Ultimate Guide to Tax Treatment: Equity vs. Debt

Debt can cut taxable income. Equity cannot. That one rule drives much of the tax gap in a commercial real estate deal.

If I had to boil this guide down, I’d put it this way:

- Debt interest is often deductible, but Section 163(j) can cap that deduction at 30% of adjusted taxable income

- Equity distributions are not deductible

- Principal payments are not income to the lender and not deductible to the borrower

- Equity payouts can be return of capital, capital gain, or ordinary income, depending on basis and deal terms

- Pass-through entities usually avoid the double tax that hits C corporations

- Below-market related-party loans can trigger imputed interest

- If a “loan” looks like equity, the IRS can reclassify it and deny interest deductions

That means you can’t stop at labels. A note with no paid interest, no enforcement, and repayment tied to deal success may be treated like equity even if the paperwork says “loan.”

Tax Implications of Corporate Debt and Equity Financing

sbb-itb-df8a938

Quick Comparison

| Issue | Debt | Equity |

|---|---|---|

| Tax deduction at entity level | Interest often deductible | No deduction for distributions |

| Cash repayment | Fixed payment duty | Depends on cash flow or sale |

| Investor tax treatment | Interest usually taxed as ordinary income | Can be return of capital, gain, or ordinary income |

| Basis effect | Lender basis tied to note | Owner basis changes with contributions, income, losses, and distributions |

| IRS risk | Reclassification if terms or conduct look weak | Lower unless it mimics debt |

| Common trouble spots | Thin capitalization, missed payments, no enforcement | Poorly drafted preferred return or disguised loan terms |

One more point matters here: after 2021, the 163(j) cap uses EBIT, not EBITDA. In depreciation-heavy CRE deals, that can shrink current interest deductions more than many sponsors expect.

I’ll keep the rest of this simple: the tax result turns on deductions, basis, entity type, AFR pricing, and whether the parties act like lender and borrower in practice - not just on paper.

