How to Negotiate Earnest Money Terms

In most commercial real estate deals, earnest money comes down to 3 things: how much you put up, when it goes hard, and when you can get it back.

If I were negotiating a PSA today, I’d focus on one goal first: match the deposit to the deal risk. In many U.S. CRE deals, the buyer starts with 1% to 2% at signing, then adds more after due diligence so the total lands around 3% to 5%. Higher-risk deals like land, hotels, and distressed sales often go above that.

Here’s the short version:

- Buyers should keep the first deposit refundable during due diligence.

- Sellers should use deposit size and timing to test whether the buyer is serious.

- Both sides should pin down deadlines, notice rules, escrow terms, interest, and default language in the PSA.

- Most disputes come from vague wording around contingencies, hard dates, and refund rights.

A few deal points matter more than the rest:

- Initial deposit: Often due within 1 to 5 business days

- Soft period: Usually lasts through due diligence

- Hard date: The point when the deposit becomes non-refundable

- Closing treatment: The deposit is usually credited toward the purchase price

- Escrow: Funds should go to a neutral third party, not straight to the seller

| Deal point | What I’d watch |

|---|---|

| Deposit amount | Keep hard money within the dollar loss you can live with |

| Timing | Tie each deadline to the effective date |

| Refund rights | List each contingency clearly in the PSA |

| Seller protection | Limit buyer exit rights after diligence ends |

| Escrow terms | State who holds funds, who gets interest, and how disputes are handled |

If I had to boil the whole topic down to one line, it would be this: the best earnest money deal is not the biggest deposit - it’s the one with clear timing, clear exit rights, and clear default rules.

The Main Terms You Negotiate

Once the deposit structure is in place, the next step is working through the terms that shift risk. This is where the deal starts to feel real. The main pressure points are the deposit trigger, the hard date, refund rights, interest, and the closing credit. Each one moves the balance either toward buyer flexibility or seller certainty.

Amount, Timing, and Go-Hard Dates

The deposit amount usually depends on the asset class, the deal size, and how competitive the market is. In seller-friendly markets, sellers may push for part of the deposit to become non-refundable at signing [1]. Land and development deals often come with higher deposits because the timelines are longer and the seller gives up more time and deal options while the property is tied up [1][2].

A tiered deposit setup often works best. The buyer puts down a refundable initial deposit when the PSA is signed, then adds a larger hard deposit at the end of the diligence period. Initial deposits are usually due within 1 to 5 business days after PSA execution [1][2]. That timing matters a lot. It tells you how long the buyer can still walk away and when the deposit starts giving the seller real leverage.

Refundability, Interest, and Closing Credits

After timing, the next issue is straightforward: what comes back to the buyer, who gets any interest earned in escrow, and how the deposit is handled at closing.

During diligence, the deposit should be refundable if there are express contract failures. After the hard date, it should be lost only if the buyer defaults and the seller has not breached the agreement [1][2][3].

The PSA and escrow instructions should also spell out who receives escrow interest. They should also say that the deposit is credited toward the purchase price at closing [2][3].

These terms shape the buyer and seller playbook in the next section, whether that means protecting refund rights or using the deposit to lock in certainty.

sbb-itb-df8a938

How Buyers Should Negotiate Earnest Money Terms

Once the deposit setup is in place, the buyer’s next job is simple: protect the right to get that money back before the hard date.

Set a Deposit Structure That Matches Due Diligence Risk

Your soft period should line up with your due diligence timeline. And your hard deposit should stay within the amount you can afford to lose.

That’s the key point. Before you agree to any deposit figure, decide the maximum dollar amount you could live with losing if the deal falls apart outside your contingencies. That number should be your cap for hard money, not the seller’s opening ask.

If your downside limit is $50,000, don’t talk yourself into a $150,000 hard deposit just because the broker says it’s “market.” A hard deposit is money at risk. Treat it that way.

Those protections, though, only hold up if the notice rules are handled exactly right.

Use Contingencies and Notice Rules to Protect Refund Rights

Your deposit is protected by clear contingency language, not by assumptions or handshake logic.

