How Appraisal Reports Impact CRE Financing

In CRE lending, the appraisal can change your loan amount, leverage, DSCR, closing conditions, and timeline. If value comes in low, proceeds often drop. If NOI support is thin, lenders may tighten structure, ask for more equity, or delay closing.

Here’s the short version:

- I see appraisals act as a lender checkpoint for value, cash flow, and collateral support

- A $10,000,000 value at 70% LTV points to $7,000,000 in senior debt

- If NOI is weaker than expected, DSCR and debt yield can fall, which often leads to a smaller loan

- Lenders review cap rates, comps, rent assumptions, expenses, property condition, and subject-to items

- Weak spots like stale data, unsupported adjustments, cash flow gaps, or wrong appraisal scope can slow approval

- In tighter property sectors, lenders may underwrite at 50%–60% LTV and 1.45x–1.65x DSCR

- For many regulated CRE loans above $500,000, a full appraisal is usually part of the credit process

If I had to boil it down to one point, it’s this: when the appraisal and the lender’s underwriting model match, the deal has a smoother path to close. The biggest issues usually come from poor support, not from the report format itself.

| Area | What lenders check | What can happen if it’s weak |

|---|---|---|

| Value | Comps, cap rates, reconciliation | Lower proceeds |

| Cash flow | Rents, vacancy, expenses, NOI | Tighter DSCR and debt yield |

| Property | Condition, deferred maintenance, use | Reserves, holdbacks, more equity |

| Scope | As-is vs. as-complete/as-stabilized | Report revision and closing delay |

I’d frame the whole article this way: the appraisal is not just a file item. It directly affects whether your CRE loan closes on current terms, on tighter terms, or not at all.

What Lenders Review in an Appraisal Report

Lenders focus on the parts of an appraisal that affect value, cash flow, and closing conditions. Those points shape loan proceeds, deal structure, and how long closing may take.

Market Value, Valuation Methods, and Reconciliation

After the appraiser gives a value conclusion, lenders look at how that number was reached. Most commercial appraisal reports use three main methods: the Sales Comparison Approach, the Income Capitalization Approach, and the Cost Approach. From there, lenders check whether the final reconciliation lines up with the property type.

For office, retail, and other income-producing assets, the income approach usually gets the most weight. For special-use properties, the cost approach matters more. If the appraiser’s reasoning doesn’t fit the asset, underwriters see that as a red flag.

Old valuation support can also create problems. If the comps or market data are stale, the lender may be working from a value conclusion that no longer fits current pricing.

Lenders also compare exit cap rates to current market conditions. In 2025, office assets were being underwritten with exit cap rates between 7.25% and 8.50%, while multifamily and industrial were closer to 6.00% to 6.75%. [1] If the cap rates in the report trail the market, underwriters often stress the value before they approve the loan.

Income Assumptions, Property Condition, and Highest and Best Use

Once the lender is comfortable with the valuation method, the next step is the math behind NOI. When income drives value, lenders dig into rent, vacancy, and expense assumptions.

They’re looking for things like:

- Gross rents that look higher than they should because of concessions

- Management fees set below market

- Expense ratios that come in too low compared with similar properties

Those issues can make NOI look stronger than it is and push value above what the market will support. [2]

Property condition matters too. Deferred maintenance can lead to reserves or a holdback, which can cut loan proceeds. And highest and best use can shift the whole picture. If the appraiser says the property’s current use is still the best use, but the market points in another direction, the value conclusion may be too high.

That’s showing up a lot with office properties. Because vacancy has stayed high and obsolescence risk hasn’t gone away, many lenders are now underwriting office with alternative use value in mind. [1] In plain English, if the building no longer fits current demand, the value may lean more toward land value or redevelopment potential than its present use.

Assumptions, Limiting Conditions, and Subject-To Items

Even a strong value conclusion can weaken if the report leans on unresolved conditions. Subject-to items have to be cleared before closing.

Lenders also pay close attention to limiting conditions and any assumptions that narrow the appraisal’s scope. If the report relies on inputs that haven’t been verified, or on conditions that still need to be met, underwriters may add more closing conditions or cut the loan size.

sbb-itb-df8a938

How Appraisal Findings Change Loan Terms and Timing

Favorable vs. Adverse CRE Appraisal Outcomes: Key Loan Metrics Compared

Once the appraisal lands in underwriting, it starts to shape the loan in very direct ways. The numbers in the report affect proceeds, loan structure, and how fast the deal can get to closing.

How a Lower Value Reduces Proceeds and Tightens Structure

If the appraised value comes in below the borrower’s expectation, the lender cuts the loan amount. That shortfall usually has to be filled by the borrower with more equity.

