State-by-State Lender Title Insurance Comparison

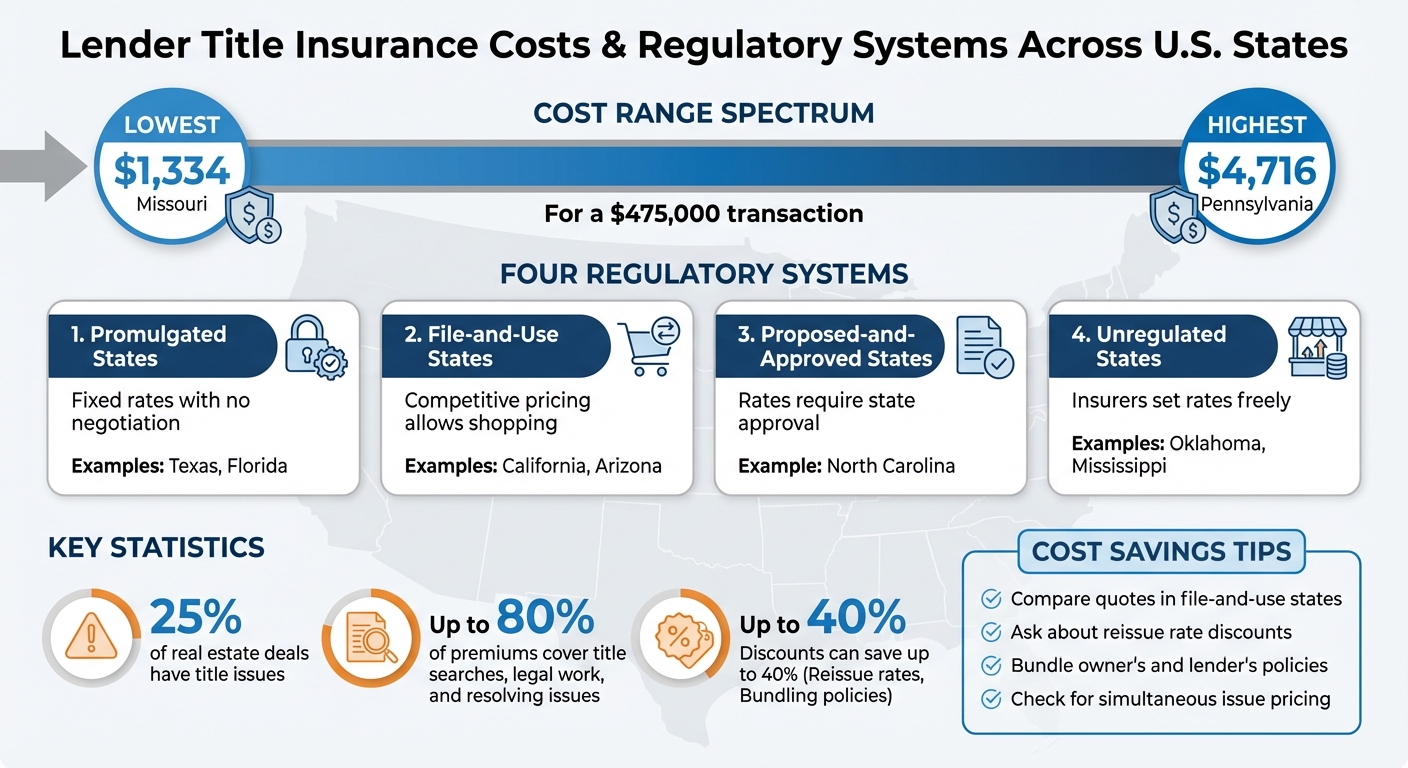

Lender title insurance costs vary significantly across the U.S., influenced by state regulations, pricing systems, and additional fees. For a $475,000 transaction, costs range from $1,334 in Missouri to $4,716 in Pennsylvania. States use one of four regulatory systems:

- Promulgated States (e.g., Texas, Florida): Fixed rates with no negotiation.

- File-and-Use States (e.g., California, Arizona): Competitive pricing allows shopping for better deals.

- Proposed-and-Approved States (e.g., North Carolina): Rates require state approval.

- Unregulated States (e.g., Oklahoma, Mississippi): Insurers set rates freely.

Key Insights:

- Title issues occur in 25% of real estate deals.

- Up to 80% of premiums cover title searches, legal work, and resolving issues.

- Discounts like reissue rates or bundling policies can save up to 40%.

Each state's system impacts costs and practices, offering opportunities to reduce expenses by understanding local rules and available discounts.

State-by-State Lender Title Insurance Cost Comparison for $475,000 Transaction

1. Alabama

Regulatory Requirements

Alabama operates under a file-and-use system, which means insurers must file rates with the Department of Insurance but can still offer flexible pricing [6]. This system gives you the opportunity to compare options and find better deals on service fees.

Under the Alabama Title Insurance Act, individual agents must either be state residents or employees of licensed agents, and agencies must be based in Alabama. However, licensed attorneys are not required to obtain agency licensing [3].

All title commitments, policies, and endorsements must include signatures along with the corresponding license numbers. Policies must also be issued within 60 days of meeting the commitment requirements and collecting the premium [3]. These rules can impact both the pricing and potential discounts you might receive.

Pricing Structures

For an average mortgage in Alabama, valued at $339,384, the cost of a standalone lender's policy is approximately $2,094, which typically falls within 0.5% to 1% of the purchase price [4][7].

Simultaneous issue pricing can lead to noticeable savings. For example, in Jefferson and Shelby Counties, you can get a lender's policy along with an owner's policy for as little as $125, plus additional fees like a $350 service fee and a $25 CPL fee [5].

If the seller already holds an owner's policy, you might qualify for a reissue rate discount. However, insurers are not obligated to offer this discount. If they do, the agent must secure a copy of the previous policy to apply the credit [3].

Mandatory Endorsements

Alabama's regulatory framework also covers standard endorsements required for lender policies. For loans closing on or after January 1, 2024, lenders will require the 2021 ALTA policy forms, provided they are approved for use in Alabama [9]. While specific endorsements depend on lender guidelines (e.g., Fannie Mae or Freddie Mac), certain ones are standard for residential transactions.

- The ALTA 8.1 endorsement offers protection against environmental "superliens" that could take precedence over a mortgage [9].

- For adjustable-rate mortgages, endorsements like ALTA 6, 6.1, or 6.2 cover risks tied to interest rate changes.

- Condominiums require an ALTA 4 endorsement, while planned unit developments need an ALTA 5 [9].

State law also sets a minimum $25 CPL fee for each party (buyer or lender) receiving closing protection when a title policy is issued. For sellers transferring title without a loan policy, the fee increases to at least $50 [10]. Additionally, when a lender's policy is issued during a purchase transaction, the insurer or agent must notify the buyer in writing about the option to purchase owner's title insurance.

sbb-itb-df8a938

How Much Does Title Insurance Cost?

2. Alaska

Alaska follows a filed rates system similar to Alabama's file-and-use framework, creating a competitive environment for title insurance providers.

Regulatory Requirements

In Alaska, insurers are responsible for filing their rate schedules and policy forms for state approval [1][11]. Unlike states with uniform, state-mandated pricing, this approach allows for competition, leading to price differences among providers.

Before issuing a policy, insurers must assess insurability through a thorough title search and examination [11]. They are required to own or lease a title plant that meets district standards. Additionally, offering rebates is prohibited under AK Stat § 21.66.310 [11]. This regulatory model highlights the competitive nature of Alaska's market compared to states with fixed pricing.

Pricing Structures

For a typical mortgage of $246,007, the cost of a lender's title insurance policy is approximately $1,601, which aligns with the typical 0.5% to 1% range of the home's sale price [12]. Since insurers set their own rates, prices can vary significantly - often by $300 to $500 between providers [1].

| Property/Loan Value | Base Rate | Additional Cost (per $1,000) |

|---|---|---|

| $200,000 – $500,000 | $882 | $3.00 |

| $500,001 – $750,000 | $1,782 | $2.50 |

| $750,001 – $2,000,000 | $2,407 | $2.00 |

Purchasing both an owner's and lender's policy from the same company often qualifies for a simultaneous issue discount, which can lead to substantial savings [1][12]. Additional costs include title searches ($60–$200) and land surveys ($200–$800) [12].

Beyond the base pricing, endorsements play a key role in defining the scope of coverage for policies in Alaska.

Mandatory Endorsements

While Alaska does not require specific endorsements for every transaction, lenders typically insist on policies that ensure a valid and enforceable lien on the property [13]. For instance, a lender's policy protects against losses stemming from issues like the invalidity or unenforceability of a deed of trust [13].

