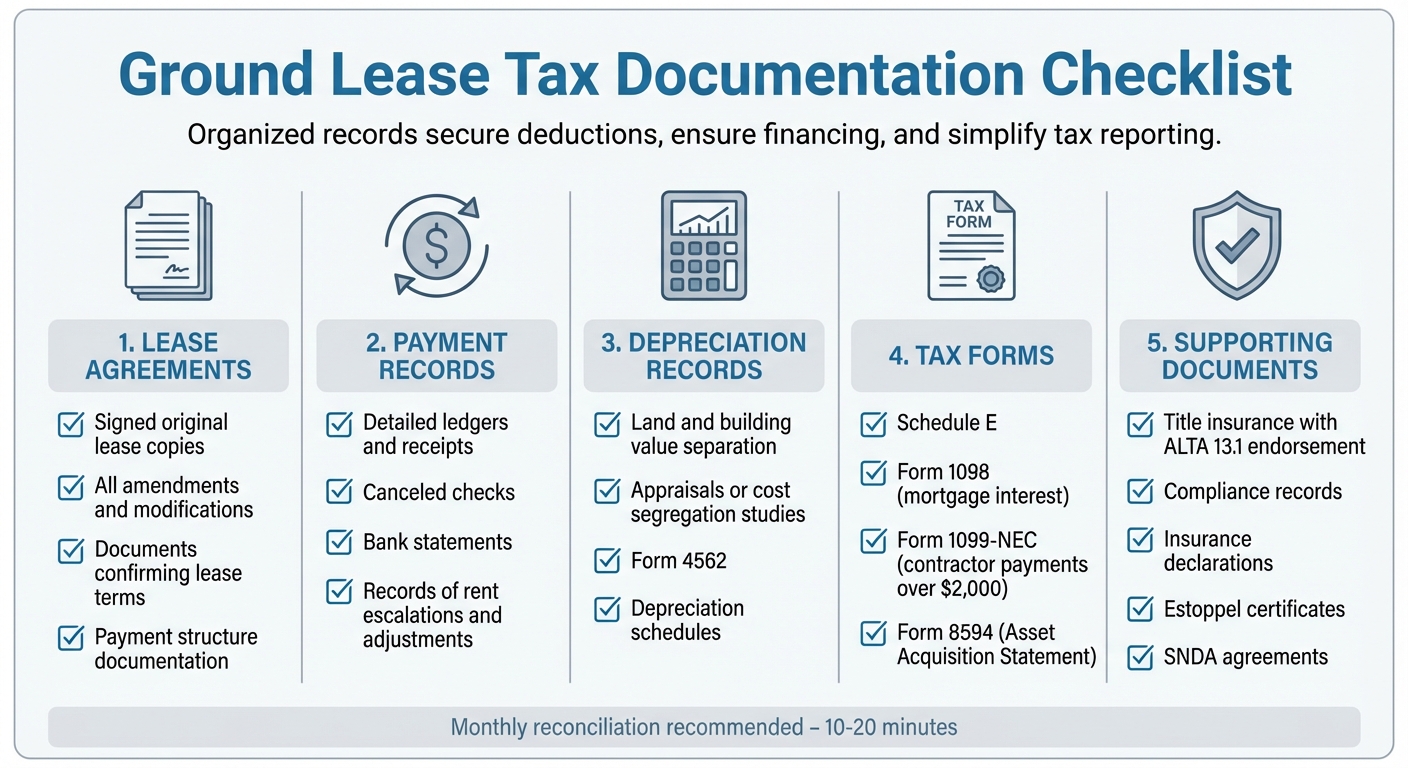

Checklist for Ground Lease Tax Documentation

Ground lease tax documentation is critical for maintaining deductions and avoiding penalties. To ensure compliance and prepare for potential IRS audits, here’s what you need:

- Lease Agreements: Keep signed copies of the original lease, amendments, and documents confirming lease terms and payment structures.

- Payment Records: Maintain detailed ledgers, receipts, canceled checks, and bank statements showing rent payments, including escalations and adjustments.

- Depreciation Records: Separate land and building values using credible methods like appraisals or cost segregation studies. Retain Form 4562 and other depreciation schedules.

- Tax Forms: File accurate forms like Schedule E, Form 1098 (mortgage interest), and Form 1099-NEC for contractor payments over $2,000.

- Supporting Documents: Include title insurance, compliance records, and insurance declarations to support leasehold rights and financing.

Proper records help secure deductions, ensure financing options, and simplify tax reporting. Stay organized by reconciling accounts monthly and categorizing expenses.

