Ultimate Guide to Exit Cap Rates

Exit cap rates are essential for estimating the future sale price of commercial properties. They help investors project a property's terminal value by dividing the projected net operating income (NOI) by the estimated sale price. This metric is key for financial modeling, influencing internal rate of return (IRR) and overall investment feasibility.

Here’s what you need to know:

- Exit cap rate formula: Projected NOI ÷ Terminal Value.

- Comparison with entry cap rates: Exit cap rates typically account for market risks, property aging, and future investor expectations, making them higher than entry cap rates.

- Factors affecting exit cap rates: Interest rates, market trends, property age, asset class, and risk tolerance.

- Importance in financial modeling: Small changes in exit cap rates can significantly impact projected returns, making conservative assumptions critical.

For accurate projections, adjust exit cap rates upward by 0.5%-1.0% above current market levels to account for risks. Use normalized NOI and revisit assumptions regularly to align with market conditions. Exit cap rates directly impact your exit strategy and investment outcomes, so approach them with care.

How To Set The Exit Cap Rate On A Real Estate Deal

sbb-itb-df8a938

What Is an Exit Cap Rate?

Entry Cap Rate vs Exit Cap Rate Comparison Chart

An exit cap rate (also known as a terminal or reversion cap rate) represents the expected rate of return on a commercial property at the end of your holding period. This rate is used to estimate the property’s terminal value - its projected selling price at the time of exit [1][5].

Unlike current market conditions, which are known, the exit cap rate involves forecasting market dynamics five, seven, or even ten years into the future. It’s calculated by dividing the projected net operating income (NOI) for the year of sale by the estimated selling price [1][6].