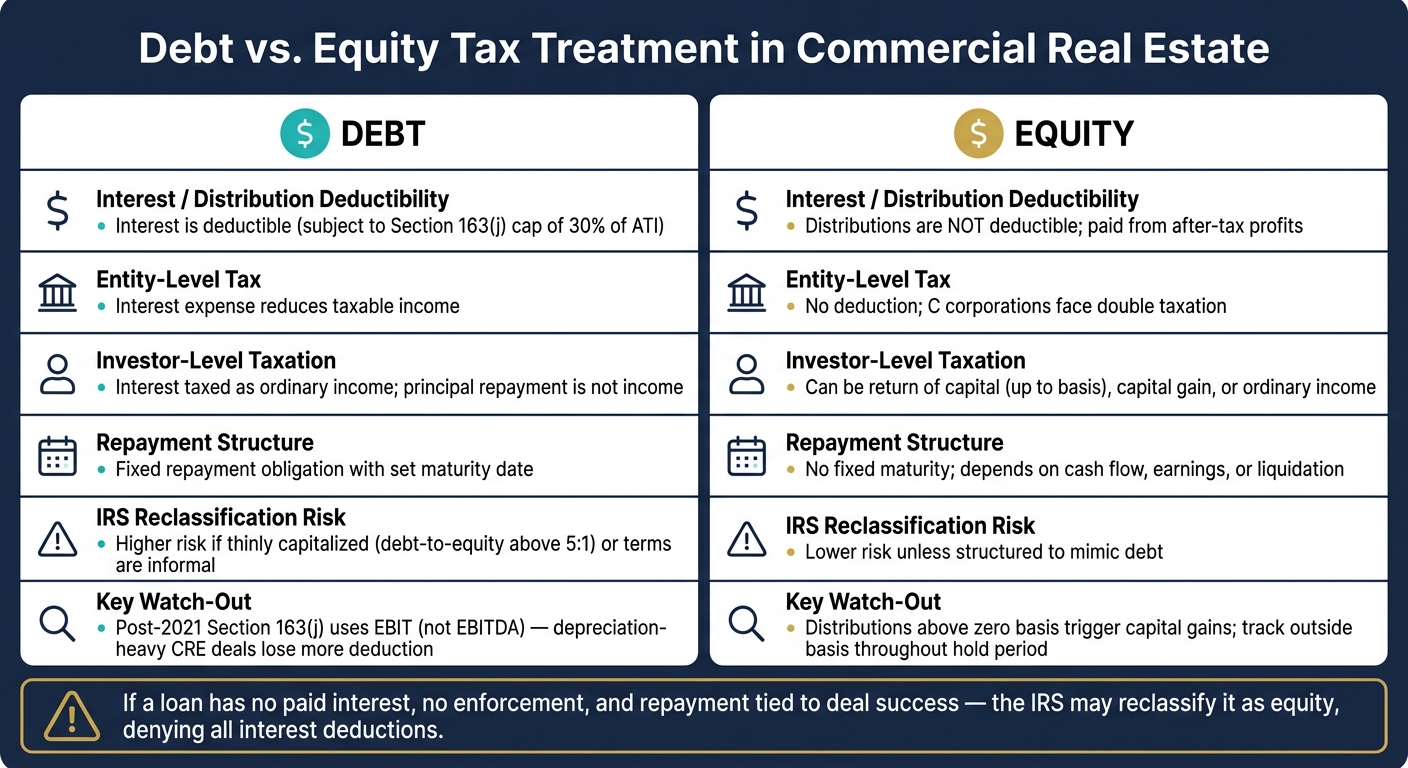

Debt vs. Equity Tax Treatment: Core Differences

Debt vs. Equity Tax Treatment in Commercial Real Estate

In a CRE capital stack, debt is a fixed repayment duty. Equity is ownership. And when the IRS reviews an arrangement, it doesn’t stop at whatever label the documents use. It looks at the economic reality of the deal.

The IRS uses an all-facts-and-circumstances test. It looks at points like whether there’s a fixed maturity date, whether repayment turns on performance, and whether the holder has governance rights. No single factor controls the outcome.

Those facts show up most clearly in the tax results below.

For sponsors, this is where things get very practical. These rules shape whether cash flow is sheltered by deductions or taxed before it ever gets distributed.

| Feature | Debt | Equity |

|---|---|---|

| Interest Deductibility | Deductible, subject to Section 163(j) | Not deductible; distributions are made from after-tax profits |

| Entity-Level Taxation | Interest expense reduces taxable income | No deduction; double taxation for C corporations |

| Investor-Level Taxation | Interest is ordinary income; principal is not income | Distributions may be taxed as ordinary income, capital gains, or a return of capital |

| Repayment Treatment | Fixed repayment obligation | No fixed maturity; repayment depends on earnings or liquidation |

| Priority in Capital Stack | Senior or mezzanine financing; ahead of equity | Residual interest; paid after debt obligations are satisfied |

| Reclassification Risk | Higher if the arrangement is thinly capitalized or lacks formal loan terms | Lower, unless structured to mimic debt |

The two biggest tax effects are deduction treatment and investor-level taxation.

How Debt Affects Taxable Income

Debt can reduce taxable income because interest is generally deductible, though Section 163(j) may limit that deduction. That’s a major point for sponsors trying to manage tax drag.

Principal works differently. Principal repayments are not deductible, and the lender generally does not recognize income on repayment of principal.

How Equity Returns Are Taxed

Equity follows ownership, not a fixed promise to repay. That changes the tax picture.

For C corporations, taxable earnings can be taxed at the entity level and then taxed again when distributed. For pass-throughs, the result depends on the owner’s basis and the entity’s earnings.

Distributions up to basis are generally a return of capital. Amounts above basis are generally taxable gain.

