ASC 810 Rules for Real Estate SPEs

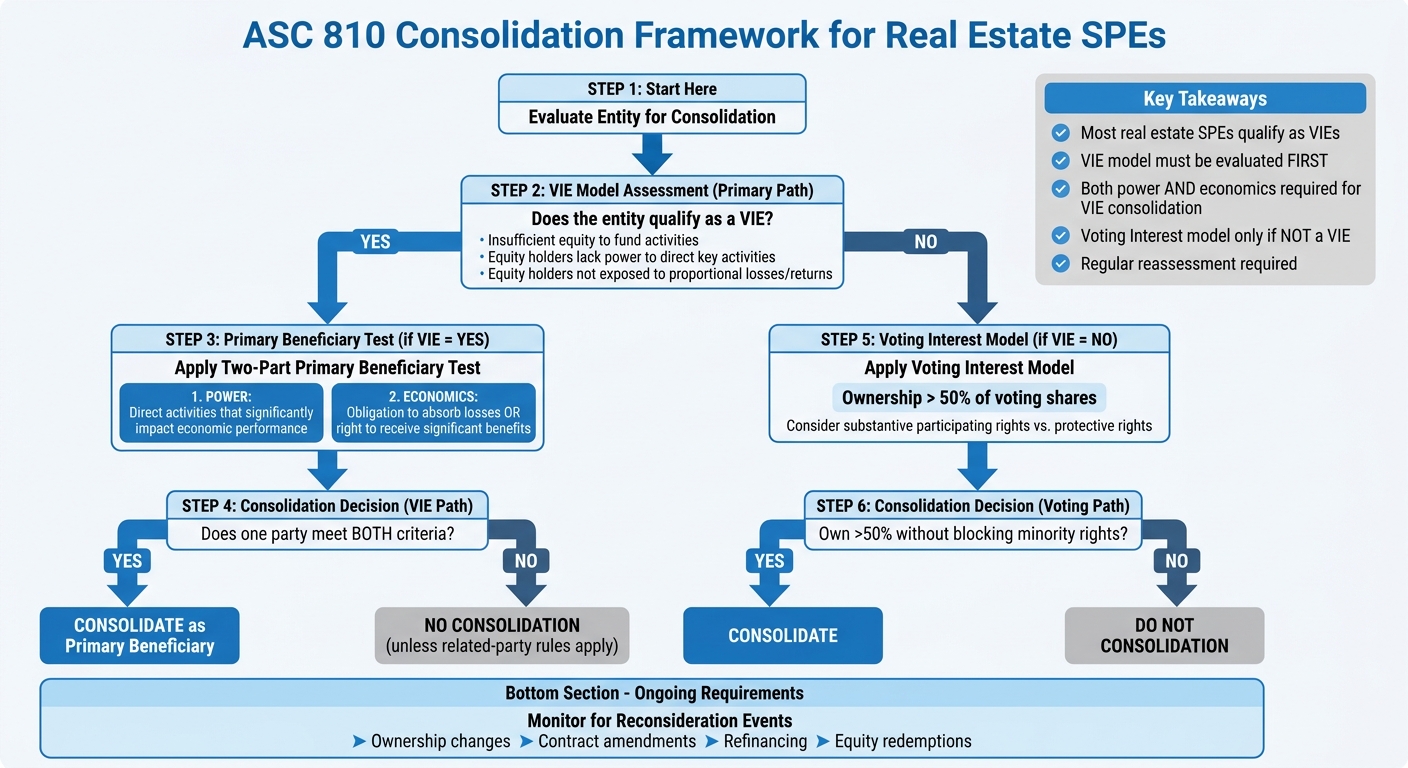

Consolidating Special Purpose Entities (SPEs) in real estate is complex but essential for accurate financial reporting. ASC 810 provides the framework to decide whether to consolidate an entity, using two models: the Variable Interest Entity (VIE) model and the Voting Interest model. The process starts with the VIE model, focusing on control and economic exposure, and moves to the Voting Interest model only if the entity doesn’t qualify as a VIE.

Key takeaways for real estate professionals managing SPEs:

- VIE Model: Most real estate SPEs qualify as VIEs due to limited partner structures or insufficient equity.

- Primary Beneficiary: To consolidate, a party must control key activities and have significant financial exposure.