Spell out each contingency by name: financing, title and survey, environmental, and zoning. Then connect each one to a firm deadline and a clear termination notice process [1][2]. If the contract says notice must be sent to the seller or escrow agent before the deadline, do exactly that. No late email. No vague heads-up call. No “we thought they knew.”

The table below shows the main contingency types buyers usually negotiate in a standard CRE transaction to protect refund rights:

| Contingency Type | What It Covers | Typical CRE Timing | Refundable? |

|---|---|---|---|

| Due Diligence | Inspections, financials, and general feasibility | 30–90 days | Yes, before deadline [2] |

| Financing | Ability to secure debt on acceptable terms | 30–60 days | Yes, if lender denies [2] |

| Title & Survey | Liens, easements, and boundary encumbrances | 15–30 days | Yes, if defects found [1] |

| Zoning/Entitlement | Confirmation that intended use is legally permitted | 60–180+ days | Often negotiated |

| Post-diligence non-refundable deposit | No remaining contingencies; buyer committed to close | Post-DD to closing | No - forfeited on default [2] |

A good rule of thumb: terminate at least two business days before the hard date. That small cushion can save you from a missed deadline, a wire issue, or a notice dispute that turns into a mess.

Model the Downside Before You Agree to Hard Money

Before you accept a hard deposit, pressure-test the deal.

Run through failure cases tied to the lender, appraisal, title, and survey before the deposit goes hard. Then add your sunk due diligence costs to that downside math. It’s one thing to lose a deposit on paper. It’s another to lose the deposit plus legal fees, third-party reports, lender costs, and time.

That exercise gives you a cleaner read on your actual risk before you commit.

How Sellers Should Negotiate for Certainty Without Losing Buyers

Earnest Money Terms: Seller-Friendly vs. Balanced CRE Deal Structure

For sellers, the goal flips. You want tighter refund rights without driving away a serious buyer. Put simply: once the PSA is signed, the deposit should make up for taking the asset off the market.

Use Deposit Size and Timing to Qualify the Buyer

The easiest way to test buyer intent is deposit size. A buyer willing to put up more money, sooner, is usually showing real conviction.

In competitive markets, sellers can often push for a total deposit of 5% or more, with an initial wire of 1% to 2% due within 3 to 5 business days after PSA execution, and the rest going hard at the end of the due diligence period [3][1].

A small deposit, or one that arrives late, can be a warning sign. It often points to a buyer who wants control of the deal without much risk. On land, development, or distressed assets, though, a tiered deposit setup tends to work better than demanding a big number on day one. Start lower, then require the deposit to step up once the diligence window ends [2]. That gives the seller stronger commitment at the moment the buyer has had time to review the deal.

The due diligence window matters too. A shorter period tells the market you expect a prepared, well-capitalized buyer. If someone asks for a long diligence period on a stabilized asset, that should get your attention.

Once you've tested commitment through deposit size and timing, the next step is protecting that leverage in the extension and default terms.

Structure Extensions, Default Remedies, and Liquidated Damages Carefully

Extensions are one of the easiest places for sellers to give up leverage. If you grant extra time, you should get paid for it. That usually means an added non-refundable deposit or extension fee. Otherwise, the buyer gets more time tied to your property with no added cost [3][4].

In many commercial PSAs, earnest money acts as liquidated damages. So if the buyer defaults, the seller's main remedy is usually the deposit. That's why the PSA needs to define both default and the hard date with no gray area.

Refund rights should also rest on objective contract triggers, not broad judgment calls. Language like "satisfactory due diligence" gives buyers too much room to walk. A better approach is to tie termination rights to specific items, such as a title defect that can't be cured, a major environmental issue, or a lender denial in writing [3]. The tighter the wording, the harder it is for a buyer to exit without a clear contract basis.