Interest Deductibility, Limitations, and Imputed Interest Rules

Even if a deal is set up as debt, the tax upside only holds if the instrument is treated as debt for tax purposes and the interest stays deductible.

When Interest Is Deductible and When It Is Limited

Interest deductions are one of the biggest tax upsides of debt. But there’s a catch: the debt has to be respected, and the pricing has to hold up. If the IRS reclassifies the instrument as equity, the interest deduction is gone. And even when the debt is respected, Section 163(j) limits business interest expense to 30% of adjusted taxable income (ATI) [2].

For tax years beginning after 2021, ATI is based on EBIT, not EBITDA. That means depreciation and amortization no longer increase the interest cap. In plain English, depreciation-heavy CRE deals can lose more of the deduction than sponsors may expect [2].

Below-Market Loans and Imputed Interest

Related-party loans get extra IRS attention. If the interest rate is below the Applicable Federal Rate (AFR), the IRS imputes interest. In that case, the lender is treated as receiving interest income, and the borrower is treated as paying interest [4]. The IRS updates the AFR each month. As of April 2026, the mid-term rate for loans with terms of 3 to 9 years was 3.75% [3][5].

Allen v. Commissioner (T.C. Memo 2023-86) shows the risk: notes with stated maturity dates were reclassified as equity because repayment depended on business success, no interest was paid, and the lenders did not enforce default [4].

The practical takeaway is pretty simple:

- Price loans at or above the AFR

- Pay cash interest

- Enforce repayment the way an outside lender would

Once those debt limits are clear, the next issue is how equity contributions and distributions are taxed at the entity level.

Equity Contributions, Distributions, and Entity-Level Tax Consequences

Equity follows a different tax path. It affects basis, distributions, and entity-level tax. That matters because equity changes both the investor's basis and the way the entity reports tax items.

Capital Contributions and Return of Capital

When an investor puts equity into a deal, that contribution increases their tax basis. In partnerships, the capital account changes too. Unlike debt, equity does not give the entity a deduction.

When capital is paid back, those distributions are treated as a return of capital to the extent the investor still has basis. In most cases, that means the distribution is not taxable. But once basis drops to zero, any extra distributions are usually treated as capital gains. That's why tracking outside basis matters during the full hold period, not just when the property sells [1].

There's another wrinkle here. Depreciation can push taxable income down while cash distributions keep going out. So an investor can show tax losses even when the deal is throwing off positive cash flow.

Pass-Through Entities vs. C Corporations

The entity type plays a big role in how much of the tax upside actually reaches investors. Partnerships and LLCs taxed as partnerships pass income, losses, and deductions straight through to owners. The entity itself does not pay federal income tax. Partners may also include their share of partnership debt in basis, which can help support loss deductions, subject to basis, at-risk, and passive activity limits [6]. That's why the exact same project can land very differently on two investors' tax returns.

C corporations work differently. They pay tax at the entity level, and then shareholders pay tax again when dividends are distributed. That double layer creates a clear after-tax drag. It's a big reason partnerships and LLCs are still the main choice in commercial real estate.

"Partnerships provide the most flexibility in terms of profit and loss allocation and even allow including partnership liabilities in your tax basis." - Steven Barranca and Gregory Booth, EisnerAmper

C corporation blockers show up most often when tax-exempt investors are involved. Those investors may prefer a blocker or lower leverage because they can't use the interest tax shields that make leverage appealing [1].

| Feature | C Corporation | Partnership / LLC |

|---|---|---|

| Entity-Level Tax | Yes | No |

| Double Taxation | Yes | No |

| Basis from entity debt | No | Yes |

| Special Allocations | No | Yes |

Even if equity is respected for tax purposes, sloppy capital terms can still lead to debt reclassification. In plain English, these tax results only work if the structure continues to be treated as equity, not disguised debt.

When Debt Gets Reclassified as Equity and How to Reduce That Risk

A CRE loan can look solid on paper and still lose debt treatment if the IRS or a court decides the economics look more like an equity investment. That’s the core issue here: what facts make a loan fail the debt test?