The ALTA 49 endorsement, introduced in August 2025, provides coverage for post-closing forgery and adds $50–$150 to the premium. Adoption of this endorsement is still ongoing across the state [1]. Enhanced policies, which offer coverage for up to 33 risks, generally come at a premium of 10% to 20% more than standard ALTA policies [1][12].

3. Arizona

Arizona operates as a market-based state, meaning insurers file their rates with the Department of Insurance, enabling a competitive pricing environment [15][1]. This approach differs from states like Texas and Florida, where rates are standardized and regulated [15][1]. Title insurers in Arizona must submit all policy forms and contracts to the Director of Insurance at least 30 days before they are issued [14].

Regulatory Requirements

In Arizona, only companies that are members of the American Land Title Association (ALTA) are permitted to issue title insurance [17]. Additionally, escrow agents are required by law to inform buyers and sellers in residential transactions about the availability of a Closing Protection Letter (CPL). The fee for this letter is capped at $25 and offers protection against escrow fund losses caused by fraud or dishonesty on the part of the agent [16].

Unlike "Attorney States" such as Georgia or South Carolina, where attorneys oversee real estate closings, Arizona is a "Title Company State." Here, title companies handle both escrow and title services [15]. For properties purchased with a mortgage, a lender's policy is mandatory and cannot be excluded from the closing costs [17][18].

These regulatory requirements shape the pricing structures for lender's policies in Arizona.

Pricing Structures

In Arizona, the cost of a lender's title insurance policy is a flat $315 when purchased alongside an owner's policy, regardless of the home's value [17][18]. For a standalone lender's policy, the cost averages $1,432 based on the state's average mortgage amount of $213,787 [19]. Owner's policies, however, follow a tiered pricing model. For example:

- A $300,000 property incurs a cost of approximately $1,335.

- A $1,000,000 property costs $3,025, with an additional $16.50 charged for every $10,000 above that threshold [18].

Title insurance plays a critical role in resolving issues, addressing problems in about 25% of real estate transactions before closing [1]. Additional fees include:

- Title searches: $100–$300

- Escrow fees: Around $2 per $1,000 of the property sale price

- Deed preparation: $250–$500 [19]

Mandatory Endorsements

Lender policies in Arizona often include endorsements to address specific risks. While the state doesn't require endorsements for every transaction, lenders commonly request coverage for concerns like environmental protection liens, priority assessments, and ensuring the property has access to a public street [20].

The ALTA 49 endorsement, introduced in August 2025, offers protection against post-closing forgery and deed fraud. This endorsement typically adds $50–$150 to the policy premium [1].

A noteworthy legal decision in July 2025 further clarified lender policy coverage. In Centerpoint Mechanic Lien Cls., LLC v. Commonwealth Land Title Ins. Co., the Arizona Supreme Court ruled that lender policies provide no coverage if the insured loan is fully repaid. The case involved a $165 million construction loan with $30 million in mechanics' liens. The court determined that, under ALTA loan policy terms, no actual loss occurred because the lenders were reimbursed through a complex transaction [21]. This decision underscores that lender coverage is strictly limited to the amount of unpaid, unreimbursed debt.

4. Arkansas

Arkansas operates as a filed rate state, meaning insurers set their rates and file them with the Insurance Department at least 20 days before they take effect. This system blends regulatory oversight with market-based pricing strategies, similar to other states.

Regulatory Requirements

The Arkansas Title Insurance Act requires a thorough 30-year search of public records to ensure a detailed review of any title issues. As noted by the Arkansas Insurance Department:

"No title insurance report or policy shall be issued unless the insurer or agent has made a search of all matters affecting the title to the property for a continuous period of not less than the immediately preceding thirty years." [22]

Title agents in Arkansas need to meet stringent requirements. They must complete 2,000 hours of title work, pass a written exam (with no exceptions for attorneys), and complete six hours of continuing education annually, including one hour focused on ethics. Title insurers are also required to perform yearly on-site audits of their agencies. Additionally, both insurers and agencies must retain their records for seven years.

State law ensures that agencies offer Closing Protection Letters (CPLs) to all involved parties - buyers, sellers, and lenders. Written consent must be obtained, and CPL fees are required to be filed with the Commissioner at least 20 days before they can be used. [22]

Pricing Structures

For a standalone lender’s policy on Arkansas’s average mortgage of $432,075, the cost is approximately $2,582 [24]. However, when paired with an owner’s policy, the lender’s policy fee typically drops to a flat rate ranging from $50 to $200 [23]. The state’s pricing structure charges $3.50 per $1,000 for properties valued up to $100,000 and $2.00 per $1,000 for amounts between $100,000 and $5,000,000 [23][24].

For example:

- A $500,000 policy costs $1,072 for Standard Loan coverage versus $1,340 for Expanded Loan coverage - about 25% higher.

- A $1,000,000 policy is priced at $1,947 for Standard coverage and $2,434 for Expanded coverage [25].

5. California

California uses a filed rate system for title insurance, meaning companies must submit their rate schedules to the California Department of Insurance (CDI) for approval [26]. This differs from states like Texas or Florida, where fixed rates apply across all companies [1].

Regulatory Requirements

The CDI requires title insurers to obtain a Certificate of Authority and maintain a minimum $50,000 surety bond [26]. Escrow service providers must keep funds in separate accounts and preserve transaction records for at least five years. Additionally, California title companies must adhere to the California Consumer Privacy Act (CCPA) and the California Financial Information Privacy Act (FIPA) [26]. These regulations directly influence the state's competitive pricing structure.

Pricing Structures

In California, the cost of a standalone lender's policy averages $2,132 for a $346,762 mortgage [27]. However, when purchased alongside an owner's policy, the lender's policy typically drops to a flat fee of about $110. Nearly 90% of real estate transactions in California in 2024 included both policies [28][29].

The state employs tiered pricing based on property value. For properties valued up to $10,000,000, the rate is $0.75 per $1,000, while properties valued between $10,000,000 and $20,000,000 are charged $0.65 per $1,000 [27]. About 80% of premiums are allocated to pre-closing tasks like title searches, examinations, and curative services, with the remaining 20% reserved for claims. Additional fees may include title search costs ($150–$500), settlement fees ($200–$600), and land surveys ($200–$800) [1]. This pricing approach reflects California's diverse regulatory landscape and emphasizes the importance of state-specific analysis.

Mandatory Endorsements

Lenders often require specific endorsements to ensure comprehensive protection. For instance, the Environmental Protection Lien endorsement (ALTA 8.1/8.2) protects against lien priority loss due to recorded environmental liens [31], while the Variable Rate endorsement (ALTA 6.0) ensures the lender's lien retains priority if loan terms change [31]. Extended coverage policies are also common, offering additional protection against off-record issues such as easements, encroachments, and boundary line disputes [30].

California stands out as one of the few states that uses its own state-promulgated forms (CLTA) alongside standard ALTA forms [31]. In August 2025, the ALTA 49 endorsement for post-closing forgery was introduced and began rolling out statewide in early 2026 [1].

6. Colorado

Colorado uses a filed rate system for title insurance, meaning each company submits its rates and discounts to the Colorado Division of Insurance. This setup allows for noticeable price differences, giving buyers and sellers the chance to compare options and potentially save money [1] [35].

Regulatory Requirements

Colorado has specific regulations shaping its title insurance process. The Colorado Division of Insurance mandates that title insurance companies publicly file their rates for transparency. Additionally, a lender’s title insurance policy is required for all real estate transactions involving financing, ensuring the bank’s interest in the property is protected [33] [34]. Title companies must conduct a thorough public records search and issue a title commitment [33].

“A lender's policy is always required when financing is involved, to protect the bank's interest in the property.” – Jerad Larkin, Chicago Title Colorado [33]

The state’s regulatory framework also addresses unique risks tied to Colorado's geography and history. For instance, the complex water rights under the prior appropriation doctrine, severed mineral rights, and mining claim histories present specific challenges. Title insurance generally excludes coverage for water rights disputes, which require separate verification [34]. These distinctive issues highlight the importance of Colorado’s detailed title search protocols.

Pricing Structures

Title insurance premiums in Colorado are calculated based on a rate per thousand dollars of the property’s purchase price [1] [36]. For instance, an owner’s policy for a $420,000 home costs approximately $1,427. When both an owner’s and lender’s policy are issued simultaneously, the lender’s fee can drop to around $175 [37]. For a typical mortgage of $448,975, the lender’s policy costs about $2,671 [39].

Pre-closing work is a major factor in these costs. Title insurance helps resolve issues in about 25% of real estate transactions before the closing date [1]. While it’s customary for sellers to pay for the owner’s policy and buyers to cover the lender’s policy, this can be negotiated in the purchase agreement [34] [36].