A lower value can also mean a tighter capital stack. For office assets in 2024–2025, maximum LTVs have dropped to 50%–60%, while DSCR requirements have moved up to 1.45x–1.65x. Multifamily and industrial still tend to be underwritten around 60%–70% LTV with minimum DSCRs of 1.30x–1.50x. [1]

How Stronger Support Improves Underwriting Confidence

A well-supported appraisal tends to reduce back-and-forth. When income support is clear, comps are current, and the reconciliation makes sense, underwriters can move with more speed and less hesitation.

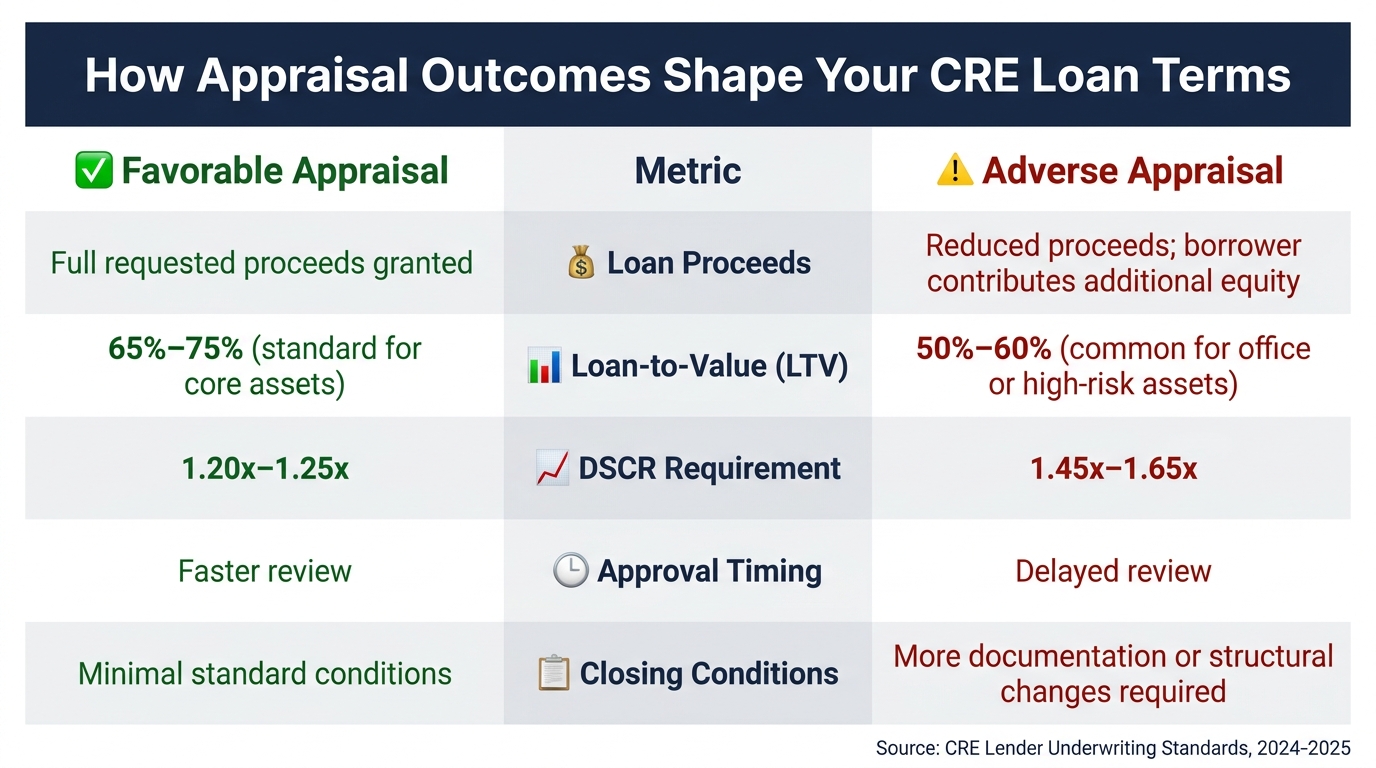

Favorable vs. Adverse Appraisal Outcomes: A Side-by-Side Comparison

The same appraisal can help push a deal forward or lead to a tighter structure.

| Metric | Favorable Appraisal Finding | Adverse Appraisal Finding |

|---|---|---|

| Proceeds | Full requested proceeds granted | Reduced proceeds; borrower brings additional equity [2] |

| Loan-to-Value (LTV) | 65%–75% (standard for core assets) [1] | 50%–60% (common for office or high-risk assets) [1] |

| DSCR Requirement | 1.20x–1.25x [1] | 1.45x–1.65x [1] |

| Approval Timing | Faster review | Delayed review |

| Closing Conditions | Minimal standard conditions | More documentation or structure changes [4] |

When a report falls short, the drag often comes from fixable problems like data gaps, stale support, or scope issues.

