Vacancy Loss and Revenue Stabilization Explained

Vacancy loss happens when rental spaces sit empty, cutting into your income and property value. For example, a 10% vacancy rate on a property with $500,000 potential annual income means losing $50,000. This loss affects cash flow, financing options, and operational costs.

To combat this, focus on:

- Reducing Vacancies: Improve property management, market units early, and offer flexible leases.

- Maintaining Revenue: Build financial reserves, adjust rent pricing, and diversify tenant types.

- Cutting Costs: Streamline turnover processes and invest in marketing tools like virtual tours.

Vacancy loss impacts more than just rent - it can lower property value by 2-3% for every 1% increase in vacancy. Managing this risk is key to keeping your property financially stable.

3 Expert Strategies to Minimize Vacancy Loss

sbb-itb-df8a938

What Causes Vacancy Loss

Understanding what drives vacancy loss is key to safeguarding your property's financial health. From broader economic trends to specific property issues and sudden external disruptions, these factors directly influence how vacancy loss affects overall performance.

Economic and Market Conditions

Economic trends play a big role in vacancy rates. When the economy is growing, businesses expand and demand for space increases, which typically reduces vacancies. On the flip side, during economic downturns, companies may downsize or shut down, leading to more empty spaces [1]. Factors like job growth and GDP expansion also fuel demand by giving businesses the resources and confidence to grow [4].

Local market conditions can create imbalances too. For instance, when new construction outpaces demand or higher interest rates make borrowing costlier, expansion plans often slow down [4]. Additionally, the rise of remote and hybrid work has shifted office space preferences, with modern Class A buildings seeing higher demand than older Class B and C properties. In industrial markets, e-commerce growth has helped keep vacancies low, while in retail, reduced consumer spending can weaken demand for storefronts [4].

Property-Level Issues

Issues specific to a property can also drive vacancy loss. Deferred maintenance is a major culprit - properties that look outdated or need significant repairs tend to stay vacant longer [1][5]. A neglected facade or an old-fashioned lobby can push potential tenants toward better-maintained options [4]. Operational inefficiencies, like slow unit turnovers due to poor coordination between maintenance and leasing teams, also contribute. High-performing teams typically prepare units within 3 to 5 days, minimizing downtime [6].

Meeting tenant expectations is another critical factor. Properties lacking modern amenities - such as high-speed internet, coworking spaces, or in-unit laundry - are less appealing to renters. Slow response times can further hurt leasing efforts; studies show that responding to inquiries within five minutes can increase lead conversion rates by up to eight times [6].

External Disruptions

Unexpected events can also cause vacancy spikes, even for well-managed properties. Regulatory and legal hurdles, such as lengthy eviction processes, can significantly impact vacancy rates. For instance, when a tenant stops paying rent but remains in the unit, the property loses income while incurring legal and collection costs [1].

In retail, losing an anchor tenant - like a major grocery store - can trigger co-tenancy clauses, allowing smaller tenants to reduce their rent or break leases, leading to a chain reaction of vacancies [4]. Additionally, a surge in new construction can temporarily flood the market with available space, increasing competition even for properties that are well-maintained and managed [3][4]. These challenges highlight the importance of proactive strategies to maintain occupancy.

How Vacancy Loss Affects Your Finances

Financial Impact of Vacancy Loss: Costs and Property Value Effects

Vacancy loss doesn't just mean a temporary dip in income - it creates a cascade of financial challenges. From ongoing expenses to diminished property value and the costs of attracting new tenants, the financial impact can be significant. Let’s break it down into three areas: lost income, property value reduction, and tenant turnover costs.