Mandatory Endorsements

Colorado law doesn’t require specific endorsements for all policies, but mortgage lenders often insist on certain endorsements to meet secondary market requirements, such as those set by Fannie Mae and Freddie Mac [32] [38]. Common lender-required endorsements include:

- ALTA 9 (Survey/Comprehensive)

- ALTA 4 (Condominium)

- ALTA 5 (Planned Unit Development)

- ALTA 8.2 (Environmental Protection Lien)

These endorsements generally cost between $25 and $200. Starting in early 2026, the ALTA 49 endorsement for post-closing forgery coverage will be available, adding $50 to $150 to the premium [1] [38]. These endorsements ensure that lender coverage aligns with state practices.

Coverage Limits

Colorado’s coverage limits are designed to adapt to the changing nature of mortgage financing. Lender’s title insurance coverage is capped at the loan amount and decreases as the mortgage is paid off [34]. For refinancing, homeowners may qualify for reduced "refinance rates" if they’ve owned the property for several years [32]. Buyers should ask about simultaneous issue discounts when purchasing both owner’s and lender’s policies. Additionally, discounts like "short-term" or "reissue" rates may apply if a previous policy was issued within the last five years [35] [37].

7. Connecticut

Connecticut takes a unique approach to title insurance, blending legal expertise with the standard processes. In this state, title agents must be practicing attorneys, a requirement in place for all agents licensed after June 12, 1984. This ensures that legal oversight is built into the title examination process, making Connecticut stand out among other states that simply focus on filing and competitive rates [40][41]. This legal framework emphasizes precision and accountability in title work.

Regulatory Requirements

Connecticut enforces several strict regulations to ensure transparency and consumer protection in title insurance:

- Before issuing a lender's policy, insurers are required to conduct a thorough title search and confirm insurability. Records of this process must be kept for 10 years [40][44].

- Agent commissions are capped at 60% of the gross premium, which is lower than in many other states [40][45].

- For residential loans, insurers must issue Closing Protection Letters (CPLs) to safeguard lenders against agent misconduct [43].

- If a lender’s policy is issued without an owner’s policy, agents must provide borrowers with a written notice explaining that the lender’s policy does not protect them personally. Failure to comply can lead to fines of up to $15,000 [41].

These regulations not only ensure a higher level of consumer awareness but also contribute to Connecticut's competitive pricing structure.

Pricing Structures

As a filed rate state, Connecticut mandates that insurers submit their premium schedules to the Insurance Commissioner [40][41]. Title insurance costs typically range from 0.5% to 1% of the home’s sale price [42]. For a mortgage averaging $414,090, the lender’s policy costs about $2,487 [42].

Here’s a breakdown of rates per $1,000 for different property value ranges:

| Property Value Range | Rate per $1,000 |

|---|---|

| $20,001 – $100,000 | $4.36 |

| $100,001 – $200,000 | $4.09 |

| $200,001 – $500,000 | $3.54 |

| $500,001 – $5,000,000 | $3.00 |

| $5,000,001 – $10,000,000 | $2.45 |

Refinancing may qualify for discounted or reissue rates if the previous policy is less than 10 years old [41]. Buyers who purchase both owner’s and lender’s policies simultaneously often benefit from a simultaneous issue discount [41][1]. Additional fees include title search costs, which typically range from $100 to $150, and settlement fees averaging around 0.26% of the sale price [42].

Coverage Limits

In Connecticut, lender’s title insurance coverage is limited to the loan amount and decreases as the mortgage balance is paid down [41][45]. Additionally, the state enforces a single risk limitation: a title insurer’s net retained liability for any single risk cannot exceed 50% of its total surplus and reserves [40]. This rule protects both insurers and policyholders by minimizing financial exposure on individual transactions.

8. Delaware

Delaware operates as a filed rate state, meaning companies submit rate schedules to regulators, which can lead to variations in pricing [47][1]. Lender's title insurance is required for all mortgage-backed transactions in the state, ensuring the lender's investment is protected throughout the life of the loan [47]. Below, we’ll break down Delaware’s regulatory framework, pricing tiers, mandatory endorsements, and coverage limits.

Regulatory Requirements

Delaware’s regulations prioritize transparency and consumer protections, as is typical for filed rate states. According to state law, lenders must accept a written binder as proof of insurance if it includes specific details: names and addresses of the borrower and lender, a property description, a 10-day cancellation notice, a paid receipt, and the coverage amount [46]. These rules apply to mortgages for consumer purposes, which are liens on residential properties with one to four units [46].

There are also strict limits on hazard insurance requirements. Lenders cannot demand coverage that exceeds the value of the property improvements, as determined by the insurer or through the lender’s appraisal [46]. Violations carry steep penalties - lenders must pay the borrower’s reasonable attorney fees and the greater of actual damages or 5% of the mortgage’s face value [46]. The Delaware Title Insurance Rating Bureau (DTIRB) oversees rate and form filings in the state [49].

These regulations form the foundation for Delaware's pricing structures.

Pricing Structures

Title insurance costs in Delaware generally range between 0.5% and 1% of the sale price [47]. For example, on an average mortgage of $324,690, the lender’s policy would cost approximately $2,016 [47]. Delaware’s pricing model is tiered, with rates per thousand dollars decreasing as the total liability increases:

| Liability Amount | Rate Per $1,000 |

|---|---|

| Up to $100,000 | $4.60 |

| $100,001 to $1,000,000 | $3.90 |

| $1,000,001 to $5,000,000 | $3.25 |

| $5,000,001 to $10,000,000 | $2.25 |

| Over $10,000,000 | $1.65 |

For refinancing, lower rates often apply. For instance, a refinance policy might cost $1.50 per $1,000 for the first $100,000, compared to $2.50 per $1,000 for a standard loan policy [48]. Additionally, buyers can save money by purchasing both an owner’s and lender’s policy at the same time, thanks to a simultaneous issue discount [1]. Because Delaware allows competitive pricing, borrowers are encouraged to shop around and gather at least two quotes, which could result in significant savings [1].

Mandatory Endorsements

As of April 1, 2025, Delaware uses updated DTIRB-approved forms and endorsements [49]. While state law doesn’t explicitly require specific endorsements for every transaction, lenders often insist on endorsements to protect against certain risks. Common examples include:

- Construction loan endorsements (DTIRB-92 and DTIRB-95)

- Future advance endorsements (DTIRB-29)

- Zoning endorsements (DTIRB-26) [49]

Delaware has also introduced a new ALTA Short-Form Expanded Coverage Residential Loan Policy, effective April 1, 2025. This policy simplifies the process by bundling standard endorsements for one-to-four family residential properties [49].

Coverage Limits

In Delaware, a lender’s title insurance policy remains valid for the entire term of the loan [47]. However, the coverage amount decreases as the mortgage is paid down, only covering the remaining loan balance [47].

9. Florida

Florida has a fixed-rate system for title insurance, regulated by the Florida Office of Insurance Regulation (OIR). This means agencies must strictly follow the rates approved by the OIR. When it comes to lender's title insurance, it’s usually required for most mortgages to protect the lender's financial interest until the loan is either paid off or refinanced. Who pays for what? That depends on the county. In many counties, the seller covers the cost of the owner's policy. However, in counties like Miami-Dade, Broward, Palm Beach, Collier, and Sarasota, the buyer typically picks up the tab [51].

Regulatory Requirements

The Florida Department of Financial Services (DFS) handles licensing and compliance, while the OIR is responsible for setting premium rates. Title agents must ensure escrow accounts are reconciled with bank statements and records [53]. Florida law also requires that charges like title searches, examination fees, and closing costs are listed separately from the risk premium on the closing statement [54]. Mortgage title insurance policies must cover at least the full principal debt and can go up to 125% to account for interest and foreclosure costs [54]. These rules directly influence Florida's tiered pricing system.

Pricing Structures

Florida uses a tiered rate system that adjusts based on the loan amount or purchase price [54]:

| Liability Amount | Rate per $1,000 |

|---|---|

| First $100,000 | $5.75 |

| $100,001 to $1,000,000 | $5.00 |

| $1,000,001 to $5,000,000 | $2.50 |

| $5,000,001 to $10,000,000 | $2.25 |

| Over $10,000,000 | $2.00 |

Premiums typically range from $500 to $3,500, which is about 0.5% to 1% of the property’s purchase price [50][55]. If a lender's policy is issued alongside an owner’s policy, there’s an additional $25 fee [54]. Refinancing might qualify for discounted substitution loan rates - 30% of the original rate if the loan is three years old or less [54]. Additionally, properties insured within the last three years may be eligible for reissue credits, offering up to a 40% discount [50].

