Ground Lease Depreciation Rules Explained

Ground lease depreciation rules can be complex but understanding them is essential for managing tax benefits effectively. Here's the key takeaway: land cannot be depreciated, but improvements made by tenants on leased land can be. These improvements, like buildings or structures, follow IRS guidelines for depreciation, typically over a 39-year straight-line schedule.

Key Points:

- Ground Lease Basics: The tenant leases land to develop it, while the landlord retains ownership of the land. Improvements made by tenants usually revert to the landlord at the end of the lease.

- Depreciation Rules:

- Tenants can depreciate the cost of improvements (e.g., buildings) over 39 years.

- Landlords cannot depreciate land but may depreciate owned improvements unless lease terms prevent it.

- IRS Section 178:

- Lease terms, including renewal options, affect depreciation periods.

- If the lease term is less than 60% of the improvement's useful life, renewal options must be included in calculations.

- Exceptions: Short lease terms and specific agreements may alter depreciation eligibility or calculation methods.

By understanding these rules, tenants and landlords can optimize their tax strategies while staying compliant. Let’s dive into the details.

IRS Guidelines for Ground Lease Depreciation

Who Can Claim Depreciation on Ground Lease Improvements

The IRS states that to claim depreciation, taxpayers must demonstrate ownership-like responsibilities. This includes holding legal title, paying for the property, handling maintenance and taxes, and facing the risk of loss if the property is damaged or declines in value [5].

Tenants (lessees) cannot depreciate the land or the leased property itself. However, they can depreciate capital improvements made to the leased land [5][2]. For instance, if you lease a plot of land and construct a warehouse on it, you can depreciate the cost of building the warehouse over 39 years, even though you don’t own the land.

Landlords (lessors) can depreciate improvements they own. However, if the lease requires the tenant to return the property in its original condition, the landlord cannot claim depreciation [5]. Essentially, the right to depreciation typically goes to the party who makes the capital investment and assumes the associated risks.

The specifics of lease terms under Section 178 further clarify how depreciation periods are determined.

Section 178: How Lease Terms Affect Depreciation

Under Section 178, lease durations play a significant role in determining depreciation periods. If the remaining lease term (excluding renewal options) is less than 60% of the improvement's useful life, all renewal options must be included in the calculation. Similarly, if a lease is acquired and less than 75% of the cost relates to the unexpired term, renewal options extend the amortization period [3][8][7][6].

For example, imagine you have a 20-year ground lease and build a structure with a 39-year useful life. Since 20 years is only 51% of 39 years (below the 60% threshold), you must account for any renewal options when calculating your depreciation period. However, if you can demonstrate that it’s "more probable than not" the lease won’t be renewed, you may exclude these options [3][8].

If the landlord and tenant are related parties as defined by the IRS, the lease term is extended to match the full useful life of the improvements. This eliminates the possibility of shorter depreciation periods [3][8].

39-Year Straight-Line Depreciation for Commercial Buildings

Commercial buildings follow a standard depreciation schedule under the Modified Accelerated Cost Recovery System (MACRS). These structures are classified as nonresidential real property with a 39-year recovery period [5]. The IRS requires the use of the straight-line method, which spreads the cost evenly over the 39 years.

The mid-month convention applies to commercial buildings, meaning depreciation begins as if the property was placed in service in the middle of the month, regardless of the actual date [5]. This impacts the depreciation claimed in the first and last years. For example, if a building is completed in March 2026, you would claim 9.5 months of depreciation for that year.

Even if the ground lease term is shorter than 39 years, improvements are typically depreciated over the full 39-year MACRS period. Section 178 rules determine whether renewal options require extending this period. Remember, only the improvements - not the land - are depreciable [5][2].

sbb-itb-df8a938

Real Estate Depreciation Explained

Exceptions and Special Cases

The IRS guidelines for ground lease depreciation include several exceptions and special cases that can significantly affect how depreciation is applied. Understanding these nuances is crucial for ensuring compliance and optimizing tax benefits.

