Ultimate Guide to CRE Exit Risk Mitigation

In this market, a deal can fail at the exit even if the asset has performed okay. If you want to cut exit risk, I’d focus on four things early: sale value, refinance proceeds, new equity options, and time to maturity.

Right now, the math is tougher. Office exit cap rates have moved from 6.00%–6.75% before COVID to 7.25%–8.50% in 2025. Multifamily leverage has also tightened, with LTVs moving from 70%–80% to 60%–70%. That means lower values, smaller loan proceeds, and more pressure on sponsor equity.

Here’s the short version of what I’d check first:

- Asset risk: Is NOI based on market expenses, taxes, insurance, and reserves?

- Loan risk: Will the property still meet DSCR, LTV, and debt-yield tests at maturity?

- Market risk: Are buyer demand and cap rates still in line with your exit price?

- Downside risk: What happens if NOI drops 10%–20% and cap rates move up 25–100 bps?

- Backup plans: Can you extend, modify, pay down, recap, or sell before maturity becomes a crisis?

- Decision rules: Do you have trigger points at 18–24 months, 12–18 months, and below 95% refi coverage?

How To Use The Three Pillars of Real Estate to Limit Your Downside Risk

sbb-itb-df8a938

Quick Comparison

| Exit risk area | What can go wrong | What I’d watch |

|---|---|---|

| Sale | Buyer pricing comes in below target | Exit cap rate, lease rollover, buyer pool, market-normalized NOI |

| Refinance | New loan doesn’t pay off the old one | DSCR, debt yield, LTV, reserves, rate-cap timing |

| Recap | New equity is too expensive or not available | Dilution, partner demand, sponsor cash need |

| Hold | Asset can’t carry debt and CapEx long enough | Cash flow, covenant headroom, maturity timeline |

The core idea is simple: don’t wait for maturity to tell you the exit no longer works. I’d stress the deal early, rank the weak spots, and choose the exit path that gives you the best shot at protecting equity and cash.