Coverage Limits

Lender's title insurance in Florida covers the outstanding loan balance, decreasing as payments are made. The policy expires when the loan is paid off or refinanced. On the other hand, an owner's policy stays in effect as long as the owner or their heirs retain an interest in the property [52][55]. For all conveyances, the minimum premium is $100, except in cases of multiple conveyances on the same property, which are charged $60 [54].

10. Georgia

In Georgia, insurance companies operate under a filed rate system. This means insurers submit their rates to the Office of Commissioner of Insurance and Safety Fire, allowing for competitive pricing. As a result, buyers can compare quotes and potentially save between $300 and $500. While lenders almost always require a lender's policy as part of the mortgage process, state law does not require title insurance.

Regulatory Requirements

The Georgia Office of Commissioner of Insurance and Safety Fire regulates the title insurance industry, overseeing policy forms and premium rates. Title insurers must maintain a guaranty fund (also known as an unearned premium reserve) equivalent to 10% of the total risk premiums written annually. This reserve decreases by 5% each year over a 20-year period [57]. Georgia also uses updated ALTA forms approved in 2017, aligning them with the 2006 ALTA policies for better clarity [58].

Under GA Code § 33-7-8.1, title insurers may issue Closing Protection Letters (CPLs) only for transactions where they are also issuing a title insurance policy and their agent is responsible for handling settlement funds [56]. These CPLs protect lenders from losses caused by fraud, theft, or negligence by the settlement agent, up to the settlement fund amount. The premiums for CPLs must be filed with and approved by the Commissioner, and agreements to split these premiums are prohibited.

These regulations contribute to Georgia's tiered pricing structure, which is outlined below.

Pricing Structures

Georgia uses a tiered system for pricing title insurance, with rates determined by property value. The standard ALTA pricing is as follows [59][60]:

| Property Value | Rate per $1,000 |

|---|---|

| Up to $100,000 | $4.20 |

| $100,001 to $500,000 | $3.65 |

| $500,001 to $1,000,000 | $3.10 |

| Above $1,000,000 | $3.00 |

Simultaneous issue pricing offers significant savings. For example, when purchasing a lender's policy alongside an owner's policy, the lender's policy costs a flat fee of $150. The minimum premium for any policy is $200, and title insurance typically ranges between 0.5% and 1% of the home's sale price. For instance, with Georgia's average mortgage of $331,030, a standalone lender's policy might cost around $2,132, but with simultaneous issuance, the cost drops to just $150 [59][60].

According to ALTA, title insurance processes resolve issues in about 25% of real estate transactions before closing [1].

Mandatory Endorsements

Georgia does not require specific endorsements for every lender's policy. Instead, lenders select from ALTA forms approved by the Commissioner, based on the risks of the transaction [58][59]. Common endorsements include:

- ALTA 9.6.1-06 – Protects against losses if private rights in a covenant impact the mortgage.

- ALTA 45-06 – Designed for "Pari Passu" mortgages, ensuring co-equal lien priority.

- ALTA 18.2-06 – Covers multiple tax parcels.

In early 2026, the ALTA 49 endorsement - offering protection against post-closing forgery - began rolling out after its release in August 2025 [1].

Coverage Limits

A lender's title insurance policy covers the outstanding loan balance, and the coverage decreases as the loan is repaid. The policy ends once the loan is paid in full or refinanced. Enhanced Homeowner's Policies provide broader coverage, protecting against roughly 33 risks compared to the 12 risks covered by standard ALTA policies. These enhanced policies generally cost 10% to 20% more [1].

In Georgia, buyers typically pay for both the lender's and owner's policies, though this can be negotiated in the real estate contract [1][59]. Like other states using a filed rate system, Georgia ensures that lender policies decrease in coverage as the loan balance is reduced, maintaining consistency in coverage limits.

11. Hawaii

Hawaii operates as a filed rate state, meaning title insurance companies set their own rates with regulators rather than adhering to fixed state pricing. This creates competition among providers, giving buyers the chance to shop around for the best deal - a benefit for those involved in commercial real estate financing [1][62].

In Hawaii, lender's title insurance is a required part of mortgage loans, ensuring the lender's investment is protected from potential title defects. Unlike many states that rely on a deed of trust, Hawaii uses a mortgage as its main security instrument, which affects how liens are recorded and enforced [61][62]. Title insurance premiums in the state generally range from 0.5% to 1% of the home's sale price. For example, with an average mortgage of $345,963, a lender’s policy costs about $2,128 [62]. This regulatory framework directly influences both pricing and coverage, as detailed below.

Pricing Structures

Hawaii's rate-filing system encourages competition among title insurance providers. Here's a breakdown of typical costs based on property value [62]:

| Property Value | Estimated Cost |

|---|---|

| $100,000 – $200,000 | $585 – $935 |

| $300,000 – $400,000 | $1,395 – $1,755 |

| $600,000 – $700,000 | $2,495 – $2,790 |

| $800,000 – $900,000 | $3,010 – $3,355 |

| $1,000,000 – $2,000,000 | $3,635 – $5,605 |

When both lender's and owner's policies are purchased at the same closing, simultaneous issue discounts can help reduce costs significantly. Buyers typically pay for the lender's policy, while the cost of the owner's policy is often subject to local negotiation [62][64]. Additional fees, such as title searches ($60–$200), deed preparation ($50–$200), and land surveys ($300–$800), may also apply [62]. These extra costs, common across many states, highlight the importance of evaluating the full expense.

Coverage Limits

Understanding what a policy covers is just as important as knowing its cost. A lender's title insurance policy covers the outstanding loan balance and ends when the loan is paid off or refinanced. In Hawaii, each loan instrument requires its own policy, meaning a new policy is necessary with every refinance [64].

Standard ALTA policies protect against 12 pre-closing risks, while Enhanced Homeowner's policies extend coverage to 33 risks, including post-closing issues like building permit violations. These enhanced policies typically cost 10% to 20% more [1][62]. Additionally, the ALTA 49 endorsement, which offers protection against post-closing forgery, began rolling out in early 2026 [1].

For a deeper dive into how these pricing structures and coverage details influence commercial real estate financing, real estate professionals can explore specialized insights at The Fractional Analyst (https://thefractionalanalyst.com).

12. Idaho

Idaho operates as a filed rate state, meaning title insurance companies determine their own rates and submit them to the Department of Insurance instead of adhering to state-mandated pricing [68]. This system fosters competition, making Idaho one of the most affordable states for title insurance. The average standard premium here is $370, ranking as the third-lowest in the country [2]. This affordability can significantly reduce costs in commercial real estate deals.

Although Idaho law doesn't require title insurance, lenders almost always insist on a lender's policy as part of loan conditions [67]. According to the Idaho Department of Insurance:

Title Insurance is not required in the state of Idaho. However, your lender may require you to purchase a Title Insurance Lender's Policy to protect their interests [67].

For a typical Idaho mortgage of $201,143, a lender's policy costs about $1,365 [70]. These competitive rates are upheld by a strong regulatory framework, outlined below.

Regulatory Requirements

The Idaho Department of Insurance enforces strict rules for title insurance operations. Insurers cannot issue policies on Idaho properties without obtaining a certificate of authority and adhering to state insurance laws [65]. Additionally, all policy forms, preliminary reports, and binders must be submitted to the Director before issuance [65].

Title insurance agents must carry a surety bond of at least $10,000 for each county where they are licensed. If they employ additional escrow officers, an extra $10,000 bond is required for each officer, up to a maximum of $50,000 [66]. Agents are also required to file their escrow rates annually by March 15, with those rates becoming effective on April 15. They must also report any criminal or administrative actions to the Idaho Department of Insurance within 30 days [66].

Pricing Structures

Premium rates in Idaho cover the title examination and policy issuance, including preliminary reports. These rates start at a base level and increase in $1,000 increments [68]. Discounts are available under certain conditions, such as a simultaneous issue discount, where the lender's policy is offered at a reduced rate for any portion of coverage that overlaps with the owner’s policy [68]. Additionally, a reissue rate - up to 50% off the basic rate - may apply if a new policy is ordered within two years of a previous one [68].

| Property Value / Loan Amount | Estimated Cost |

|---|---|

| $25,000 – $250,000 | $319 – $1,161 |

| $251,000 – $500,000 | $1,164 – $1,822 |

| $501,000 – $750,000 | $1,822 – $2,442 |

| $751,000 – $1,000,000 | $2,444 – $3,062 |

| Above $1,000,000 | $3,062 + $1.87 per $1,000 |

Coverage Limits

A lender's policy in Idaho must provide coverage equal to at least the full principal amount of the loan [68]. Additional coverage - up to 20% - may be included to account for interest and foreclosure costs [68]. If the land secures only a portion of the loan, coverage is limited to the lesser of the land's unencumbered value or the loan amount [68].