Ground Lease Tax Documentation Checklist: 5 Essential Categories

Rental Income Taxes Explained (US): Schedule E for Landlords

sbb-itb-df8a938

Ground Lease Eligibility Documentation

To claim ground lease deductions, you need to confirm that your lease aligns with IRS guidelines. This starts with verifying that the lease meets the IRS's criteria for term and use. Collect documentation that specifies the lease's duration, any renewal options, and its role in generating business or rental income.

Lease Term and Use Requirements

Your lease agreement should clearly state the lease term and any renewal options. For capital advance projects, the Department of Housing and Urban Development (HUD) mandates a minimum lease term of 75 years [6].

To qualify for deductions, the property must produce business or rental income. Keep detailed records that separate business and personal use, supported by evidence such as rental receipts or activity logs [5]. If part of a ground-leased property is used for business purposes, document the "exclusive and regular use" of that space to validate partial deductions [5].

Supporting documentation like bank statements, canceled checks, and invoices is essential to confirm lease payments [5]. For instance, the Austin Housing Finance Corporation required compliance documentation under Section 42 for Low-Income Housing Tax Credits to secure leasehold financing [6].

Proof of Written Agreement

After verifying term and use, ensure your lease agreement complies with IRS standards by providing a written, executed document. The IRS requires this agreement to confirm a legitimate lease arrangement, not a disguised sale or financing structure [5][7]. As noted by the AccountingInsights Team:

The lease agreement must also constitute a true lease, not a conditional sales contract or financing arrangement [5].

The agreement should clearly define the lease term, renewal options, and payment terms. Avoid including provisions like a bargain purchase option or automatic ownership transfer, as these could lead to IRS reclassification [5][7]. For specific tax benefits, such as 1031 exchanges, you’ll also need documentation proving the lease has at least 30 years remaining.

Keep copies of the signed lease agreement, along with any amendments or modifications, to establish the legal relationship and terms. These records are critical for validating your deductions if the IRS conducts a review.

Lease Agreement and Rental Payment Records

Keeping accurate lease and payment records is essential when claiming ground lease deductions. These documents not only validate your eligibility but also serve as critical evidence if the IRS requests verification of your tax claims. Organized and detailed records are the backbone of a solid tax deduction strategy.

Fully Executed Lease Agreement and Amendments

Start with the original lease agreement and include all subsequent amendments. These documents should clearly establish ownership of improvements for depreciation purposes. Every amendment must be properly documented to avoid any gaps in the record.

The lease should detail the rent structure and any escalation terms. This includes the base rent, advance rent, and the method of escalation - whether it's fixed, tied to the Consumer Price Index (CPI), or based on fair market value. If your lease is structured as triple net (NNN), you can typically deduct those additional expenses as business costs.

Provisions like purchase options or lease extensions should also be documented carefully. These clauses might lead to immediate transfer tax liabilities in certain areas or cause the IRS to reclassify the lease as a disguised sale. If you're extending the lease term, check whether the total duration crosses local transfer tax thresholds, which are often set at 30, 35, or 50 years.

Ground Rent Payment Receipts and Records

Maintain a thorough record of all rent payments, including receipts, bank statements, and a detailed rent ledger. It's not enough to record the initial rent amount - your records should also reflect any escalations or adjustments over time. This level of detail ensures you're prepared for an audit if needed [8].

Separate records should be kept for late fees, cancellation fees, and other charges. If you're the landlord, these are taxable income. If you're the tenant, they count as additional expenses [4][3]. For advance rent payments, such as the last month's rent paid at the beginning of the lease, the IRS requires that these be reported as income in the year they are received, regardless of the period they cover [3].

Security deposits need special attention. Clearly distinguish between deposits intended for return (which are not taxable) and those applied as final rent payments or retained due to lease violations (which are taxable as advance rent) [3]. To simplify audit preparation and keep business income separate from personal finances, consider using a dedicated bank account for all rental transactions [1].

Allocation and Depreciation Documentation

Keeping detailed lease and payment records is important, but that's just the beginning. If you're aiming to maintain tax deductions, you also need to focus on properly allocating land and building values. Why? Because this allocation directly impacts your depreciation claims. Without solid documentation to back up your method, the IRS could reject your claims altogether.

Land vs. Building Value Allocation

When determining the value of land versus buildings, it’s essential to use recognized valuation methods. The IRS and Tax Courts don’t accept arbitrary splits, like the often-used 80/20 rule [9][10]. Instead, back up your allocation with credible data sources, such as:

- County assessor cards

- USPAP-compliant appraisals

- Cost segregation studies

- Insurance replacement cost estimates [9][11][13]

If you’re looking for the most defensible option, a full-scope commercial appraisal is your best bet. While it can cost a few thousand dollars, it provides the strongest support for your allocation in the eyes of the IRS [13].