- Voting Interest Model: Applies when VIE criteria aren’t met, requiring over 50% ownership unless minority rights block control.

- Documentation: Maintain detailed records of agreements, ownership, and decisions to ensure compliance and avoid errors.

Proper consolidation impacts critical metrics like leverage ratios and asset valuations, making it vital to follow ASC 810’s structured approach. Missteps can lead to restatements or regulatory issues. Regular reassessment and expert guidance can help navigate these rules effectively.

ASC 810 Consolidation Decision Framework for Real Estate SPEs

Introduction to Consolidation Accounting: ASC 810, VIEs & Elimination Entries

sbb-itb-df8a938

Core Principles of ASC 810 Consolidation

Let’s take a closer look at the core principles of ASC 810 as they apply to real estate Special Purpose Entities (SPEs). When evaluating consolidation under ASC 810, you must follow a specific sequence: start with the Variable Interest Entity (VIE) model. Only if the entity does not qualify as a VIE should you move on to the Voting Interest model [2][5]. This sequence is critical and applies regardless of the entity's structure.

Control and Consolidation Criteria

Under the Voting Interest model, consolidation is required if you hold more than 50% of the outstanding voting shares [2]. In the case of limited partnerships, this typically means owning over 50% of the "kick-out rights", which allow limited partners to remove the general partner [2]. However, control can be affected if minority investors have substantive participating rights - rights that enable them to block significant financial and operational decisions made during regular business activities [2][4]. On the other hand, protective rights, which are limited to extraordinary decisions like liquidation or charter amendments, do not prevent consolidation [2].

Variable Interest Entities (VIEs)

An entity is classified as a VIE if it meets one or more of the following conditions:

- It has insufficient equity to fund its activities without additional financial support.

- Its equity holders lack the power to direct activities that significantly impact the entity's performance.

- Its equity holders are not exposed to losses and returns proportional to their investment [2][1].

In the real estate sector, most commercial real estate partnerships meet the VIE criteria because limited partners often provide capital but lack operational control [1]. A variable interest refers to any involvement whose value changes with the entity’s net assets. This can include equity stakes, guarantees, subordinated debt, or service fees that are not negotiated at arm’s length [2].

Determining the Primary Beneficiary

Once an entity is identified as a VIE, the next step is determining who consolidates it. The Primary Beneficiary is the party responsible for consolidating the VIE. According to FASB ASC 810-10-25-38A, this is determined through a two-part test, and both criteria must be met:

A reporting entity shall be deemed to have a controlling financial interest in a VIE if it has both of the following characteristics: [2] The power to direct the activities of a VIE that most significantly impact the VIE's economic performance [5] The obligation to absorb losses of the VIE that could potentially be significant to the VIE or the right to receive benefits from the VIE that could potentially be significant to the VIE [6].

Power refers to the ability to direct activities that significantly influence the VIE’s economic outcomes, such as property management or refinancing decisions in real estate [2][5]. Economics involves the obligation to absorb losses or the right to receive benefits that are significant to the VIE [5]. If these roles are split between different parties, no single entity consolidates the VIE [4]. However, if no party within a related-party group meets both criteria, the party "most closely associated" with the VIE is required to consolidate it [2][6].

Step-by-Step Guide to Applying ASC 810 to Real Estate SPEs

Now that the core principles of consolidation are clear, let’s dive into how ASC 810 applies specifically to real estate Special Purpose Entities (SPEs). This process involves a structured sequence to ensure accurate consolidation decisions.

Identifying Variable Interests in SPEs

The first step is to identify all variable interests within the SPE. A variable interest refers to any contractual, ownership, or financial stake that fluctuates with the fair value of the entity’s net assets [5]. In real estate SPEs, these interests extend beyond simple equity ownership.

Here are some examples of variable interests commonly found in real estate structures:

- Equity interests: Includes common stock or partnership stakes.

- Guarantees: Covering the SPE’s debt or performance obligations.

- Fee arrangements: Where fees for management or services depend on the entity’s performance.

- Subordinated debt: Absorbs expected losses.

- Contractual rights: Tied to the SPE’s net asset changes.

For instance, providing property management services at rates below market value could qualify as a variable interest, even if no equity is held.