Idaho law offers strong protections for consumers when it comes to claims. Under Idaho Code section 41-1839, insurers may be held responsible for reasonable attorney's fees if they fail to pay a valid claim within 30 days after receiving proof of loss [69]. Generally, a lender's policy liability ends once the mortgage is fully paid or satisfied, unless the insured acquires the property through foreclosure or a trustee's sale [69].

13. Illinois

Illinois operates under a filed rate system, where title insurance providers set their own rates rather than adhering to fixed, state-mandated prices [1]. On average, the standard title insurance premium in Illinois is about $1,130, while enhanced coverage averages around $1,430 [2]. For a property valued at $300,000, the cost of an owner's policy typically ranges between $800 and $1,200 [1]. This market-driven approach highlights Illinois' alignment with broader national regulatory trends.

Regulatory Requirements

In 2025, regulatory oversight for title insurance in Illinois transitioned from the Department of Financial and Professional Regulation to the Department of Insurance, following the enactment of Senate Bill 2648. This change brought Illinois' practices more in line with national standards [72]. Rick Young of Plymouth Title Insurance commented:

The transfer of regulatory authority to the Department of Insurance introduces important compliance adjustments for Illinois title insurance companies... companies now align more closely with national practices [72].

Illinois law requires Closing Protection Letters (CPLs) for residential transactions involving title agents who manage escrow duties [71]. Under 215 ILCS 155/16.1, these letters protect lenders, buyers, and sellers from losses due to escrow agent fraud, dishonesty, or failure to follow closing instructions. However, coverage is limited to actual losses, not exceeding the settlement funds deposited [71]. Additionally, the state enforces a "good funds" provision under Section 26 of the Illinois Title Insurance Act, ensuring that escrow disbursements are backed by verified and secure funds [72].

Title companies in Illinois are also required to maintain a statutory premium reserve of $0.125 per $1,000 of net retained liability, with 10% of added reserves released annually over a five-year period [73].

Pricing Structures

The competitive filed rate system in Illinois allows consumers to save significantly by comparing rates among providers [1]. When both lender's and owner's policies are purchased at the same closing, a simultaneous issue discount can greatly reduce the cost of the lender's policy [1]. Typically, the seller pays for the owner's policy, while the buyer is responsible for the lender's policy as part of their closing costs [1][74].

Starting in 2026, the ALTA 49 endorsement, which addresses risks such as post-closing forgery and deed fraud, became available. Adding this endorsement increases the premium by around $50 to $150 [1]. Enhanced policies generally cost 10–20% more than standard policies [1].

14. Indiana

Indiana follows a filed rate system regulated by the Indiana Department of Insurance (IDOI). Title insurers in the state are required to submit all policy documents to the IDOI at least 30 days before their intended effective date [75]. If the commissioner does not issue a disapproval within this 30-day period, the filing is automatically approved [75].

Regulatory Requirements

Indiana stands out for its Title Insurance Consumer Comparison Tool, a helpful online resource that allows buyers to compare rates from all approved insurers in the state [75][76]. This tool must be updated within 10 business days whenever new or revised filings are approved [75]. By making these rates easily accessible, Indiana gives buyers the ability to make informed decisions about title insurance [75][76]. Although an owner's policy is optional in Indiana, lenders typically require title insurance to safeguard against risks such as unpaid mortgages, outstanding taxes, undisclosed easements, child support liens, or claims from missing heirs [77][79][80].

In a standard residential transaction, it’s common to see two or three endorsements, depending on the specific requirements of the mortgage [76]. The lender's policy coverage matches the loan amount and decreases as the loan is paid off, ending entirely once the loan is fully paid [77][79][80]. These regulatory measures contribute to the competitive pricing environment in Indiana.

Pricing Structures

Indiana’s regulatory framework supports competitive title insurance rates. For example, an owner's policy on a $200,000 property costs approximately $545, while a standalone lender's policy for an average mortgage of $278,175 runs about $1,771. However, buying both policies together significantly reduces the lender's policy cost to just $50 [78][81]. On average, title insurance premiums in Indiana fall between 0.5% and 1% of the home's sale price [81].

The state also offers a simultaneous issue discount, which lowers the lender's policy cost to $50 when purchased alongside an owner's policy [78]. Buyers should also ask about reissue discounts if an owner's policy was issued within the last 10 years [76]. Additional costs, such as fees for a Closing Protection Letter and endorsements, may apply [76]. While these fees are negotiable, it’s common in Indiana for buyers to cover both the owner's and lender's policies. In some cases, however, local practices may require the seller to pay for the owner's policy [78].

15. Iowa

Iowa takes a distinctive approach by prohibiting private commercial title insurance [85][87]. Instead, the state relies on Iowa Title Guaranty (ITG), a not-for-profit division of the Iowa Finance Authority [83]. Through this system, lenders receive a "Lender's Certificate", which ensures the title's legality and the mortgage's validity [83]. This method simplifies the title process and keeps costs low for residents.

Regulatory Requirements

Iowa uses an abstract-plus-attorney-opinion model [82][84]. This involves creating a written history (abstract) of the property, which is then reviewed by a participating attorney to determine if the title is insurable [82][84]. This thorough process has earned Iowa a reputation for having the "cleanest title in the country" [89]. Additionally, title insurance agents in Iowa must carry errors and omissions (E&O) insurance and fidelity coverage when managing escrow or security deposits [82]. The state supports this system with a network of 1,261 participating attorneys, abstractors, and independent closers [90].

Pricing Structures

Iowa's pricing model is straightforward and affordable. For residential properties valued up to $750,000, the cost of a lender's certificate is $175 [84][85][88]. If the property exceeds $750,000, fees are calculated at $1 per $1,000 of the property's value [84][88]. For properties under $750,000, an owner's certificate is included at no extra charge when issued alongside the lender's certificate [83][85][88].

"For a residential transaction under $750,000, our policy is $175, and that covers both the owner and lender" [85][87].

Additional costs include title searches ($200–$440), deed preparation ($50–$200), and closing fees ($200–$400) [84][86]. In 2024, ITG processed $15.4 billion in residential real estate transactions [85]. These low fees highlight Iowa's focus on keeping residential transaction costs manageable.

| Property Value | Lender's Certificate Cost |

|---|---|

| Up to $750,000 | $175 flat fee (owner's certificate is free with the lender's) |

| Over $750,000 | $1 per $1,000 of property value |

Mandatory Endorsements

Iowa does not require specific endorsements by law, but ITG includes standard endorsements and Closing Protection Letters (CPLs) at no extra cost [83]. Additionally, ITG provides modified versions of ALTA endorsements designed specifically for title guaranty certificates, rather than traditional insurance policies [91]. Thanks to the abstract and attorney review process, which resolves title issues before closing, Iowa typically requires fewer endorsements compared to other states [89].

16. Kansas

Kansas follows a filed-rate system, requiring title insurance companies to submit their rates and charges to the Kansas Department of Insurance for public review [92]. However, there’s an exception: title agents or agencies operating exclusively in counties with populations under 10,000 are not obligated to file their rates with the Department [92]. This approach reflects the state's mix of rural and urban areas, creating a dual regulatory framework.

Regulatory Requirements

In Kansas, lender's title insurance is required for mortgage transactions, while owner's policies are optional [93]. The state uses the 2021 ALTA title insurance forms and endorsements as the standard for real estate transactions [94][31]. Additionally, Kansas permits Attorney Opinion Letters (AOLs) as a more affordable alternative to title insurance, though these carry increased risks for lenders [93]. For lender’s policies, coverage decreases as the mortgage loan balance is paid down [93].

Pricing Structures

The cost of title insurance in Kansas generally ranges between 0.5% and 1% of the home's sale price [93]. For a typical Kansas mortgage of $236,009, the estimated cost for a lender's policy is about $1,549 [93]. Buyers can save by bundling owner's and lender's policies through the same provider, often qualifying for a simultaneous issue discount [93]. Other closing costs include deed preparation ($50–$200), land surveys ($200–$800), and escrow fees ($200–$400) [93].

| Housing Price Range | Estimated Title Insurance Cost |

|---|---|

| $50,000 – $250,000 | $470 – $1,040 |

| $250,000 – $500,000 | $1,040 – $1,570 |

| $500,000 – $750,000 | $1,570 – $1,860 |

| $750,000 – $1,000,000 | $1,860 – $2,140 |

Mandatory Endorsements

Kansas doesn’t impose specific endorsements by law, but lenders often require certain ALTA endorsements to meet lending standards, especially for SBA-guaranteed loans or secondary market requirements [31]. Common endorsements include:

- ALTA 8.1 or 8.2 (Environmental Protection Lien)

- ALTA 9 series (Restrictions, Encroachments, and Minerals)

- ALTA 6 (Variable Rate Mortgage) [94][31]

Kansas also offers a state-specific "Arbitration Endorsement - Standard" [94]. These endorsements, which enhance the base policy, are typically added for a small additional cost [31].