Short Lease Terms and IRS Probability Tests

For ground leases with short terms, the IRS uses a probability test to assess depreciation eligibility. This test allows renewal options to be excluded from depreciation calculations if you can demonstrate a higher likelihood that the lease will not be renewed [3].

This becomes particularly important when the remaining lease term is less than 60% of the original term. If you can provide evidence - such as market data, business plans, or other relevant factors - that renewal is unlikely, depreciation can be calculated based on just the base term [3].

"The establishment by a lessee as of the close of the taxable year that it is more probable that the lease will not be renewed, extended, or continued will ordinarily be effective as of the close of such taxable year and any subsequent taxable year." - 26 CFR § 1.178-1 [3]

To support a non-renewal determination, it’s essential to maintain detailed records at the end of each tax year. This could include documentation like correspondence about relocation plans, financial forecasts that show the lease no longer aligns with your business needs, or evidence of declining property values in the area [3].

Leasehold Improvements vs. Land Ownership

While land itself cannot be depreciated, improvements made by tenants on leased land can be. Leasehold improvements, particularly those classified as Qualified Improvement Property (QIP), are eligible for a 15-year recovery period [9][10]. However, only interior modifications qualify as QIP - exterior changes like roofing, elevators, or structural expansions do not [9][10].

For GAAP financial reporting, the rules differ slightly. Improvements must be amortized over the shorter of their useful economic life or the remaining lease term [9][11]. If the lease is terminated early, the remaining un-depreciated balance can be deducted in the year of termination [12].

The Tax Cuts and Jobs Act increased the maximum expensing limit for certain improvements to $1.0 million, while the CARES Act of 2020 made QIP eligible for first-year bonus depreciation [10]. These changes allow for faster tax benefits compared to the traditional 39-year depreciation schedule.

Non-Standard Lease Agreements and Depreciation

Non-standard lease agreements can introduce unique challenges when it comes to depreciation. For example, reversion clauses - where the lessee is required to return the property and improvements in their original condition and value - can prevent the landlord from claiming depreciation on the property [13].

"If the lease provides that the lessee is to maintain the property and return to you the same property or its equivalent in value at the expiration of the lease in as good condition and value as when leased, you cannot depreciate the cost of the property." - IRS Publication 946 [13]

Variable lease terms, such as performance-based extensions or conditional renewal options, require a detailed review under Section 178. These situations are evaluated on a case-by-case basis, depending on the specifics of the lease agreement. Attorney Kelly Nicole Depew of Holland & Knight explains that while tenants can depreciate the cost of their improvements for tax purposes, the exact terms of non-standard agreements play a critical role in determining how depreciation is applied [1].

Extended ground leases can also lead to additional complications, such as triggering transfer taxes or being treated as property sales, which can alter depreciation calculations [1].