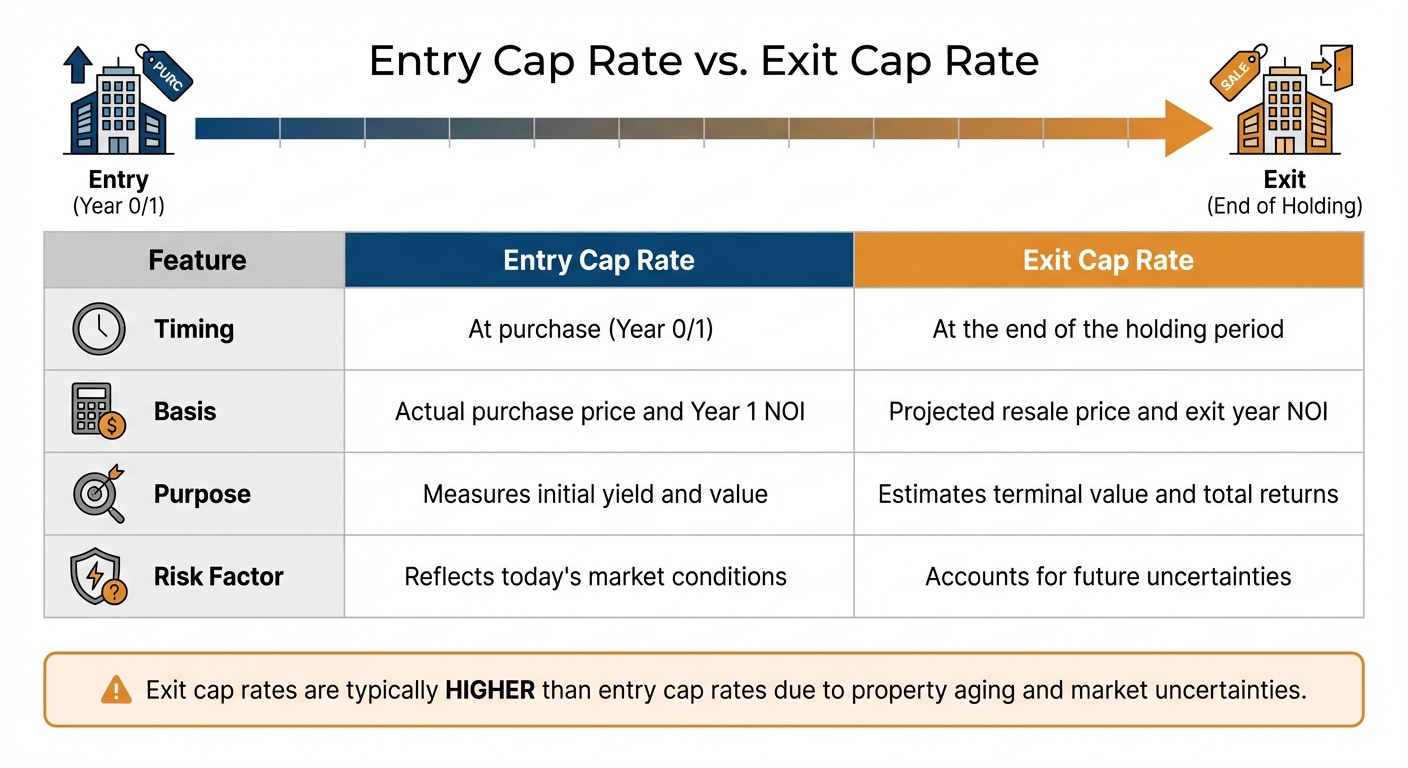

Exit Cap Rates vs. Entry Cap Rates

To get a clearer picture of exit cap rates, it’s helpful to compare them with entry cap rates.

The entry cap rate, often called the "going-in" cap rate, measures the initial yield on a property. It’s calculated by dividing the first-year NOI by the purchase price [1][2]. This metric reflects the relationship between the price paid and the property’s current income under today’s market conditions.

In contrast, the exit cap rate is a forward-looking measure. It estimates the yield at the time of sale, factoring in future market uncertainties like property aging, evolving investor expectations, and potential market shifts. Because of these risks, exit cap rates are generally higher than entry cap rates.

| Feature | Entry Cap Rate | Exit Cap Rate |

|---|---|---|

| Timing | At purchase (Year 0/1) | At the end of the holding period |

| Basis | Actual purchase price and Year 1 NOI | Projected resale price and exit year NOI |

| Purpose | Measures initial yield and value | Estimates terminal value and total returns |

| Risk Factor | Reflects today’s market conditions | Accounts for future uncertainties |

This comparison highlights how exit cap rates are essential for planning and forecasting future returns.

Why Exit Cap Rates Matter for Investors

Exit cap rates play a critical role in determining a property’s projected resale value, which directly impacts key metrics like internal rate of return (IRR) and overall cash returns. For instance, if you assume a 5.0% exit cap rate but the market shifts to 6.0%, the property’s value could drop significantly, hurting your returns.

For investors, this metric is essential in underwriting and exit strategy planning. It allows you to test different scenarios and evaluate how sensitive your returns are to changes in market conditions. Choosing the right exit cap rate requires balancing optimism with caution, ensuring your projections align with realistic market trends. This careful approach lays the groundwork for accurate financial modeling and a well-thought-out exit strategy.

How to Calculate an Exit Cap Rate

Now that we’ve covered why exit cap rates matter, let’s dive into the details of how to calculate them. The calculation helps determine the expected return on your property at the time of sale by using projected figures for net operating income (NOI) and terminal value. It’s a simple process once you understand these two key components.

Exit Cap Rate Formula

The formula to calculate an exit cap rate is:

Exit Cap Rate = Projected NOI ÷ Terminal Value

Here’s what the terms mean:

- Projected NOI: The net operating income for the final year of your hold period.

- Terminal Value: The estimated sale price of the property at the end of that period.

To express the result as a percentage, multiply it by 100. For example, if your projected NOI is $500,000 and the terminal value is $10,000,000, dividing these gives you 0.05. Multiply by 100, and you get an exit cap rate of 5.0%.

Example Calculation

Let’s walk through an example. Say you’re holding a multifamily property for seven years. By Year 7, you estimate the property will generate $750,000 in NOI. After analyzing the market, you project the terminal value to be $12,500,000.

Using the formula: $750,000 ÷ $12,500,000 = 0.06, or 6.0%. This means you’re assuming a 6.0% exit cap rate when it’s time to sell.