17. Kentucky

Kentucky operates as a filed-rate state, meaning title insurance companies submit their rates to state regulators while maintaining the ability to set competitive prices [1]. This setup gives consumers the opportunity to shop around and compare rates, unlike fixed-rate states such as Texas or Florida. In Kentucky, lender's title insurance is required for most mortgage transactions, ensuring the lender’s investment is protected against unforeseen claims [95][97]. The insurer’s liability decreases over time as the mortgage balance is paid down [97].

Regulatory Requirements

Kentucky follows standard ALTA title insurance forms for real estate transactions. The lender's policy stays active for the life of the loan [97]. While lender's insurance is mandatory, owner's title insurance is optional but strongly recommended to protect the buyer’s equity [95][97]. The state also requires attorney involvement in real estate transactions, countersignatures on policies, and thorough title examinations [96].

Interestingly, about 80% of the title insurance premium goes toward pre-closing tasks like title searches and resolving potential issues, while the remaining 20% is allocated to the insurance reserve for future claims [1]. These regulations contribute to the competitive pricing environment in Kentucky.

Pricing Structures

In Kentucky, title insurance typically costs between 0.5% and 1% of the home’s sale price [97]. For instance, on a typical mortgage of $220,294, the lender’s policy would cost around $1,466 [97]. Buyers can save money by requesting simultaneous issue pricing, which offers discounts when purchasing both lender's and owner's policies at the same closing [1]. Given the competitive filed-rate system, it’s a good idea to get at least two quotes to compare fees.

| Property Value Range | Estimated Title Insurance Cost |

|---|---|

| $50,000 – $100,000 | $225 – $425 |

| $100,001 – $150,000 | $428 – $575 |

| $150,001 – $250,000 | $662 – $875 |

| $250,001 – $500,000 | $878 – $1,625 |

| $500,001 – $525,000 | $1,627 – $1,678 |

| $525,000 and above | $2.50 per $1,000 |

Additional closing costs can include title searches ($60–$200), settlement fees ($750–$975), and land surveys ($200–$800) [97]. Typically, buyers cover the cost of the lender’s policy, while sellers pay for the owner’s policy, though these terms are negotiable [97].

Kentucky’s policies also allow for certain endorsements, which can impact costs further.

Mandatory Endorsements

Kentucky does not require state-mandated endorsements for every transaction [98]. Instead, endorsements are typically determined by lender requirements or the specific property type. Examples include endorsements for condos or survey coverage [98]. Additionally, the state may begin adopting the ALTA 49 endorsement on a rolling basis through 2026, with an added cost of $50–$150 [1].

18. Louisiana

In Louisiana, lender title insurance must adhere to specific legal requirements. According to Louisiana Revised Statute § 22:513.1, every mortgage must include the name, bar number, and identifying details of an attorney licensed in Louisiana. Additionally, recorded documents must list the attorney's information alongside the title insurance producer's name, address, license number, and the underwriter's name. It's the producer's responsibility to ensure all these details are accurate before the documents are recorded [99].

Regulatory Requirements

Louisiana's title insurance regulations are deeply rooted in its legal framework. The state operates under a filed-rate system overseen by the Louisiana Department of Insurance (LDI) and the Louisiana Title Insurance Statistical Services Organization (LATISSO) [1][100]. Lender's title insurance is required for mortgage loans, providing protection to the lender against potential title defects. This policy remains in effect throughout the life of the loan, with the insurer's liability decreasing as the mortgage balance is paid down. Typically, the buyer is responsible for covering the cost of this insurance [101].

Pricing Structures

In Louisiana, the cost of title insurance generally ranges from 0.5% to 1% of the home's sale price [101]. For a mortgage averaging $234,325, the lender's policy would cost around $1,540. The pricing follows a tiered sliding scale, as outlined below:

| Housing Price Range | Title Insurance Cost |

|---|---|

| Up to $12,000 | $100.00 (Base) |

| $12,001 – $50,000 | + $5.40 per thousand |

| $50,001 – $100,000 | + $4.80 per thousand |

| $100,001 – $500,000 | + $4.50 per thousand |

| $500,001 – $1,000,000 | + $3.60 per thousand |

To reduce costs, buyers can take advantage of simultaneous issue pricing by purchasing both lender's and owner's policies during the same closing. Additionally, properties sold or refinanced within the past 2 to 10 years may qualify for a reissue rate discount of up to 40%. Louisiana uses Form LA107 (Simultaneous Premium Disclosure Form) to provide transparency about premium details to consumers [1][63][100].

Louisiana also includes specific mandatory endorsements to enhance policy coverage.

Mandatory Endorsements

For residential lender's policies, the ALTA 8.1 (Environmental Protection Lien) endorsement is standard in Louisiana [100]. Other frequently used endorsements include LATISSO 109 (Limited Construction Advance), LA 103 (Foundation), and the ALTA 49 endorsement (Post-Closing Forgery), which was introduced in August 2025 to address fraud risks occurring after the policy date [1][100]. Additionally, Louisiana mandates an "Endorsement Supplement" for policies exceeding standard limits or covering high-risk scenarios [100].

19. Maine

Maine is a filed rate state, meaning title insurers set and submit their own rates, fostering competition in the market. In most mortgage transactions, lender's title insurance is a requirement to safeguard the lender's financial stake [1][103]. The state strikes a balance between regulatory oversight and competitive pricing.

Regulatory Requirements

Maine's regulatory framework emphasizes strong consumer protections while maintaining competitive pricing. The Maine Bureau of Insurance oversees title insurance regulations and rate approvals. To protect lenders from potential losses caused by settlement agent misconduct, title insurers in Maine issue a single Closing Protection Letter (CPL) per transaction [102]. Additionally, state law prohibits splitting CPL fees, ensuring only one fee is charged for each transaction [102].

Maine has largely transitioned to using the 2021 ALTA forms, with limited reliance on the older 2006 versions [104][31]. The state is one of four - alongside Idaho, New Hampshire, and North Carolina - that mandates a Standard Arbitration Endorsement. This endorsement modifies standard policy language to align with state-specific dispute resolution requirements [104].

Pricing Structures

The cost of title insurance in Maine typically ranges from 0.5% to 1% of the home's sale price [103]. For properties valued up to $750,000, the standard rate is approximately $3.00 per $1,000 of property value. For instance, on a $452,697 mortgage, a lender's policy would cost around $2,691 [103]. Since Maine allows competitive filed rates, it’s a good idea for consumers to shop around and get at least two quotes. Differences of $300 to $500 between providers are common [1].

| Service Component | Estimated Cost |

|---|---|

| Lender's Policy (on $452,697 loan) | ~$2,691 |

| Title Search | $60–$200 |

| Title Settlement | $1,500–$3,000+ |

| Deed Preparation | $100–$250 |

| Escrow | $300–$700+ |

Bundling lender's and owner's policies can lead to additional savings. If the seller already holds an owner's policy, asking for a reissue rate could further reduce costs [8][103].

Mandatory Endorsements

Maine also specifies certain endorsements to meet lender requirements. While not explicitly mandated by state law, institutional lenders often require specific ALTA endorsements to comply with secondary market standards. The ALTA 8.1 (Environmental Protection Lien) endorsement is a standard inclusion for residential lender policies in Maine [104][105]. Similarly, the ALTA 9 (Restrictions, Encroachments, Minerals) endorsement is frequently requested by lenders [105][31]. For construction loans, lenders should consider state-specific Construction Loan Update endorsements to maintain lien priority as funds are disbursed [31]. Most endorsements in Maine can be added for a small fee on top of the base premium [31].

20. Maryland

Maryland operates as a filed rate state, meaning all premium rates for lender's and owner's title insurance must be submitted to and approved by the Maryland Insurance Administration (MIA). Title agents are not allowed to alter these rates, making service quality and additional fees the primary areas of competition [106].

Regulatory Requirements

Maryland has strict rules governing title insurance practices. Only licensed producers are permitted to handle trust funds, such as escrow and settlement monies [107]. Title insurers are required to conduct annual evaluations of their principal agents' underwriting, claims, and escrow practices. Additionally, they must secure a blanket fidelity bond and either a surety bond or letter of credit - usually set at $150,000 unless otherwise approved - to protect trust funds [107]. Anti-rebate laws are also enforced, preventing title companies from offering rebates, which helps maintain fair market conditions [110]. These regulations ensure Maryland's pricing model remains consistent and transparent.