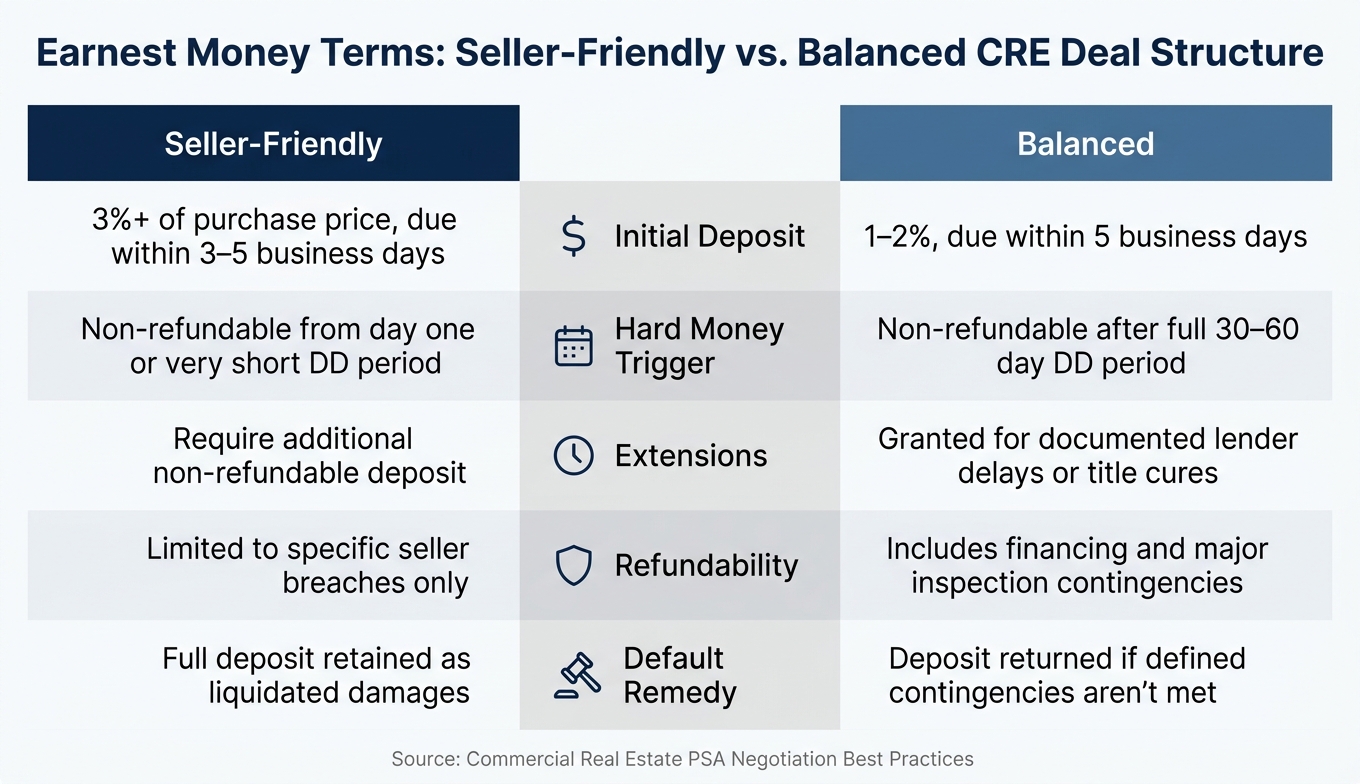

Here's how seller-friendly and balanced terms usually compare:

| Term | Seller-Friendly | Balanced |

|---|---|---|

| Initial Deposit | 3%+ of purchase price, due within 3 to 5 business days | 1–2%, due within 5 business days |

| Hard Money Trigger | Non-refundable from day one or very short DD | Non-refundable after full 30–60 day DD period |

| Extensions | Require additional non-refundable deposit | Granted for documented lender delays or title cures |

| Refundability | Limited to specific seller breaches only | Includes financing and major inspection contingencies |

| Default Remedy | Full deposit retained as liquidated damages | Deposit returned if defined contingencies aren't met |

Use narrow, objective termination rights and clear default language.

Turning the Business Deal Into Clear Contract Language

Once the business terms are set, put them into clear PSA language before anyone signs. The LOI sets the deal at a high level. The PSA has to turn that deal into exact, enforceable terms. If the wording stays loose, you leave space for conflict. And that’s usually where fights begin. Earnest money terms only work the way you expect if the PSA says what you actually negotiated.