Common Appraisal Problems That Disrupt CRE Financing

Most appraisal delays come down to a handful of fixable support gaps. In plain English, the issue usually isn’t the valuation idea itself. It’s the backup behind it. When that support is thin, lenders ask more questions, underwriting gets pulled back in, and the file slows down.

Stale Data, Weak Comps, and Unsupported Adjustments

Weak comps and unexplained adjustments are a fast way to get underwriter pushback. The 99 Broadway retail condominium shows how bad that gap can get: a 2026 sale at $32 million versus a 2016 appraisal near $150 million [3].

Some adjustment categories come up again and again:

- Property condition: 5% to 10%

- Quality levels: 2.5% to 5%

- View and location: about 1% positive or negative

Those ranges aren’t the problem by themselves. The problem starts when the report doesn’t clearly show why the appraiser used them. If an adjustment looks like it came out of thin air, the lender is likely to push back, slow the file, and ask for more support before accepting the value.

Inconsistent Cash Flow Analysis and Missing Documentation

A common underwriting problem is a mismatch between the appraisal’s NOI and the lender’s model. That sounds small, but it can hold up the whole deal.

The trouble usually starts when the appraisal projects revenue growth that the market doesn’t support or keeps expenses too low by leaving out capital expenditures, tenant improvement allowances, and leasing commissions. It also shows up when rent and expense terms in the report don’t match the actual lease abstracts. At that point, the lender has to stop and reconcile the gap before the loan can move ahead.

Scope Mismatch Between the Appraisal and the Loan Purpose

A scope mismatch can slow closing even when the rest of the report looks fine. If the appraisal is based on an as-is premise but the loan calls for an as-complete or as-stabilized view, the lender may need a revised report before moving forward.

That kind of mismatch is frustrating because it often could have been avoided at the start. If the scope doesn’t line up with the loan purpose, the report may not answer the lender’s main question.

How to Cut Appraisal-Related Financing Friction

Once the report is in motion, the focus changes. It’s no longer just about value on paper. It’s about getting the loan through without avoidable slowdowns.

Order the Right Scope and Review the Report Before Final Credit Action

Match the appraisal scope to the loan purpose before you place the order. For regulated deals, keep the scope FIRREA-compliant [2].

Then read the report with a practical eye. Look for property details that can affect marketability and value. A short internal review before final credit action can catch missing items early, before they turn into delays or force a re-trade.

After the scope is set, the next step is simple: check whether the appraisal’s income and cap-rate assumptions line up with the lender model.

Close Valuation Gaps Early With a Consistent Underwriting Framework

Once the report is back, compare the appraiser’s NOI, cap rates, and market assumptions against your underwriting model as a standard process step, not a second appraisal review.

Underwriting is tighter right now across office, multifamily, industrial, retail, and hospitality, so appraisal assumptions need to line up with lender stress levels [1]. If they don’t, the lender model and the appraisal can drift apart. That’s when deals get stuck while the team sorts out the gap.

A steady underwriting framework helps cut that back-and-forth. Teams that use one spend less time fixing mismatches and more time moving deals ahead.

Conclusion: Report Quality Drives Loan Execution

When the appraisal and underwriting model tell the same story, credit moves faster.

FAQs

What if my appraisal comes in low?

A low commercial real estate appraisal can shrink your LTV ratio. And that can lead to a bigger equity contribution or extra cash at closing to fill the gap.

Start by reviewing the appraisal report line by line. Check for mistakes in square footage, renovation history, or the comparable properties the appraiser used. You’ll also want to make sure the appraiser accounted for current market conditions and any property-specific improvements that could change the valuation.

Can a weak appraisal delay closing?

Yes. If an appraisal comes in lower than expected, it creates a gap between the purchase price and the home’s market value.

That gap can slow down closing while the buyer and lender try to renegotiate the price or rework the deal. Appraisal problems, including mistakes in the report or signs that the home’s value is slipping, can also reduce financing choices and bring the process to a halt.

Do all CRE loans need a full appraisal?

Yes. Lenders require formal appraisals for most commercial real estate loans, including purchases, refinances, and construction financing.

Why? They serve a few clear purposes:

- They help lenders meet regulatory rules

- They confirm the property’s market value

- They lower lending risk

- They help shape loan terms

In some early-stage reviews, a lender may use a more flexible valuation service. But when it’s time to move forward with the loan, a formal, USPAP-compliant appraisal is the standard.