If your entry cap rate was 5.5%, this 50 basis point increase represents cap rate expansion. This is a conservative approach that accounts for factors like the property aging and potential market changes over time. A higher exit cap rate lowers the implied property value, which is a common way to add a safety buffer to your financial projections.

Factors That Affect Exit Cap Rate Assumptions

Grasping what influences exit cap rate assumptions is crucial for precise financial modeling and planning an effective exit strategy. These rates differ based on property specifics and market dynamics, requiring tailored assumptions for reliable projections.

Market Trends and Economic Conditions

Economic factors are a major driver of exit cap rates. Interest rates are especially critical since they directly impact the returns investors expect. For instance, in November 2024, the 10-year U.S. Treasury rate stood at 4.32%, leading to an implied cap rate spread of 382 basis points - well above the historical average of 200 to 250 basis points [4]. When risk-free rates increase, investors seek higher returns from real estate, causing cap rates to rise.

Market cycles also play a big role. During economic growth, cap rates often compress as competition for assets heats up. Conversely, during downturns, cap rates expand because buyers become more cautious. It’s worth noting that recorded sales data often lags by months, meaning you might need to anticipate trends rather than rely solely on past data - especially in times of interest rate volatility [7]. To refine your assumptions, benchmark them against historical spreads and consider using tools like the Band of Investment for cross-checking [4][7].

Property Age and Asset Class

Property-specific traits also heavily influence exit cap rate assumptions. For example, a Class A office building in a major city typically has a lower exit cap rate than a Class C multifamily property in a smaller market. Urban properties tend to have lower cap rates due to their higher liquidity and lower perceived risk [4].

Different property types react differently to market shifts. By late 2024, projections for cap rate changes by the end of 2025 showed clear differences: industrial properties were expected to drop by 40 basis points, office properties by 20 basis points, retail by 35 basis points, and multifamily by 25 basis points [4]. Older properties with deferred maintenance typically require higher exit cap rates to account for future capital expenses. When calculating terminal value, ensure your Net Operating Income (NOI) is stabilized - reflecting typical vacancy rates and market-level expenses rather than short-term fluctuations [4].

Risk Adjustments and Investor Strategy

Once market trends and property characteristics are factored in, adjust for risk tolerance and your investment approach. Use a normalized NOI, excluding any one-time income spikes or deferred maintenance, for a more accurate calculation [4]. Cross-referencing your assumptions with current spreads to risk-free rates and historical data ensures your exit cap rate reflects both the property's risk profile and your planned hold period strategy.

Using Exit Cap Rates in Financial Models

Applying exit cap rates in financial models is crucial for creating realistic exit strategies. These rates play a key role in real estate financial models, especially when determining terminal value in a discounted cash flow (DCF) analysis. To estimate terminal value, divide the final year's stabilized net operating income (NOI) by the exit cap rate. Then, discount it back to the present value to calculate return metrics.

Exit Cap Rates in Sensitivity Analysis

Sensitivity analysis highlights how even small changes in exit cap rates can significantly alter financial outcomes. For example, testing exit cap rates between 4.2% and 5.2% in 50 basis point increments provides a clear picture of downside risk. In one scenario, a property expected to sell for $142.9 million at a 4.2% exit cap rate could see its value drop to $115.4 million at a 5.2% rate. That’s a $27.5 million reduction - a 19% loss in value [8]. These tests emphasize just how critical exit cap rate assumptions are, particularly when assessing risk and return.

Impact on IRR and Investor Returns

Exit cap rate assumptions can have a disproportionate effect on internal rate of return (IRR). This is because terminal value often represents a significant portion of total returns, especially in value-add and development projects. A higher exit cap rate results in a lower sale price, reducing disposition profits and compressing both IRR and equity multiples. To avoid overly optimistic projections, many investors now use "reversion cap rates" that are 0.5% to 1% higher than current market rates. This approach adds a margin of safety to their models [8]. Including both a base case with market-level exit cap rates and a downside case with elevated rates helps evaluate whether an investment can still meet return goals under less favorable conditions.