How to Calculate Ground Lease Depreciation

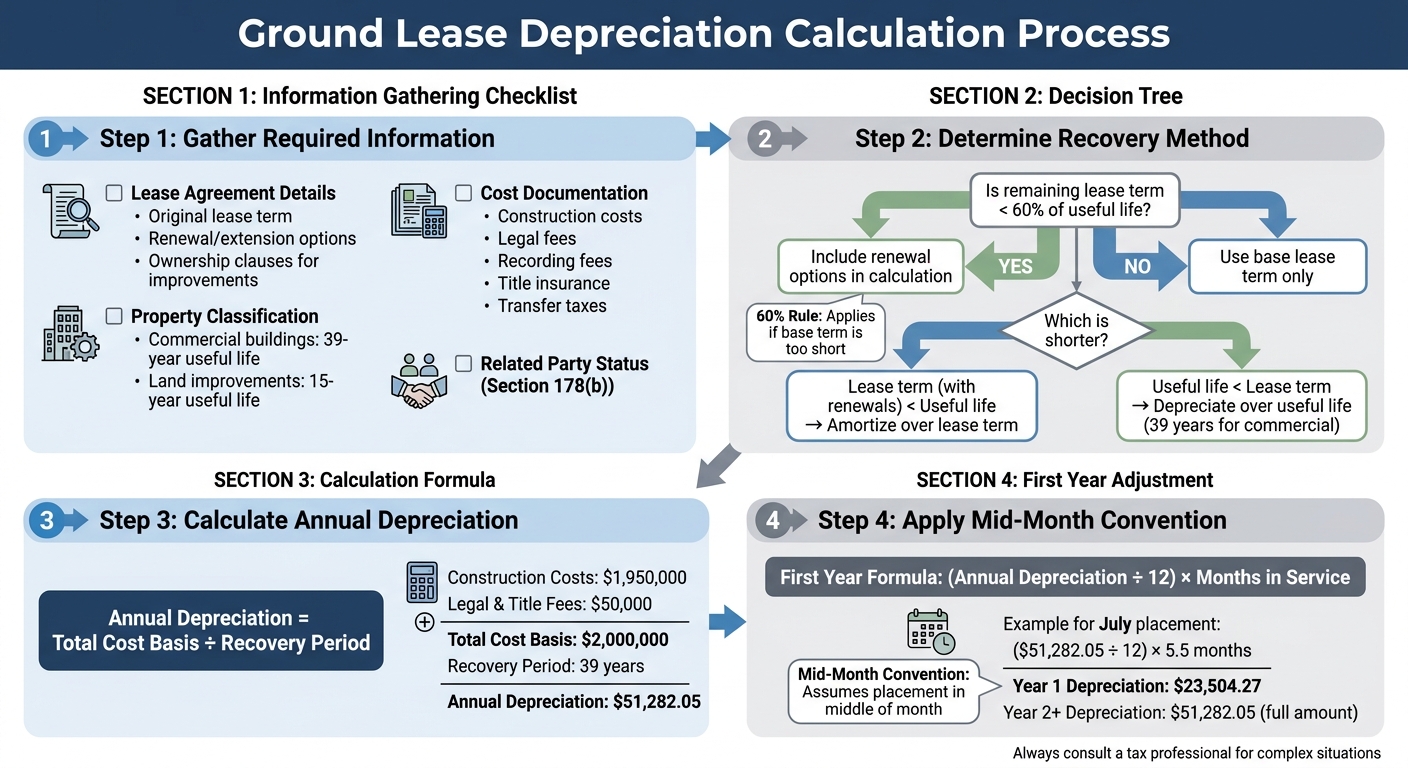

Ground Lease Depreciation Decision Tree and Calculation Guide

Information You Need to Calculate Depreciation

To get started, you'll need to gather a few key pieces of information. Begin with your lease agreement details, which should include the original lease term, any renewal or extension options, and any clauses about ownership of improvements once the lease ends [4] [8]. You'll also need detailed records of improvement costs, such as invoices, contracts, and service dates [8] [14].

Your cost basis is another critical figure. This includes the total construction costs plus any qualified closing costs like legal fees, recording fees, title insurance, and transfer taxes [16] [17]. You’ll also need to determine the useful life of the improvements - 39 years for most commercial buildings or 15 years for land improvements [8] [14]. If you’ve purchased a lease, make sure to document the total cost and allocate it across the remaining lease term and any renewal options [8].

One more thing to confirm: whether you and the lessor are considered "related persons" under Section 178(b). If you are, the IRS requires you to depreciate the improvements over their remaining useful life, regardless of the lease term [8].

Once you’ve gathered all this information, you can apply IRS recovery methods to calculate depreciation.

Applying IRS Rules to Your Calculations

The IRS uses two different recovery methods based on the specifics of your lease. If the remaining lease term (including required renewals under the 60% rule) is longer than the improvement's useful life, you’ll depreciate the cost over the asset's useful life - 39 years for most commercial buildings [3] [15]. However, if the lease term is shorter than the useful life, you’ll need to amortize the cost over the remaining lease term instead [3].

The IRS also requires you to use the mid-month convention, which treats the property as if it was placed in service in the middle of the month [16]. This impacts your first-year depreciation calculation. After that, you’ll typically use straight-line depreciation, spreading the cost basis evenly across the recovery period.