How to Diagnose Exit Vulnerabilities at the Asset, Loan, and Market Level

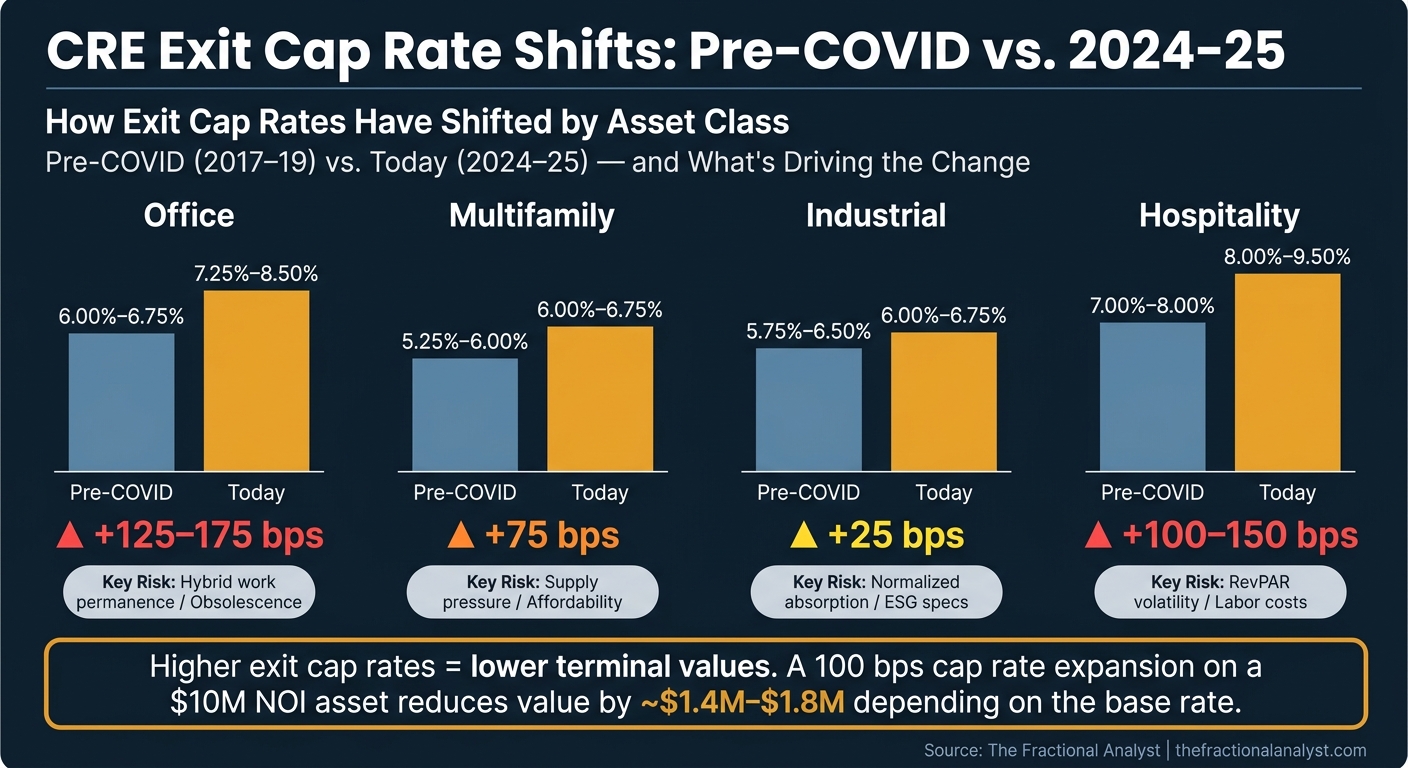

CRE Exit Risk: Cap Rate Shifts by Asset Class (Pre-COVID vs. 2024–25)

Exit risk shows up in three places: the asset, the loan, and the market. Break them apart first. That makes it much easier to see where the problem starts and what to fix first.

Asset-Level Weak Points That Reduce Exit Value

Start with the property’s income stream. Underwrite NOI using market-level expenses, not unusually low operating costs. Buyers and lenders will reset expenses to market norms, underwrite property taxes as if a reassessment happens after the sale, and include reserves when they calculate exit value [1].

That matters because rising insurance, taxes, and payroll eat into NOI and push terminal value down [2]. Lease rollover is another pressure point. If a large chunk of leases expires within 12 to 24 months of exit, buyers usually price in vacancy and re-leasing risk. Office assets face extra pressure from the staying power of hybrid work and softer demand [2]. Industrial assets with clear heights below 32 feet or weak power specs also tend to trade at a discount [2].

Buyers at the institutional level are also paying more attention to energy and sustainability features. If an asset lacks EV charging, efficient systems, or similar features, liquidity can weaken [2]. And these same weak points don’t just hurt a sale. They often show up again in refinance proceeds and covenant tests.

The table below shows how exit cap rates have moved by asset class. That shift changes how buyers price risk right now [2]:

| Asset Class | Pre-COVID Exit Cap (2017–19) | Today's Exit Cap (2024–25) | Key Exit Risk Factor |

|---|---|---|---|

| Office | 6.00%–6.75% | 7.25%–8.50% | Hybrid work permanence / Obsolescence |

| Multifamily | 5.25%–6.00% | 6.00%–6.75% | Supply pressure / Affordability |

| Industrial | 5.75%–6.50% | 6.00%–6.75% | Normalized absorption / ESG specs |

| Hospitality | 7.00%–8.00% | 8.00%–9.50% | RevPAR volatility / Labor costs |

Debt Terms and Covenant Triggers That Increase Maturity Pressure

After the asset review, move to the loan. This is where pressure can turn into default risk. Start with the maturity date and any extension options. Then model whether the deal still qualifies under today’s debt yield, DSCR, LTV, and reserve rules.

Stress-test each one. Debt yield below 8% often reduces refinance proceeds [2]. For office assets, LTV above 60% can point to a higher chance of a refinance shortfall [2]. If reserves have been drained, lenders may require paydowns or hold back proceeds [1].

| Indicator | Low Risk Range | Elevated Risk Range | Impact on Exit |

|---|---|---|---|

| Debt Yield | >10% | <8% | Reduces lender proceeds in a higher-for-longer rate environment [2] |

| LTV (Office) | <60% | >60% | Signals high refinance shortfall risk [2] |

| Reserve Funding | Fully funded | Unfunded / deferred | Reduces buyer interest; lender may withhold proceeds [1] |

Once you’ve worked through the loan math, the next step is simple: check whether the exit still works if NOI slips and cap rates move out.