Lost Income and Continuing Expenses

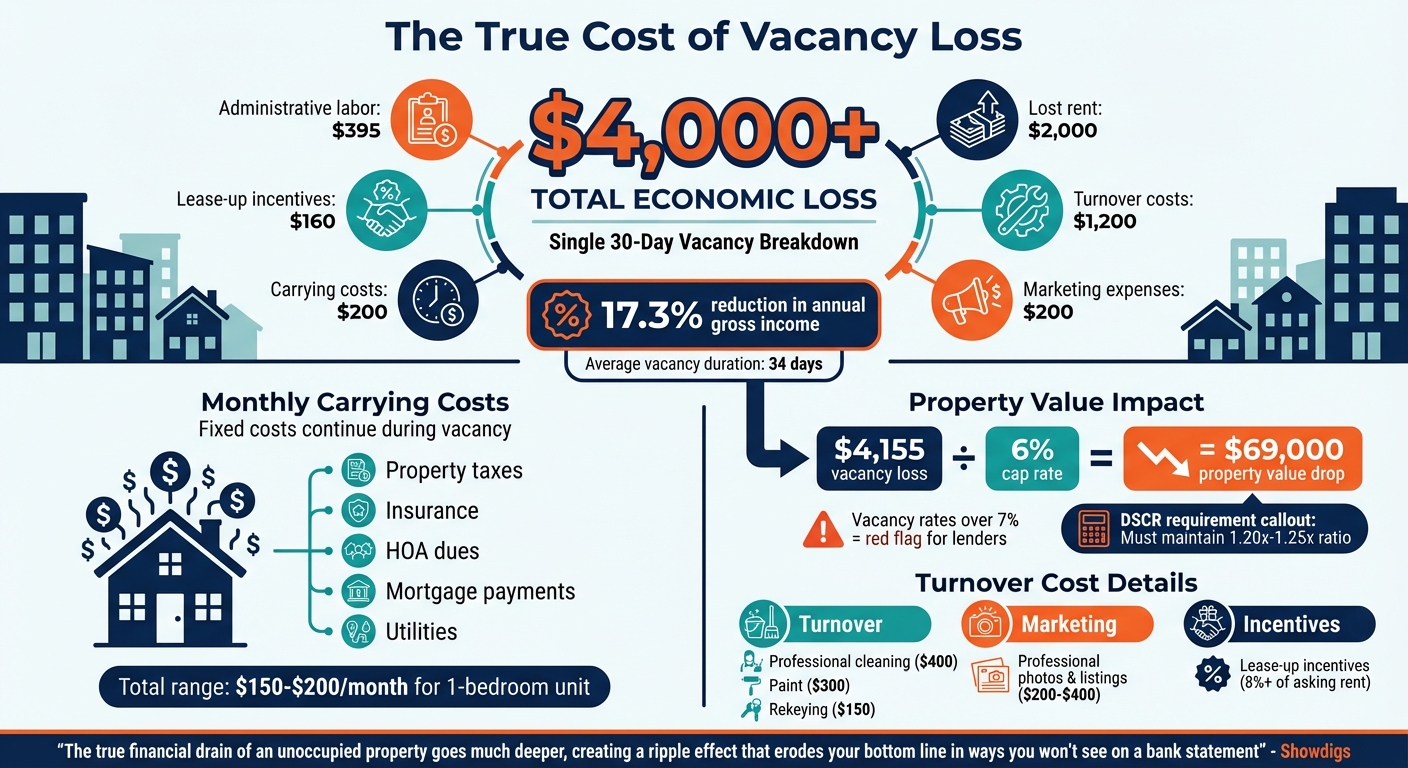

When a rental unit is unoccupied, the rent stops coming in, but your fixed costs don’t take a break. Expenses like property taxes, insurance, HOA dues, mortgage payments, and utilities - often ranging between $150 and $200 monthly for a one-bedroom unit - keep piling up [5][6][7].

Here’s an example: a single 30-day vacancy in a unit renting for $2,000 could lead to a total economic loss exceeding $4,000. This figure includes not just the lost rent but also $160 in lease-up incentives, $1,200 in turnover costs, $200 in marketing expenses, $200 in carrying costs, and $395 in administrative labor. All of this can reduce annual gross income by 17.3% [7]. With the average multifamily unit sitting vacant for over 34 days between tenants, this isn't a one-time issue - it’s a recurring financial burden [7].

Effects on Property Value and Financing

Vacancy directly affects your property’s Net Operating Income (NOI), which is a key factor in determining its market value. For commercial and multifamily properties, value is calculated by dividing NOI by the capitalization rate. So, a $4,155 vacancy loss at a 6% cap rate results in a property value drop of about $69,000 [7].

Vacancies also make refinancing more difficult. Lenders assess debt capacity based on stabilized NOI. If your property doesn’t maintain stable occupancy, you might not qualify for the loan amount you’re expecting [3]. Even worse, prolonged vacancies could trigger loan covenant violations, such as falling below the required Debt Service Coverage Ratio (typically 1.20x to 1.25x), which could lead to a technical default [3]. For stabilized assets, vacancy rates over 7% are often seen as a warning sign by lenders [6].

Costs of Finding New Tenants

The process of filling a vacant unit comes with its own set of expenses, including turnover costs, marketing, and lease-up incentives. Turnover costs alone - such as professional cleaning ($400), paint touch-ups ($300), and rekeying locks ($150) - can range from a few hundred dollars to over $1,000 per unit [7][8].

