inflated valuations that could lead to over-lending.

Next, lenders calculate the maximum loan amount based on LTV, DSCR (Debt Service Coverage Ratio), and Debt Yield constraints. They then choose the lowest figure from these tests to finalize loan size. For example, even if a deal meets a 65% LTV threshold, it might still be reduced by a stricter DSCR limit.

"The lower the spread between the loan amount and the value of the property, the higher the risk for the lender." - Robert Schmidt, CCIM, PropertyMetrics [6]

When LTV ratios are higher, lenders often impose higher interest rates and stricter terms to offset the increased risk [1][3]. Over the 2025–2026 period, many lenders have tightened LTV limits across various asset classes, as illustrated below:

| Asset Class | 2024–2025 LTV Range | 2024–2025 DSCR Range |

|---|---|---|

| Office | 50%–60% | 1.45x–1.65x |

| Multifamily | 60%–70% | 1.30x–1.50x |

| Industrial | 60%–70% | 1.30x–1.45x |

| Retail (Necessity) | 60%–70% | 1.35x–1.55x |

| Hospitality | 50%–60% | 1.50x–1.75x |

| Self-Storage | 60%–70% | 1.30x–1.50x |

Source: The Fractional Analyst [5]

LTV Workflow for Equity Investors

Equity investors also rely on LTV to assess their position in the capital stack and evaluate the level of risk. A lower LTV indicates that more equity is built into the deal, offering a cushion against potential property value declines [3].

Over recent years, equity requirements have increased significantly. Before COVID-19, multifamily deals often closed with 70%–80% LTV. Now, the range has shifted to 60%–70% [5]. Office properties have seen an even sharper decline, with LTV limits dropping from 65%–75% to 50%–60%. For Class B/C office assets, financing may not even be available. These higher equity requirements mean lower return-on-equity if projected income falls short.

The key takeaway for equity investors? Use conservative assumptions. Stress-test LTV scenarios with current cap rates rather than acquisition-era values. If a deal only works under optimistic projections, the equity position is more vulnerable than it may appear [5].

Tools to Support LTV Analysis: The Fractional Analyst

With leverage constraints tightening, precise LTV analysis has become essential. However, fragmented tools like spreadsheets often fail to deliver the accuracy and consistency needed. This is where The Fractional Analyst steps in, offering two options for LTV analysis:

- Direct Servicing: A team of financial analysts provides hands-on support, including underwriting, asset management, and lender/investor reporting. They help with custom LTV modeling, sensitivity analysis, and covenant monitoring.

- Self-Servicing: The CoreCast platform offers real-time data, dashboards, and forecasting tools to streamline underwriting. Available at $50/user/month during beta, CoreCast also includes free downloadable tools like multifamily acquisition models and IRR matrices for teams needing quick solutions.

Both options are designed to deliver the rigorous, data-driven analysis required for effective LTV management and risk assessment.

Conclusion and Key Takeaways

LTV serves as a dependable starting point for assessing risk in a CRE loan. It highlights the equity supporting a deal, the lender's vulnerability to property value drops, and the available loss cushion. Generally, a lower LTV indicates greater borrower equity, a stronger collateral safety net, and often more favorable loan terms.

That said, the accuracy of LTV hinges on the valuation it’s based on. A 2024 Moody's Ratings analysis of 41 banks revealed a stark contrast: while lenders reported an average CRE LTV of 54.8%, the actual estimated average was closer to 74.2% [7]. This gap illustrates the potential pitfalls of relying solely on static appraisals in a market that’s constantly shifting.

Experts echo this warning:

"If you're not adjusting your cap rate to current market environment, then [LTVs] are not useful. They're misleading." - Tom Iadanza, President, Valley National Bancorp [7]

The takeaway here is clear: LTV should never be viewed in isolation. It works best when combined with other metrics like DSCR, Debt Yield, and current-market cap rates to provide a fuller picture. For construction and value-add projects, Loan-to-Cost (LTC) is more appropriate during the build phase, transitioning to LTV at stabilization. Loans should always be sized to the most conservative figure among these measures [4].

Looking ahead, CRE debt maturing between 2025 and 2027 amounts to about $1.5 trillion, with cap rates now exceeding 2021 levels by over 150 basis points. Deals structured at 65% LTV in 2021 may now reflect implied LTVs above 80% due to value compression [2]. This highlights the importance of maintaining disciplined, real-time LTV assessments.

FAQs

Which property value does my lender use for LTV?

Lenders determine the Loan-to-Value (LTV) ratio by comparing the appraised market value of the property and its purchase price, then using the lower of the two. This approach ensures the loan amount is calculated based on the more cautious property valuation.

Why can my LTV rise even if I pay down the loan?

Your Loan-to-Value (LTV) ratio can go up even as you pay down your loan. Why? Because it's calculated by dividing your loan amount by the current value of your property. If your property’s value drops due to market conditions, the ratio might increase, even though you're actively reducing your loan balance. This shows how much property values and market trends can influence your financial picture.

If my LTV is too high, what financing options do I have?

If your loan-to-value (LTV) ratio is above what lenders typically allow, you have a few ways to address the issue:

- Increase your equity contribution: Putting more of your own money into the deal reduces the loan amount, bringing down the LTV.

- Look for financing with lower LTV requirements: Some lenders or loan products might have more flexible terms that better suit your situation.

- Restructure the deal: Adjusting the overall financing structure can help lower the loan amount and align your LTV with lender expectations.

Lenders usually cap LTV ratios between 60% and 75%, depending on the type of property and loan product. Making these adjustments can help ensure your LTV meets their criteria.