Scenario Modeling for Base, Downside, and Severe Downside Cases

With the asset and loan pressure points mapped, run scenarios across the exit window. Use three cases:

- Base: flat NOI, current cap rate

- Downside: NOI down 10%, cap rate up 25–50 bps

- Severe downside: NOI down 15%–20%, cap rate up 75–100 bps

Add 5 to 10 bps to the exit cap rate for each remaining hold year to reflect continued rate uncertainty [1].

"Your future cap rate still has to make sense today." - Spencer Vickers, The Fractional Analyst [1]

The number to watch is equity recovery in each case. If the severe downside case shows a refinance shortfall or negative equity at exit, that’s not just a model output. It’s a planning signal. Use that case to rank the move that will matter most: NOI lift, paydown, recap, or sale. From there, you can see whether the deal needs more time, more capital, or a different exit path.

How to Build Refinance and Sale Contingency Plans Before Maturity

Once the downside case is on the table, the next step is simple: build fallback plans before the loan matures. Use current financials, lender feedback, and conservative assumptions so you keep time on your side when talks get tough.

Refinance Options: Extension, Modification, Paydown, and Hedging

Use the severe downside case to decide on the first fallback path. In a tight refinancing market, early lender communication can make a big difference. Borrowers who stay ahead of the issue bring updated financials, explain what's happening before the lender has to ask, and put realistic options in front of the lender early.

| Tool | What it does | Best fit |

|---|---|---|

| Maturity Extension | Pushes the loan maturity out to buy time for a cleaner exit | Loans that need more time before a clean exit |

| Loan Modification | Adjusts terms to better match current performance | Stressed but still performing assets |

| Sponsor Paydown | Uses sponsor equity to reduce the balance and improve leverage | Assets with enough equity to bridge the gap |

| Reserve Use | Applies approved reserves to cover temporary shortfalls or required items | Loans where reserves are available and permitted |

| Rate Cap Renewal | Replaces an expiring cap to keep the hedge matching the loan term | Floating-rate debt with near-term cap expiration |

| Interest Rate Swap | Hedges interest-rate exposure over a longer term | Borrowers seeking more certainty on floating-rate debt |

Two details matter here. Renew any required rate cap early. And after every lender proposal, rerun the covenant tests so you know where the deal stands.

Sale and Recapitalization Paths When Refinance Proceeds Fall Short

If lender options still leave a financing gap, move to a sale or new capital plan. A sale worked out before maturity usually gets better pricing than a forced sale. That's the difference between running a process and getting cornered.

If sale proceeds don't cover the gap, recapitalization can help fill it and keep the asset in play. A structured recap can buy more runway for a property that still has a workable business plan but needs time to operate through the pressure.

If tax deferral is part of the plan, build a 1031 exchange into the exit path early enough to make the timing work.

Operating Moves That Improve Exit Feasibility

Every operating move should push NOI, DSCR, or both in the right direction. Even small shifts matter. A 5% cut in operating expenses or a 5% drop in rental income can materially affect NOI and DSCR [2].

That means the day-to-day moves need to support the exit story:

- Renew leases early before they turn into vacancy risk

- Focus re-tenanting on spaces that hold up the rent roll

- Cut discretionary expenses, but don't delay maintenance that a buyer or lender will flag in due diligence

- Use capex only when the expected lift in NOI is worth the cost

The goal is to show a market-normalized, lender-ready underwriting case. Rebuild reserves before exit, keep capital spending tied to NOI improvement, and make sure each move gives you a cleaner hold, sell, or recap path.

How to Choose the Right Exit Path: Hold, Sell, Reposition, or Recapitalize

Use the severe downside case to pick the exit path you can actually execute: hold, sell, reposition, or recapitalize. The point is to rank each option by execution risk, not by the return you hoped for in the first model. You're looking for the path most likely to protect equity and cash, not the one that keeps the original pro forma alive on paper.

Hold Versus Sell: How to Decide

Hold when DSCR stays above lender minimums and the sponsor can cover debt service and CapEx. Sell when cash flow can't get back to lender minimums before maturity.

If you do sell, make sure NOI is market-normalized. If expenses look unusually low, buyers will underwrite higher costs and cut their price to match [1].

If a hold doesn't work and a sale still doesn't solve the problem, it's time to look at structural fixes.