Marketing adds another layer of expense, with professional photos and listing fees typically costing $200 to $400 [7][8]. Competitive markets often demand lease-up incentives, which can exceed 8% of the asking rent [7]. Administrative labor for tasks like showings, screenings, and paperwork adds about $395 per vacancy cycle [7].

"The true financial drain of an unoccupied property goes much deeper, creating a ripple effect that erodes your bottom line in ways you won't see on a bank statement" - Showdigs [8]

Managing vacancies effectively is crucial to maintaining steady revenue and avoiding these compounding financial hits.

How to Reduce Vacancy Loss and Stabilize Revenue

Reducing vacancy loss and stabilizing revenue requires a mix of strategic planning, financial preparedness, and operational efficiency. The focus is on minimizing both the frequency and duration of vacancies while building a safety net to handle inevitable challenges.

Diversify Your Tenant Mix and Lease Terms

A diverse tenant mix and flexible lease structures can shield your property from sudden vacancy spikes. By including tenants from different sectors and staggering lease expirations, you reduce the risk of multiple vacancies occurring at once [9].

For properties with a single large tenant, consider dividing the space into smaller units. This not only attracts a broader range of tenants but also lessens the impact of losing a major occupant [9].

Flexible leases are another game-changer. For example, graduated rents - where rent starts low and increases over time - help startups establish themselves. Shorter initial leases with renewal options also give tenants the flexibility they need. Retaining tenants is far more cost-effective than replacing them; it can cost up to five times more to acquire a new tenant when you factor in downtime, commissions, and tenant improvements [9].

"The modern lease is less a rigid contract and more a dynamic partnership agreement. Flexibility and shared incentives are the new cornerstones of tenant retention."

– 2025 Commercial Real Estate Trend Report [9]

These strategies not only reduce risk but also create a more stable financial foundation.

Build Financial Reserves and Contingency Plans

Even with a balanced tenant mix, financial preparation is critical for handling unexpected vacancies. Maintaining reserves ensures that fixed expenses like property taxes, insurance, and debt service are covered when rental income dips [3][5]. These reserves are especially important during lease-up or transition periods, helping you meet Debt Service Coverage Ratio (DSCR) requirements even when income temporarily falls below standard levels [3].

When underwriting deals, include a General Vacancy and Credit Loss factor - usually 5% to 11% of Gross Potential Income. This accounts for turnover and tenant defaults, giving you a realistic picture of your property's performance [2][3]. With most properties stabilizing at 90% to 95% occupancy, this assumption aligns with industry norms [3].

Negotiating loan covenants with built-in flexibility, such as setting thresholds slightly below expected occupancy levels, provides additional breathing room. Without adequate reserves, cash flow gaps could force reliance on high-interest loans or even trigger technical defaults, leading to greater financial strain [5].

Improve Property Management and Marketing

Strong property management and effective marketing can significantly reduce vacancy durations, complementing tenant diversity and financial planning.

"The cheapest vacancy is the one that never happens."

– HonestCasa [10]

Prompt and reliable maintenance is key to retaining tenants. In fact, 62% of tenants cite slow maintenance responses as a primary reason for not renewing their lease [10]. Setting clear standards - like responding to maintenance requests within 2 hours and resolving non-emergencies within 24 hours - can make a big difference [10].

Speed is also crucial during turnover periods. A 21-day turnover standard involves scheduling contractors and starting marketing efforts as soon as the current tenant gives notice [10]. Pre-leasing - advertising a unit 2 to 3 weeks before it becomes available - can help secure an approved tenant before the unit is even ready [10].

Marketing strategies like professional photography and virtual tours can dramatically increase visibility and interest. Listings with professional photos get 118% more views, while virtual tours boost inquiries by 87% [10]. Self-showing technology, such as smart locks, allows prospective tenants to view units at their convenience, cutting lease-up times by an average of 8 days [10]. Additionally, adopting pet-friendly policies can expand your applicant pool, as 66% of U.S. households own pets, and pet owners tend to stay in rentals longer than those without pets [10].

| Strategy | Estimated Cost | Expected Vacancy Reduction |

|---|---|---|

| Market-accurate pricing | $0 | 5–15 days |

| Pre-leasing during notice period | $0 | 10–20 days |

| 21-day turnover process | $0 | 10–25 days |

| Professional photography | $150–$400 | 3–7 days |

| Pet-friendly policy | $0 | 3–10 days |

| Self-showing technology | $150–$300 | 3–8 days |

Source: [10]

Using Financial Analysis and Technology to Address Vacancy Loss

How Financial Analysis Helps Reduce Vacancy Loss

Financial analysis taps into historical occupancy trends and payment behaviors to flag potential risks and predict vacancy scenarios[11][12]. This allows property managers to pinpoint tenants who might default or choose not to renew their leases, giving them a chance to act before problems arise.