How to Set Exit Cap Rates

Setting an appropriate exit cap rate is crucial for accurate financial modeling. This decision directly impacts metrics like IRR and overall cash returns. To get it right, you need to balance market data with risk management. Start by analyzing current cap rates for similar properties, then adjust for the expected holding period and anticipated market conditions at the time of sale. It’s also important to use normalized NOI, which reflects stabilized property performance [4]. From there, consider how conservative versus aggressive strategies might influence your assumptions.

Conservative vs. Aggressive Exit Strategies

The choice between conservative and aggressive strategies can lead to drastically different outcomes. Conservative investors often add 0.5% to 1.0% to the current market cap rate. This adjustment accounts for factors like property aging and potential market softening [8]. It’s a way to build a buffer against downside risks.

"Underselling and then over-delivering is key; base your modeling on conservative exit values to secure project success." - Willowdale Equity [8]

On the other hand, aggressive strategies rely on cap rate compression or simply use current market rates without adjustment. While this can make projected returns look better on paper, it also increases exposure to risk if market conditions shift. The best approach depends on your strategy and risk tolerance. For example, value-add investors might justify using tighter exit cap rates if they’re significantly improving the asset, while opportunistic buyers should leave more room for error.

Using Professional Tools and Resources

Modeling exit cap rates accurately requires both market insights and advanced financial analysis. Programs like the Wharton Online and Wall Street Prep Real Estate Investing & Analysis Certificate teach investors how to project cap rates and perform thorough due diligence [1]. Additionally, platforms such as The Fractional Analyst provide tailored underwriting services and custom financial models. These tools incorporate market-specific exit cap rate assumptions and help stress test different scenarios. This kind of support is especially useful when evaluating properties across various asset classes, each with its own cap rate trends. By leveraging these resources, you can ensure your exit strategies align with market realities and your investment goals.

Wrapping It Up

This guide has walked you through the essentials of calculating, adjusting, and applying exit cap rates in commercial real estate investing. These rates play a central role in determining projected sale prices, influencing IRR, and assessing whether a deal makes financial sense. We've broken down the formula (Exit Value = Year-of-Sale NOI ÷ Exit Cap Rate), explored the factors that shape your assumptions - like market trends, property age, and economic conditions - and highlighted how to use them in financial models.

Here’s the key takeaway: model with caution. Always adjust your exit cap rate upward by at least 0.5% to 1.0% above current market levels. This accounts for asset aging and potential shifts in the market, helping you mitigate risks and maintain realistic projections [3]. At the same time, focus on growing NOI through operational improvements to counteract cap rate expansion [3].

Market conditions don’t stay static, and neither should your assumptions. Keep revisiting your projections during the holding period, factoring in fresh data like comparable sales, interest rate trends, and shifts in asset classes. Using normalized NOI ensures your calculations stay accurate and reliable [4][7].

Whether you're targeting value-add opportunities or sticking to core investments, the strategies outlined here will help you make well-informed choices. For additional support, platforms like The Fractional Analyst offer customized underwriting services and financial models. These tools incorporate market-specific exit cap rate assumptions, helping you stress-test scenarios and align your exit strategy with your goals.

FAQs

What’s a realistic exit cap rate to use?

A realistic exit cap rate for 2026 generally ranges between 4% and 6%, influenced by factors such as market conditions, property type, and associated risk. Lower cap rates often reflect lower risk and more stability, especially in top-tier markets. On the other hand, higher cap rates can signal greater risk or markets that are less stable. It's crucial to evaluate the unique circumstances of your investment when determining the appropriate exit cap rate.

How does the exit cap rate affect IRR?

A higher exit cap rate decreases a property's terminal value, which can lead to a lower Internal Rate of Return (IRR). On the flip side, a lower exit cap rate boosts the terminal value, potentially increasing the IRR. This dynamic underscores how crucial it is to estimate exit cap rates accurately when analyzing real estate investments.

Should I use stabilized or trailing NOI at exit?

You should use stabilized NOI at exit because the exit cap rate is tied to the projected net operating income at the end of the holding period. This method provides a clearer picture of the property's resale value by taking into account its anticipated performance at that point in time.