Align the LOI, PSA, Escrow Instructions, and Lender Timeline

Take the shorthand from the LOI and spell it out in the PSA. This isn’t just about agreeing on the numbers. It’s about drafting the deal so those numbers and terms hold up on paper.

| LOI Shorthand | What the PSA Must Say |

|---|---|

| "Market standard" deposit | Exact dollar amount and percentage of purchase price [2][3] |

| "Refundable during DD" | Right-to-terminate clause with full refund if written notice is delivered before the Due Diligence Expiration Date |

| "30-day due diligence" | A specific calendar date, or "the date that is 30 days after the Effective Date" |

| "Subject to financing" | Loan amount, rate, and commitment deadline |

| "Non-refundable" | Liquidated damages clause stating the deposit is the seller's sole remedy for buyer default |

| "Closing credit" | Explicit instruction to apply the EMD toward the down payment at closing [2][3] |

Define the Effective Date as the date of the last signature, then run every deadline from that date. That one step can save a lot of confusion later. Financing deadlines should also match the lender’s actual commitment timeline, not some neat round number pulled from the LOI.

Final Negotiation Checklist for Buyers and Sellers

Before the PSA and escrow instructions go out, do one last pass for gaps and mismatches:

- Dollar amount: Does the total deposit, including any added tranches, match the LOI, and is it credited toward the purchase price at closing?

- Deposit deadlines: Are all deadlines tied to the Effective Date? [2][1]

- Contingency end dates: Do the financing, inspection, and title review periods match actual third-party timing?

- Notice procedures: Are the delivery method, recipients, and cutoff time clearly stated? [5][6]

- Escrow holder instructions: Is a neutral third party named, are fees assigned, and do the instructions say how disputed funds will be held until the parties settle the issue? [3]

- Default remedies: Is the deposit clearly labeled as liquidated damages for buyer default, and does the buyer keep the right to specific performance if the seller defaults? [6]

- Interest allocation: Does the PSA say who gets the interest earned on escrowed funds? [6]

Conclusion: The Terms That Matter Most

Earnest money terms don't stand alone. They work as one package, and that's the lens that shapes the rest of the deal. Deposit size, timing, and refundability all tie together. At the center of it all is the same push and pull: buyer flexibility versus seller certainty.

The main rule is alignment. In most deals, the hard deposit should start only after diligence and financing milestones are done. Buyers need enough time to finish their review before the money goes hard. Sellers, on the other hand, need enough certainty to know the buyer is serious.

Once the economics are settled, clear contract language is what turns those negotiated terms into something enforceable. A well-drafted LOI, PSA, and escrow instructions should all line up on deadlines, refund conditions, and the neutral escrow holder. The deal works only when the PSA and escrow instructions match the business terms exactly. If the buyer defaults, the earnest money provision is often the seller's main remedy, so that limit should be stated plainly from the start [1]. When the PSA, escrow instructions, and timing all line up, the deposit does what it's supposed to do: protect both price certainty and closing certainty.

FAQs

How much earnest money is too much?

Earnest money deposits usually fall between 1% and 10% of the purchase price. What counts as too much depends on the market and the type of property.

In hot markets or luxury deals, buyers often put down more to show they’re serious. But once the deposit goes above 10%, many people start to see it as excessive.

Can I get my deposit back after due diligence ends?

Usually, you can get your earnest money deposit back only if your PSA lets you terminate the deal and receive a refund before the due diligence period ends.

Once due diligence is over, that deposit often becomes non-refundable if the transaction keeps moving ahead, unless the contract spells out extra protections. So the short answer is simple: it all comes down to the exact terms in your PSA.

What should the PSA say about escrow disputes?

The PSA should state that a neutral third-party escrow agent will hold the funds until the parties meet their obligations or the dispute is resolved.

It should also spell out when the escrow funds can be released and what happens if the parties disagree. For example, the agreement may call for arbitration or court intervention. That way, the funds are released only as the agreement allows.