Pricing Structures

Maryland employs a tiered pricing system for title insurance. For the first $250,000 of coverage, the rate is $2.95 per $1,000. For a $350,000 mortgage, the cost of a lender's policy, when issued simultaneously, is approximately $200. The minimum premium is $150 for properties valued at $40,000 or less [106] [110].

| Coverage Amount | Lender's Policy Rate (per $1,000) | Owner's Policy Rate (per $1,000) |

|---|---|---|

| Up to $250,000 | $2.95 | $4.35 |

| $250,001–$500,000 | $2.65 | $3.75 |

| $500,001–$1,000,000 | $2.40 | $3.20 |

| $1,000,001–$5,000,000 | $1.60 | $2.50 |

| $5,000,001–$15,000,000 | $1.20 | $1.65 |

| Over $15,000,000 | $1.15 | $1.55 |

Refinance transactions may qualify for reduced rates, with some underwriters offering rates as low as $1.50 per $1,000 for the first $250,000 of coverage [108]. Since Maryland's filed rates prohibit price negotiation, buyers are encouraged to evaluate the total package of title-related fees. These include title searches, which typically range from $150 to $500, and settlement fees, which usually fall between $200 and $600 [1]. This structured pricing, shaped by Maryland's robust regulatory framework, helps buyers understand their overall costs.

Mandatory Endorsements

Maryland law does not require specific endorsements. However, lenders typically insist on a Lender's Title Insurance Policy to ensure lien priority. The ALTA 49 endorsement, introduced in August 2025 to address post-closing forgery issues, is available as an optional add-on [1] [109].

21. Massachusetts

Massachusetts stands out as one of the few states that does not regulate title insurance rates in any way [112]. While the Massachusetts Division of Insurance is responsible for licensing title insurance companies, it does not review or approve policy forms or premiums [111][113]. In 2020, homebuyers in the state spent nearly $403 million on title insurance, shedding light on the market's lack of transparency [112].

Regulatory Requirements

Massachusetts operates differently from states that require filed rates. Here, title companies can set their own rates without needing state approval [1]. Real estate attorneys often act as title agents and may receive commissions as high as 80% of the premium, typically without clear disclosure to homebuyers [112]. Although lender's title insurance isn't legally required by the state, nearly all financial institutions make it a mandatory condition for securing a mortgage [111][113]. Additionally, the state does not collect much data on insurer practices or fees, which further limits transparency [112].

Title insurance companies are not required to file their policies or rates with the Massachusetts Division of Insurance. Therefore their policies are neither reviewed nor approved by the Division. - Massachusetts Division of Insurance [113]

Pricing Structures

Title insurance premiums in Massachusetts generally range from 0.5% to 1% of a home's sale price [115]. The standard rate is $2.50 per $1,000 of coverage, with a minimum premium of $100 for properties valued up to $40,000 [114]. Enhanced loan policies are slightly pricier at $2.75 per $1,000, with a $110 minimum [114]. When a lender's policy is issued simultaneously, the fee drops to a flat $175 [114][116]. Homeowners refinancing their mortgage may qualify for a 40% discount on the loan policy premium if a prior mortgage exists [114]. Additional costs include a standard $35 fee for a Closing Protection Letter and title search fees that typically range from $80 to $200 [114][115].

Mandatory Endorsements

Since the Massachusetts Division of Insurance does not approve policy forms, the state does not mandate specific endorsements [111][113]. However, lenders often require coverage for risks such as mechanic's liens, encroachments, forged documents, and undisclosed heirs [117][113]. The ALTA 49 endorsement, introduced in August 2025 to address post-closing forgery and deed fraud, is an optional add-on priced between $50 and $150 [1]. Enhanced policies in Massachusetts offer broader protection, covering up to 33 risks compared to the 12 covered by standard policies [1][114]. This market-driven approach highlights Massachusetts' distinctive position in the broader landscape of lender title insurance regulations across the U.S.

22. Michigan

Michigan operates as a "filed rate" state, meaning title insurance companies submit their rates to the Michigan Insurance Bureau for approval [1][118]. This system encourages competition, leading to price differences between providers - unlike states like Texas and Florida, where rates are standardized [1]. While Michigan law doesn’t require title insurance, lenders almost always insist on a lender’s policy to safeguard against liens and title defects [119][120].

Regulatory Requirements

The Michigan Insurance Bureau manages all title insurance rate filings and approvals [118]. By tradition, sellers usually pay for the owner's policy, while buyers handle the lender's policy [118][119]. The premium includes title search and examination fees [118]. Pre-closing work - such as searches, examinations, and resolving title issues - makes up most of the premium costs, with the rest allocated to the insurance reserve for claims. Interestingly, title insurance resolves issues in about 25% of real estate transactions before closing [1]. These practices contribute to Michigan’s competitive pricing system.

Pricing Structures

Michigan’s filed rate system uses a tiered pricing model based on the loan amount. For example, a lender’s policy for a $250,000 property costs around $787, while a $400,000 loan (on a $500,000 property with 20% down) runs approximately $1,202 [119]. Rates decrease as the loan amount increases:

- Up to $50,000: $3.15 per $1,000

- $50,001–$100,000: $2.50 per $1,000

- $100,001–$200,000: $2.20 per $1,000

- $200,001–$300,000: $1.90 per $1,000

- $300,001–$1,000,000: $1.60 per $1,000

- Above $1,000,000: $1.25 per $1,000 [119]

A simultaneous issue discount applies when combined with an owner's policy. Additional costs include title search fees ($75–$200), closing fees ($400–$600), and recording fees (about $125) [121].

Mandatory Endorsements

Michigan lenders typically require standard ALTA endorsements to ensure the mortgage qualifies as a first lien for secondary market compliance [121]. Borrowers can choose between a standard ALTA policy, covering 12 specific pre-closing risks, or an "Eagle" (Expanded) policy, which provides protection against 33 risks - such as zoning violations and post-closing forgery - for a 10–20% premium increase [1][119][120].

Additionally, the ALTA 49 endorsement, introduced in August 2025 to address post-closing forgery and deed fraud, is now available in Michigan as an optional add-on, priced between $50 and $150 [1]. Michigan also permits "split closings", where buyers and sellers can use different title companies for their respective policies if they can't agree on a single provider [120].

23. Minnesota

Minnesota follows a filed rate system, where title insurance companies submit their rates to the Minnesota Department of Commerce. This approach creates room for price differences between providers. Importantly, Minnesota law ensures that consumers can choose their title insurer, rather than being restricted to a lender's recommendation [123]. This choice encourages competition in the market, giving buyers more control over their options.

Regulatory Requirements

The Minnesota Department of Commerce oversees the title insurance industry in the state [124]. Title insurers are required to maintain a guaranty fund of at least $100,000 or two-fifths of their capital stock, whichever is larger [122]. Additionally, Minnesota complies with federal RESPA Section 8 rules, which prohibit kickbacks or referral fees in real estate transactions [123]. For lenders, their title insurance policy remains valid until the mortgage is fully paid off, refinanced, or the property is sold [123].

Pricing Structures

Minnesota's pricing model offers potential savings depending on the property's value. For instance, on a $300,000 property with 20% down, buying both an owner's and lender's policy together can drop the lender's fee to a flat $75. On the other hand, a standalone policy for an average mortgage of $294,972 costs around $2,132 [124][125]. Title insurance rates vary based on coverage amounts, ranging from $4.00 per $1,000 for properties under $50,000 to $1.75 per $1,000 for properties exceeding $1,000,000 [124][125]. Additional fees include title searches ($60–$200), settlement charges (roughly 0.33% of the sale price), and land surveys ($200–$800) [124][125].

Mandatory Endorsements

Minnesota lenders often require endorsements to address specific risks. Standard ALTA policies are common, with optional endorsements available for issues like building permit violations, unrecorded estate tax liens, and post-policy forgery [125]. A notable development is the ALTA 49 endorsement, introduced in August 2025, which is being implemented across Minnesota. This endorsement adds protection against post-closing forgery and seller impersonation fraud - risks not typically covered by standard policies [1].

24. Mississippi

Mississippi uses an unregulated rate structure for title insurance, meaning companies set their own premiums instead of adhering to state-mandated pricing guidelines [127][128]. Each insurer submits its rate manual to the Mississippi Insurance Department, but price differences between companies are typically small [130][127]. This competitive model stands in contrast to states like Texas and Florida, where uniform rates are applied across all providers [1]. Below, we explore Mississippi's regulatory framework, pricing models, and endorsement practices.

Regulatory Requirements

The Mississippi Insurance Department oversees licensing for title insurance providers and requires annual financial filings [126]. A defining aspect of Mississippi's regulations is the attorney involvement requirement - only attorneys can draft legal documents like Warranty Deeds and Deeds of Trust unless prepared by a transaction party [128]. Attorneys licensed in the state are exempt from the $100 biennial licensing fee that non-attorney agents must pay [126].