When Repositioning or a Partial Exit Preserves More Value Than a Full Sale

Repositioning makes sense when the asset is dealing with structural obsolescence, not just a cyclical dip. For office, underwrite to liquidation, land, or conversion value when the income-producing use no longer holds up. In that setting, a targeted repositioning, partial sale, or joint venture recapitalization can preserve more cash and flexibility than a forced full-asset sale [2].

If refinance proceeds come up short, bring in new equity or a partner only when the recapitalization preserves more value than a forced sale.

Exit Path Comparison: Capital Need, Timeline, and Equity Risk

The table below ranks each path by capital demand, timing, and equity risk [2]:

| Exit Path | Capital Needed | Timeline | Risk |

|---|---|---|---|

| Hold | High | Long-term | High (market and rate risk) |

| Sell | Low | Short-term | Low if market is active |

| Reposition | Very high | Medium to long | Very high (execution risk) |

| Recapitalize | Medium | Medium | Moderate (dilution risk) |

No path is risk-free. Once you choose one, set clear trigger points and a reporting cadence around it. Then define the trigger points that would force a pivot.

Governance, Monitoring, and Reporting to Catch Problems Early

Managed exits depend on early detection, not a last-minute scramble. Trigger points only work if a reporting system sits behind them and keeps the team honest.

Portfolio-Level Triggers and Reporting Cadence

Start with a live maturity ladder. Think of it as the control center for exit risk across the portfolio. It should track each property’s loan terms, maturity date, leverage, covenants, hedges, sponsor recourse, lender status, projected balance, projected DSCR, and refinance gap in one live view. In volatile markets, update it every month. Any loan with 18–24 months to maturity should already have a preliminary exit review. Loans inside 12–18 months need a formal backup plan in place.

That dashboard should also show risk status at a glance:

- Green: refi coverage above 110%

- Yellow: 95%–110% or a falling DSCR

- Red: below 95% or a likely covenant breach

Once an asset turns yellow, lender talks and paydown planning should begin right away, not after it slips into red. In most cases, covenant breaches don’t come out of nowhere. They’re usually preceded by two to six quarters of visible weakening, which often gives the team time to act.

Flag the asset when base-case DSCR drops below 1.20x. Launch an extend-versus-sell review within 60 days if it falls to 1.10x. Start paydown planning and lender outreach when modeled refinance proceeds drop below 95% of payoff [3][4]. The dashboard should guide the call on whether to hold, negotiate, sell, or recapitalize. When these thresholds are written down ahead of time, with named owners and due dates, escalation becomes automatic instead of optional.

Monthly asset-level reports should cover NOI trends, occupancy, leasing pipeline, reserve balances, and the main covenant metrics. Quarterly portfolio reviews should go to the investment committee and sum up covenant headroom, valuation watchlists, refi coverage ratios, and maturity concentrations. Each quarterly review should answer one plain question:

If this loan matured in 12 months, what are our realistic exit paths and where are the gaps?

How The Fractional Analyst and CoreCast Support Exit Risk Management

These workflows are much easier to keep up when the models and reports follow the same format. The Fractional Analyst supports underwriting, scenario modeling, maturity mapping, market research, and lender reporting. CoreCast adds standardized models, live dashboards, and what-if analysis across rates, cap rates, and NOI. It also tracks scenario history over time, so decision-makers can see how projections changed and what set off earlier actions.

FAQs

How early should I start planning for exit risk?

Start planning for exit risk as early as possible. Doing that early helps line up your investment with your goals, while cutting costs and limiting possible exposure.

It also gives you time to map loan maturity timelines, spot weak points before they turn into bigger problems, and use scenario projections to see how market conditions could affect returns and backup plans.

What is the biggest warning sign of a refinance shortfall?

The biggest warning sign is a drop in property value. That can shrink your financing choices and make it tougher to qualify for a new loan under current underwriting standards.

Other red flags include:

- falling revenue

- high debt

- limited cash reserves

- declining occupancy

- delayed financial reporting

- loans above supervisory loan-to-value limits

When is a recap better than a sale?

A recapitalization can make more sense than an outright sale when the market is shaky or pricing is all over the place. If conditions are weak, selling may force you to take a lower price than the asset is worth. In that case, a recap lets you pull out trapped equity while still keeping control of the property.

It can also help if you need to rework the capital stack. That might mean refinancing debt, bringing in or swapping out partners, or dealing with loans that are coming due. Instead of rushing into a sale at a suboptimal price, you can use a recap to buy time and hold the asset until the market improves.