For example, credit risk analysis looks at tenant credit scores and payment patterns to identify warning signs. Late payments or requests for deferrals often hint at financial struggles, giving you an opportunity to step in and reduce the time your property sits empty between leases[11][12].

Another tool, scenario analysis, helps you test how your property's income would hold up during market disruptions. Whether it’s losing a key tenant or facing a drop in local rental rates, modeling these scenarios prepares you to create contingency plans that safeguard your cash flow. Services like The Fractional Analyst specialize in tailored financial analysis, helping you spot vacancy risks across your portfolio early and take action before they hurt your bottom line (https://thefractionalanalyst.com).

By combining these financial insights with technology, you can refine your strategies even further.

Using Technology for Market Data and Forecasting

Technology complements financial analysis by providing real-time data and predictive tools that make managing vacancies more efficient. For instance, automated systems can instantly flag uncollected rent and cost overruns, eliminating the delays of quarterly reviews. In fact, users of automated reporting platforms are able to make decisions 30% faster compared to those relying on manual spreadsheets[5].

Integrating market data into your analysis ensures your assumptions align with the realities of nearby properties. Tools like CoreCast, The Fractional Analyst’s real estate intelligence platform, offer live rent comparisons and vacancy forecasts to guide data-driven decisions. Using roll-forward logic, CoreCast projects your property’s journey from its current occupancy level to full stabilization, which directly impacts its valuation and debt capacity[3].

Additionally, measuring economic vacancy - a broader metric than just physical vacancy - gives you a clearer picture of your property's performance. This approach helps uncover revenue leaks that might go unnoticed with traditional methods[5]. Together, these technological tools and strategies work to minimize vacancy loss and maintain steady revenue streams.

Conclusion

Understanding and addressing vacancy loss is a cornerstone of maintaining consistent revenue streams.

Vacancy loss directly impacts cash flow, property value, and compliance with lender requirements. By distinguishing between actual vacancy (what’s happening now) and general vacancy (your projected risk), you can better model and manage potential challenges. Even with full occupancy, incorporating a 5–8% vacancy allowance into your financial models adds a realistic safety net, avoiding reliance on overly optimistic scenarios [13].

Proactive planning is key to stabilizing revenue. This involves setting competitive rental prices from the start, marketing units before they become vacant, and keeping a close eye on financial metrics to avoid covenant breaches.

Comprehensive financial analysis - like credit risk assessments and scenario modeling - helps identify potential issues early. When combined with real-time market data and automated reporting tools, these strategies enable quicker, more informed decisions. Together, they form a strong foundation for maintaining steady revenue.

"The cheapest vacancy rate is zero, and the best way to achieve that is keeping your current tenants happy." - PropBrain [13]

Whether you’re managing a single property or an entire portfolio, the goal remains the same: minimize downtime, maximize occupancy, and ensure steady Net Operating Income. Tools like the Fractional Analyst's CoreCast platform provide real-time tracking of essential metrics, while their team of financial analysts delivers personalized support for underwriting, asset management, and investor reporting. By treating vacancy loss as a manageable risk, you can achieve long-term financial stability.

FAQs

How do I calculate vacancy loss for my property?

To figure out vacancy loss, here’s what you need to do:

- Collect your data: Start by gathering key pieces of information like your Gross Potential Income (GPI), historical vacancy rates, tenant payment records, and any relevant market trends.

- Determine the vacancy rate: Calculate this by dividing the number of vacant units by the total number of units. Be sure to account for factors like local market conditions and upcoming lease expirations.

- Estimate potential rent loss: Use tenant payment history to identify risks of non-payment that could add to your losses.

- Calculate the dollar amount: Multiply the vacancy rate by your GPI. This gives you the total expected vacancy loss in dollar terms.

By following these steps, you’ll have a clear picture of how much revenue you’re losing due to vacancies.

What vacancy rate do lenders consider “stabilized”?

In the U.S. real estate market, lenders generally consider a vacancy rate between 5% and 10% as acceptable or "stabilized." This range indicates a healthy balance, ensuring steady revenue and reliable asset performance.

What’s the fastest way to shorten days vacant between tenants?

The fastest way to cut down on vacancy periods is by using smart management strategies. Start by setting competitive rental prices - this means conducting market research every 6 to 12 months to stay in line with current trends. Another key step is simplifying the leasing process to avoid unnecessary delays.

On top of that, having an efficient leasing system in place and responding quickly to tenant concerns can make a big difference in reducing the time between tenants.