Example: Calculating Depreciation for a Ground Lease Property

Let’s walk through an example. Imagine you construct a commercial building on leased land. The construction costs total $1,950,000, and legal and title fees add another $50,000, giving you a total cost basis of $2,000,000 [16] [17]. For a commercial property with a 39-year useful life, the annual depreciation would be $2,000,000 ÷ 39, which comes out to approximately $51,282.05 per year.

Now, if the property is placed in service in July, the mid-month convention means you can only claim 5.5 months of depreciation for the first year. The calculation would be ($51,282.05 ÷ 12) × 5.5, which equals roughly $23,504.27 for Year 1 [16] [17]. Starting in Year 2, you’d claim the full annual depreciation amount until the property is fully depreciated or the lease expires. If the lease term is shorter than 39 years and meets Section 178 requirements, you’d amortize the $2,000,000 over the remaining lease term instead.

Conclusion and Key Takeaways

Summary of IRS Depreciation Rules

Ground lease depreciation depends on a few key IRS rules. Under Section 178, renewal options must be factored into the lease term if the remaining lease period is less than 60% of the useful life of the improvements [8][3]. Commercial properties are depreciated over 39 years using the straight-line method, while land improvements typically follow a 15-year depreciation schedule. For leases involving related parties, the lease term matches the remaining useful life of the improvements [8][3]. Additionally, the probability test allows renewal options to be excluded if non-renewal is deemed more likely [8][3]. These IRS guidelines are essential for ensuring accurate and compliant depreciation calculations for ground leases.

Best Practices for Managing Ground Lease Depreciation

To effectively manage ground lease depreciation, you can follow these practical steps:

- Document Lease Details: Keep thorough records of lease terms, renewal clauses, improvement costs, and closing expenses.

- Evaluate Lease Structure Early: Determine if renewal options will affect your depreciation period under the 60% rule.

- Assess Lease Acquisitions: If less than 75% of the acquisition cost is tied to the remaining lease term, renewal options should be included in depreciation calculations [8][3].

- Consult a Tax Professional: Verify related-party status and ensure the correct recovery method is applied.

- Align Tax and Financial Reporting: Regularly reconcile tax depreciation with financial reporting to avoid potential audits or investor concerns.

These practices can help streamline your depreciation management and reduce the risk of errors.

Using Financial Analysis Tools for Ground Lease Investments

Handling the intricate calculations involved in ground lease depreciation can be simplified with the right tools. The Fractional Analyst offers a range of financial analysis capabilities, including generating depreciation schedules and modeling lease scenarios. The platform also provides free downloadable templates for acquisition and development, which incorporate depreciation calculations. For ongoing management, CoreCast - The Fractional Analyst's real estate intelligence platform - makes it easier to track depreciation across multiple properties, manage assets, and ensure long-term compliance. These tools can save time and improve accuracy, making complex depreciation tasks more manageable.

FAQs

Can I use bonus depreciation on ground lease improvements?

Yes, bonus depreciation can apply to ground lease improvements if they meet the criteria for Qualified Improvement Property (QIP). This typically covers interior upgrades made to commercial buildings, enabling these costs to be written off immediately rather than depreciated over 39 years. However, to qualify, the improvements must align with specific IRS guidelines for QIP.

What happens to depreciation if my ground lease ends early?

If your ground lease ends ahead of schedule, you might need to revisit or adjust the depreciation on any improvements made to the property. An early termination can change both the depreciable basis and the timeline for those adjustments. How this is handled will depend on the lease terms and IRS regulations. It’s a good idea to work with a financial professional to ensure everything is handled correctly and stays in line with tax requirements.

How do renewal options affect my depreciation period?

When renewal options are exercised, they usually extend the lease term. This extension can affect the depreciation period of the leased asset. The depreciation period is calculated based on whichever is longer: the extended lease term (including renewal options) or the asset's useful life, depending on the specific depreciation system in use.