Can’t get a formal appraisal? Alternatives include a Broker’s Opinion of Value, Comparative Market Analysis, or replacement cost methods supported by tax court cases [9][11]. For purchased properties, don’t forget to include Form 8594 (Asset Acquisition Statement) and any written allocation agreements from your Purchase and Sale Agreement [13].

"For income tax purposes, every dollar shifted from land value to improvement value yields permanent tax benefits." - Lester Cook, Principal, KBKG [9]

Make sure your depreciable basis reconciles across all records to avoid audit issues. A common mistake happens when cost segregation studies don’t align with existing depreciation schedules [12].

Depreciation Schedules

Once the allocation is done, detailed depreciation schedules are essential for accurate tax filings. Keep all Form 4562 records to document your depreciation history and show consistent reporting over the years [1][3]. If you’re using a cost segregation study to claim accelerated depreciation, your records should break down assets by recovery periods, such as 5-year, 7-year, 15-year, 27.5-year, and 39-year property [12].

For missed depreciation, look-back studies are a solution. Be sure to retain Form 3115 and Section 481(a) adjustment records to account for these adjustments [12][13].

"The most common problem I see is not bad studies - it is good studies that get filed incorrectly because the CPA did not understand the deliverables." - Matthew Gigantelli, Cost Segregation Engineer, Overline [12]

Don’t overlook separate documentation for land improvements like parking lots or sidewalks. These items depreciate over 15 years, which can help fine-tune your deductions [13]. And under the One Big Beautiful Bill Act of 2025, qualifying property placed in service after January 19, 2025, will be eligible for 100% bonus depreciation, extending into the 2026 tax year [12][13].

Required Tax Forms and Reporting

Once you’ve organized your allocation and depreciation records, the next step is to tackle the necessary tax forms. Properly completing these forms ensures your ground lease deductions are secure and helps you avoid audits or rejected claims.

Schedule E and Form 4562

Schedule E (Form 1040) is where individual landlords report rental income and related expenses. You’ll report these details in Part I of Schedule E, and the net income or loss will flow to Line 5 of Schedule 1 for the 2025 tax year [14][15]. One key benefit of reporting rental income on Schedule E is that it’s generally not subject to the 15.3% self-employment tax [14][15].

Form 4562 (Depreciation and Amortization) is essential for claiming depreciation on building improvements. This form must be filed the first year you claim depreciation on a property and any year you place new assets - such as capital improvements - into service [14][15]. In subsequent years, if no new assets are added, depreciation can often be reported directly on Schedule E, Line 18 [14].

"You must also file Form 4562 (Depreciation and Amortization) with your return in the first year you claim depreciation on a property and in any year you place new assets in service." - RentalReportLab [14]

Form 1098 is used to report total mortgage interest paid, which can be deducted on Schedule E, Line 12 [14][15]. To establish the depreciable basis, refer to your Closing Disclosure or purchase agreement, and use appraisals or tax assessor records to allocate value between non-depreciable land and depreciable improvements [15][17]. Additionally, if you’re deducting travel expenses for property-related purposes, keep a detailed mileage log. For 2024, the IRS standard mileage rate for rental-related travel was 67 cents per mile [15].

For properties owned by a partnership or S-corporation, use Form 8825 instead of Schedule E to report rental real estate income and expenses [16].

Next, let’s look at how to handle payments made to contractors.

Reporting Payments to Contractors

When dealing with contractor payments, it’s essential to meet specific reporting requirements. Starting in 2026, if you pay a contractor $2,000 or more for services like repairs or maintenance, you must file Form 1099-NEC [18]. This form applies to non-employee compensation. The One Big Beautiful Bill Act raised the reporting threshold from $600 to $2,000 beginning in 2026 [18].

Form 1099-NEC must be filed with both the contractor and the IRS by January 31. No extensions are available, and payments to corporations are generally exempt from this requirement - except for attorneys or medical/healthcare providers [18][19].

"The 1099-NEC deadline is firm. No extensions are available for filing the IRS copy." - Moore Colson [18]

Before making the first payment to any vendor or contractor, collect a completed Form W-9. This ensures you have their Taxpayer Identification Number (TIN) and entity classification, which are critical for year-end reporting [18][19]. Keep track of all payments throughout the year, as even smaller payments that add up to $2,000 or more will trigger the reporting requirement [18][19]. If a contractor doesn’t provide a valid TIN, you may need to apply backup withholding at a 24% rate on future payments [18][19].