Title companies must maintain a reserve for losses, calculated as the lesser of 10% of all premiums received or $50,000. Additionally, policies exceeding 50% of a company’s capital and surplus require reinsurance [126]. The standard title search period in Mississippi spans 32 years [128]. These rules shape the operational and cost structure of title insurance in the state.

Pricing Structures

For a typical mortgage in Mississippi valued at $233,430, a standalone lender's policy costs about $1,535 [129]. However, if issued simultaneously with an owner's policy, the lender's policy is reduced to a flat $100 [127]. Rates vary based on property value, starting at $4.50 per $1,000 for properties under $100,000 and decreasing to $1.75 per $1,000 for properties over $15,000,000 [129]. Refinancing discounts depend on the insurer and timing [127]. This pricing model highlights that title insurance primarily covers professional services rather than just risk protection.

Mandatory Endorsements

Mississippi does not require state-specific endorsements for lender's title insurance policies, nor does it modify standard ALTA policy provisions [128]. While title insurance is not legally mandated in the state, most lenders require a Loan Policy as a condition for securing a mortgage [127]. Usury coverage is available under Mississippi Code Ann. § 75-17-1 [128].

Additionally, the state participates in a Mutual Indemnification Agreement among major underwriters to streamline the resolution of minor title defects. Automatic indemnity under this agreement is capped at the policy face amount or $250,000, whichever is lower [131].

25. Missouri

Missouri operates under a competitive filed-rate system, allowing insurers to set their own premiums [1]. This creates a range of price options, giving buyers the opportunity to shop around for better deals [134]. For a typical Missouri mortgage of $346,762, the cost of a lender's policy averages about $2,132 [134]. Bundling an owner's policy with a lender's policy often results in noticeable savings [134]. These pricing dynamics are supported by Missouri's strict regulatory framework.

Regulatory Requirements

Missouri enforces detailed recordkeeping and agent reviews, similar to other states with competitive systems. State law mandates that title insurance policies must be based on a title plant search covering at least 27 years of continuous records in the county where the property is located [133]. If a title plant is unavailable or access is restricted, insurers are required to use the best available title evidence [133]. Additionally, records from the title examination must be kept for 15 years after the policy is issued [133].

The state also requires annual on-site reviews of agents' practices, including underwriting, claims, and escrow operations. Documentation from these reviews must be retained for at least four years [132][136]. Since August 28, 2016, Missouri has mandated a $25 Closing Protection Letter (CPL) for all residential transactions [136]. These CPLs safeguard settlement funds from theft or fraud and cannot be waived by any party [136].

Pricing Structures

Missouri's competitive market keeps title insurance costs between 0.5% and 1% of a home's sale price [134]. According to Urban Institute data, combined title fees in Missouri average $358, making them some of the lowest in the country. For comparison, states like Pennsylvania see average fees as high as $3,496 [135]. Premium rates in Missouri decrease as property values rise, starting at $4.60 per $1,000 for properties under $100,000 and dropping to $1.65 per $1,000 for properties valued over $10,000,000 [134].

Around 95% of title insurance premiums in the state go toward professional services like title searches and examinations, rather than claim reserves [135]. Buyers should ask about reissue rates if the property was purchased recently, as prior title research might qualify for discounts [135]. Missouri also requires specific endorsements to ensure additional protections in residential transactions.

Mandatory Endorsements

Missouri's endorsement requirements align with top practices nationwide. A CPL must be issued for all residential transactions involving a title agent or underwriter managing funds or documents [136]. Residential properties are defined as homes designed for one to four families, excluding commercial or agricultural properties [136]. If a lender's policy is issued without a simultaneous owner's policy, agents must notify the buyer in writing that the lender's policy does not provide personal protection. This signed notice must then be retained in the underwriting file for 15 years [137].

26. Montana

Montana uses a filed-rate system for title insurance, where companies submit their rates to state regulators. This setup creates competition, leading to noticeable price differences among providers. For the average Montana mortgage of $370,576, a lender's policy costs around $2,258. While lender's title insurance is mandatory for most mortgages, an owner's policy is optional [1][140].

Regulatory Requirements

Title insurance in Montana is governed by the Montana Title Insurance Act (Title 33, Chapter 25 of the Montana Code Annotated) under the supervision of the Commissioner of Insurance [138]. Insurers and producers are required to maintain separate fiduciary trust accounts for funds handled during escrow or settlement services [139]. Regulations (ARM 6.6.2201) mandate that insurers disclose all outstanding recorded liens but allow coverage for specific items if underwriting standards are met - such as when funds are held in escrow or when a lien is barred by the statute of limitations [141]. Additionally, interest earned from pooled trust accounts is directed to the Montana Land Title Foundation, which supports nonprofit initiatives and continuing education for title agents [139].

Pricing Structures

In Montana, title insurance costs generally fall between 0.5% and 1.0% of the home's sale price [140]. Like other filed-rate states, about 80% of the premium goes toward pre-closing services like title searches, while only 20% is allocated to the insurance reserve for potential claims [1]. Premium rates decrease as loan amounts rise. For instance, the base fee for properties up to $15,000 is $180.50, while rates drop to $1.75 per $1,000 for properties over $1,000,000 [140]. Because pricing can vary significantly - sometimes by $300–$500 between providers - it's wise to request quotes from at least two companies [1]. Typically, buyers cover the lender's policy, while sellers pay for the owner's policy [140].

Coverage Limits

A lender's policy in Montana guarantees the validity, enforceability, and priority of the lien [141]. Unlike an owner's policy, which remains active as long as the owner or their heirs retain the property, a lender's policy is valid only for the loan's duration, with liability decreasing as the loan is repaid [140]. Buyers should inquire about the ALTA 49 endorsement, introduced in August 2025, which offers protection against post-closing forgery - something not covered by standard policies [1]. Bundling an owner's and lender's policy from the same provider often qualifies for a simultaneous issue discount [140].

27. Nebraska

Nebraska operates as a filed-rate state, meaning title insurance companies must submit their rates to regulators for review and approval [144]. For a typical Nebraska mortgage of $310,164, the cost of a lender's policy averages around $1,940 [143]. While lender's title insurance is required for mortgage-backed transactions, buyers have the flexibility to shop for better rates since premiums aren't strictly fixed [143].

Regulatory Requirements

Title insurance policies in Nebraska must be issued by companies authorized to operate within the state [142]. Any zero-premium endorsement - additional coverage provided at no extra charge - must automatically be included in all relevant policies [145]. Insurers are required to file all policy and endorsement forms with the Director of Insurance, and these forms are automatically approved after 30 days unless explicitly rejected [145].

If a lender's policy is issued without an accompanying owner's policy, the agent must inform the buyer in writing that the coverage only protects the lender and not the property owner. This notice must be signed by the buyer and kept in the underwriting file for at least five years [146].

Pricing Structures

Title insurance in Nebraska typically costs between 0.5% and 1.0% of the property's sale price [143]. Unlike in some states, Nebraska includes title search and examination fees within the insurance premium instead of listing them as separate charges [144]. By local custom, both the buyer and seller share the cost of owner's and lender's policies equally [144]. Opting to bundle both policies with the same company can often lead to a simultaneous issue discount [143].

About 80% of the premium is allocated to pre-closing services like title searches and legal curative work, while the remaining 20% is reserved for potential claims [1]. This breakdown highlights how the costs are distributed and the services covered.

Coverage Limits

In Nebraska, a lender's policy ensures the lender's interest is protected for the duration of the loan, with liability decreasing as the loan is repaid. Meanwhile, an owner's policy safeguards the property for as long as the owner or their heirs hold it. The lender's policy guarantees the validity and priority of the lender's lien on the property.

Nebraska also permits the use of Attorney Opinion Letters (AOLs) as a more affordable alternative. However, these come with increased risk for lenders compared to traditional title insurance [143].

28. Nevada

Nevada operates as a filed-rate state, meaning title insurers must submit their rates to the Division of Insurance for approval [148]. This system results in varying costs between providers. For example, in Clark County, the price for combined owner's and lender's policies on a $150,000 property ranges from $1,046 to $1,407 [149]. The Nevada Division of Insurance highlights this variation, stating, "The cost of title insurance can vary significantly between companies. You do not have to use the company recommended to you" [149].

Regulatory Requirements

Title insurance in Nevada is governed by Nevada Administrative Code (NAC) Chapter 692A and Nevada Revised Statutes (NRS) 692A [147][149]. Licensing is mandatory for title agents and escrow officers, requiring at least one year of recent experience and an appointment by an authorized title insurer [147][150]. While state law does not require title insurance, lenders almost always insist on a lender's policy to protect their financial interest until the loan is fully repaid [149][151].