"Variable interests are defined as 'contractual, ownership, or other pecuniary interests in a VIE that change with changes in the fair value of the VIE's net assets exclusive of variable interests.'" - BDO [5]

It’s crucial to maintain a detailed inventory of these interests to ensure all potential Variable Interest Entities (VIEs) are identified. Once this step is complete, move on to determining whether the SPE qualifies as a VIE.

Assessing VIE Status

After identifying variable interests, the next step is to evaluate whether the real estate SPE meets the criteria for a VIE. This assessment must be done before applying the Voting Interest model. A real estate SPE qualifies as a VIE if:

- It lacks sufficient equity at risk to independently finance its activities.

- Its equity holders do not have the authority to direct activities that significantly affect the entity’s economic performance.

- Its equity holders are not obligated to absorb losses or entitled to receive residual returns proportionate to their investment.

For example, in a real estate limited partnership, if limited partners provide funding but a general partner controls daily operations, the entity is likely a VIE.

Carefully review operating agreements. Check for substantive "kick-out rights" (the ability of limited partners to remove the general partner without cause) and document any participating rights, such as veto power over major decisions like asset sales, refinancing, or development budgets. Once VIE status is confirmed, the next step is to identify the primary beneficiary for consolidation.

Consolidation Requirements for Real Estate SPEs

If the SPE is classified as a VIE, the focus shifts to determining the primary beneficiary - the party responsible for consolidating the SPE. This determination hinges on a two-part test:

- The party must have the power to direct the activities that significantly impact the VIE’s economic performance.

- The party must have the obligation to absorb losses or the right to receive benefits that are significant to the VIE’s economic performance.

In real estate SPEs, "power" typically involves decision-making authority over property management, leasing, sales, and refinancing. For instance, a general partner with sole control over these activities likely satisfies the power requirement. However, both power and significant economic exposure must be present - meeting just one criterion isn’t enough. When evaluating economic exposure, consider both direct and indirect interests, including those held through related parties.

If both criteria are met, the primary beneficiary must consolidate the VIE. This involves including the VIE’s assets, liabilities, and operating results in the consolidated financial statements, while eliminating intercompany transactions. Additionally, specific disclosures are required, such as:

- The methodology used to identify the primary beneficiary.

- Maximum exposure to potential losses.

- Restrictions on the VIE’s assets.

- Details about the entity’s involvement with the VIE.

Consolidation isn’t a static process. Establish a system to monitor for reconsideration events such as changes in contracts, refinancing, equity redemptions, or shifts in ownership. This ensures that VIE status and primary beneficiary determinations remain up-to-date as circumstances evolve.

Exceptions and Special Considerations

When finalizing your ASC 810 analysis, it's crucial to address exceptions and potential challenges. Not every real estate SPE (Special Purpose Entity) requires consolidation under ASC 810. Certain scope exceptions and alternative models can simplify financial reporting.

Scope Exceptions Under ASC 810

ASC 810-10 outlines specific exclusions from consolidation requirements. For instance, investment companies governed by ASC 946 are exempt since they report investments at fair value rather than consolidating them [2]. This is particularly relevant for real estate funds structured as registered investment companies. Likewise, employee benefit plans under ASC 712 or ASC 715 are not subject to consolidation, and governmental organizations are generally excluded unless they resemble VIEs (Variable Interest Entities). Additionally, money market funds and similar entities operating under Rule 2a-7 of the Investment Company Act are exempt [2].

Private companies benefit from an important option introduced by ASU 2018-17. This allows them to bypass the VIE model for entities under common control, as long as neither the reporting entity nor the legal entity is a public business entity, and the reporting entity doesn’t have a controlling financial interest under the Voting Interest model alone [2]. This election can simplify consolidation for family-owned real estate portfolios and private holding structures. However, proper documentation of the entity’s structure and the rights of minority investors is critical to justify your consolidation decisions.

When to Use the Voting Interest Model

The Voting Interest model applies when an entity does not meet the criteria for a VIE. If you own more than 50% of the voting shares and the entity has sufficient equity at risk with voting rights aligned to economic exposure, traditional ownership rules determine consolidation.

However, even with majority ownership, consolidation isn’t guaranteed. If minority shareholders hold substantive participating rights - such as veto power over asset sales, refinancing, or budget decisions - these rights can block consolidation despite a majority stake. Understanding these details is essential to avoid misclassifications.