Starting in 2026, taxpayers filing 10 or more information returns (including 1099-NEC, 1099-MISC, etc.) must file electronically with the IRS [19]. Late filing penalties can range from $60 per form (if filed within 30 days) to $630 per form for intentional non-compliance [19].

Following these reporting rules is a crucial part of managing your ground lease documentation, ensuring compliance and safeguarding your deductions.

Title, Insurance, and Compliance Records

Beyond the essential lease and tax documents, there are additional records you should keep to safeguard your leasehold interest and meet lender expectations. These documents help address risks that could jeopardize tax deductions or financing arrangements.

By adding title, insurance, and compliance records to your lease and depreciation files, you create a more secure foundation for your investment.

Title Insurance and Leasehold Endorsements

It's important to obtain title insurance with an ALTA 13.1 leasehold endorsement. This type of insurance covers not only the leasehold estate but also tenant improvements, such as landscaping, permits, and professional services. Additionally, confirm that the lessor had the proper authority to grant the lease. Recording a memorandum of lease is another step to prevent potential title issues down the road.

Property and Liability Insurance Documentation

If you're operating under a triple net (NNN) lease, ensure that your insurance declarations page is always current. This document should list both the landlord and lender as additional insureds or loss payees, guaranteeing that all property-related business expenses are fully covered.

For ground leases, regular appraisals are essential. These appraisals, conducted at set intervals, ensure that improvements are insured for their full replacement cost. This not only protects your investment but also helps you stay in compliance with lender requirements.

Lender Compliance Provisions

Lender notice and cure rights provisions are critical. These allow your lender to step in and address defaults, helping preserve your depreciation deductions. Alongside this, maintain estoppel certificates - these confirm the lease term, compliance status, and absence of defaults. Another key document is an SNDA (Subordination, Non-Disturbance, and Attornment) agreement, which protects your leasehold even if the fee interest is foreclosed.

Lastly, if you're planning a 1031 exchange, make sure your lease has at least 30 years remaining on its term. Without this, your leasehold interest won't qualify.

"The 'financeability' of a ground lease is one of its most important features" [2].

Final Checklist

To wrap up, here’s what you need to ensure your file is complete and ready for accurate ground lease tax reporting:

Good documentation is your best friend when it comes to tax reporting. As Thomas Castelli, CPA at The Real Estate CPA, emphasizes:

"Keep all receipts, invoices, and lease documents well-organized. If you're ever audited, the IRS will want to see them" [8].

Here’s what to include:

- Lease agreements and amendments: Maintain the fully executed lease and any modifications.

- Income records: A detailed rent ledger showing all income received, along with matching payment records.

- Expense documentation: Property tax bills, insurance declarations, and receipts for repairs and maintenance are crucial, especially for triple-net (NNN) leases where these costs fall on you.

Depreciation records are another critical area. Make sure you have documents that clearly separate land value (non-depreciable) from building or improvement value (depreciable over 39 years for commercial properties). Keep Form 4562, cost allocation details, and invoices for improvements handy. Don’t forget Form 1098 for mortgage interest and W-9 forms for any contractors paid $2,000 or more.

Lastly, adopt a monthly habit: spend 10–20 minutes reconciling your LLC bank account, categorizing expenses, and uploading receipts. This small effort saves you from scrambling during tax season [20]. Before the year ends, create a concise, one-page summary of improvements, listing dates, vendors, and costs.

FAQs

How do I prove my ground lease is a “true lease” for IRS purposes?

To ensure your ground lease is recognized as a "true lease" by the IRS, it must align with the criteria outlined in IRS Revenue Procedures 2001-28 and 2001-29. Here’s what to check:

- No bargain purchase option: The lease cannot include an option to purchase the asset for less than its fair market value.

- Residual value requirements: The asset must retain at least 20% of its original value at the end of the lease, with the lessor assuming all associated risks.

- Profitability beyond tax benefits: The lease should generate profit independently of tax advantages, meeting specific pre-tax cash flow and equity investment benchmarks.

Meeting these conditions ensures the IRS recognizes the lease as a legitimate "true lease."

What’s the best way to document land vs. building value for depreciation?

The most effective way to divide land and building value for depreciation purposes is by using a logical, well-documented approach. This might involve examining the purchase agreement, referencing an appraisal, or using local property tax assessments to figure out the land-to-building ratio. If none of these are accessible, getting an independent appraisal is a good alternative. Remember, consistency and thorough documentation are crucial since only the building's value qualifies for depreciation under IRS guidelines.

Which tax forms do I need for ground lease deductions and contractor payments?

You'll need Form 1098 to report mortgage interest and Schedule E to detail rental income and expenses. This includes deductions like ground lease costs and contractor payments. Make sure all your documentation is accurate and complete to ensure proper tax filing.