Common Challenges and How to Avoid Them

One common mistake is misclassifying an entity as a VIE or incorrectly applying the Voting Interest model. As the LegalClarity Team warns:

Getting this analysis wrong can overstate or understate a company's reported assets, liabilities, and earnings, which invites restatements and regulatory trouble [2].

The "insufficient equity at risk" condition often causes confusion, especially when complex financing arrangements obscure the entity's true nature. A 2026 financial analysis highlighted that misclassification of ASC 810 structures frequently led to restatements, emphasizing the importance of applying clear criteria and maintaining regular training.

Another challenge lies in distinguishing protective rights from participating rights. Protective rights are designed to safeguard minority investors from harmful decisions but do not grant control. Participating rights, on the other hand, allow minority investors to block significant actions, potentially altering consolidation outcomes. To avoid errors, establish a structured process that includes a thorough inventory of entities and their relationships. Reassess consolidation decisions whenever governing documents change or economic relationships evolve. As the LegalClarity Team notes:

The analysis is more nuanced than most practitioners expect, particularly when control flows through contracts rather than share ownership [2].

Key Takeaways for Real Estate Professionals

Applying ASC 810 in Practice

Consolidating under ASC 810 isn’t something you can simply check off a list - it’s an ongoing process. Start with the Variable Interest Entity (VIE) model. If the entity doesn’t qualify as a VIE, then move to the Voting Interest model. For most commercial real estate partnerships, the VIE model tends to apply due to factors like thin capitalization or limited partner structures [1].

The primary beneficiary test is the heart of this process. It identifies the party with the authority to direct critical activities - such as property management or refinancing - and the one with significant economic exposure. As Madras Accountancy explains:

The difference between VIE and voting interest analysis determines which entities consolidate, directly affecting reported leverage, asset values, and financial performance metrics stakeholders rely on for investment decisions [1].

Mistakes here can lead to serious consequences like audit adjustments, restatements, or misrepresented financial positions.

Consolidation isn’t static - it can change. That’s why it’s essential to monitor for events like ownership changes, amendments, or refinancing, which can shift subordination structures and trigger the need for reassessment [1][3]. Keeping thorough documentation - such as operating agreements, waterfall structures, and consolidation memos - can help protect your accounting decisions during audits.

Given how intricate these evaluations can get, consulting with specialists is often the best way to ensure compliance and accuracy.

Getting Expert Support

ASC 810’s technical requirements can be overwhelming, even for seasoned finance teams. This is especially true when power and financial exposure are shared among multiple parties or when related-party relationships create implicit variable interests. For professionals managing complex, multi-entity real estate structures, having access to specialized expertise is a game-changer.

The Fractional Analyst offers tailored financial analysis and insights designed to support areas like underwriting, asset management, and investor reporting. Their services help ensure compliance with GAAP while keeping costs manageable during the often-challenging consolidation process.

FAQs

What makes a real estate SPE a VIE under ASC 810?

A real estate SPE is generally considered a Variable Interest Entity (VIE) under ASC 810 if it doesn't have enough equity investment to operate independently without additional financial backing. Moreover, the primary beneficiary is identified as the party that both has the authority to direct significant activities impacting the entity's financial performance and bears the obligation to absorb its losses or the right to benefit from its gains.

How do I determine who the primary beneficiary is in a real estate VIE?

To figure out who the primary beneficiary of a real estate VIE is, you’ll need to determine which entity holds two key elements: the power to direct activities that play a major role in the VIE's financial performance and the obligation to absorb losses or the right to receive benefits. This process involves a qualitative assessment, focusing on control-related factors to ensure the primary beneficiary satisfies both conditions for having substantial influence over the VIE.

What events trigger a required reconsideration of consolidation under ASC 810?

When consolidation under ASC 810 comes into question, it’s usually due to shifts in control or variable interests that meet the criteria for consolidation. These shifts can stem from major changes in contractual arrangements, legal structure, voting rights, or the entity’s purpose or design. Additionally, updates to the Variable Interest Entity (VIE) model - like those introduced in ASU 2015-02 - may prompt a reassessment. This is especially true if new developments or changes indicate that the entity’s classification as a VIE or voting interest entity might have shifted.