Common Factors the IRS Reviews

Courts often use the 13-factor Estate of Mixon analysis, and no single factor decides the case. Usually, the result turns on a group of facts viewed together.

The table below shows the main factors the IRS reviews and what tends to support debt treatment versus equity treatment:

| Factor | Debt-Like | Equity-Like |

|---|---|---|

| Written instrument | Formal promissory note | Oral agreement or informal advance |

| Maturity date | Fixed, certain date | No date, perpetual, or tied to project success |

| Interest rate | Fixed, market-based rate | No interest, or contingent on profits |

| Enforcement rights | Right to sue, foreclose, or demand payment | No collection efforts; defaults ignored |

| Repayment history | Consistent, timely principal and interest payments | Sporadic payments or none at all |

| Collateral | Secured by assets or equity pledges | Unsecured |

| Subordination | Senior or equal to other creditors | Subordinated to all general creditors |

| Books and records | Reported as debt on all returns and ledgers | Inconsistent or missing treatment |

These are the facts sponsors need to control - not just in the loan file, but in how the deal is handled day to day.

Insider loans and thinly capitalized deals get the most attention. Courts often treat a debt-to-equity ratio above 5:1 as a thin-capitalization concern [4]. In Allen v. Commissioner (T.C. Memo 2023-86), the Tax Court reclassified the advances as equity because repayment depended on future sales and no interest was actually paid [4].

"A debtor's failure to repay on the due date, or to seek a postponement, is arguably the most significant factor in the debt-equity analysis." - U.S. Tax Court (cited in Allen v. Commissioner) [4]

That quote gets right to the point. If the borrower misses the due date and no one acts like that matters, the “loan” starts to look like money left in the deal at the owner’s risk.

Structuring Steps for Commercial Real Estate Capital Raises

Paper alone won’t save a weak structure. The parties also have to act like lender and borrower in real life. In Gray v. Commissioner (T.C. Memo. 1997-67), the Tax Court reclassified more than $1.8 million in claimed loans as taxable dividends even though written promissory notes existed. The court focused on the lack of collateral, the corporation’s failure to demand repayment on overdue amounts, and the fact that only a small share of principal was ever repaid [7].

Put simply, related parties need to behave the way unrelated parties would.

A few practical steps can lower reclassification risk:

- Use signed promissory notes

- Set fixed maturity dates

- Charge market-rate interest

- Secure the loan where practical

- Enforce missed payments - if a payment is missed, formally amend the loan documents and record the change in the entity’s records

- Keep debt terms separate from ownership percentages - avoid matching debt balances to ownership stakes, since that pattern is a common IRS trigger [7]

Conclusion: Key Tax Differences Sponsors Should Keep in View

Debt treatment depends on both documentation and conduct throughout the hold period.

FAQs

How do I know if the IRS will treat a loan as debt or equity?

The IRS doesn't rely on one bright-line rule to decide whether an instrument is debt or equity. Instead, it uses a facts-and-circumstances analysis.

Courts usually look at a handful of practical signals. They often ask whether there's a written, unconditional promise to repay a set amount on a fixed maturity date, whether the instrument carries a fixed interest rate, whether the borrower could have gotten financing from a third party, and what the parties meant the arrangement to be.

On the other side, some facts can make an instrument look more like equity. Common signs include thin capitalization, subordination, or repayment that depends on how well the venture performs.

What happens if Section 163(j) limits my interest deduction?

If Section 163(j) limits your interest deduction, the amount over the cap - usually 30% of adjusted taxable income (ATI) - carries forward with no end date into future tax years. So you don't lose the deduction. You just can't claim it for the current year.

Real estate businesses can opt out by making an irrevocable election to be treated as an electing real property trade or business. But there's a trade-off: you must use the Alternative Depreciation System (ADS) and give up bonus depreciation.

How do basis rules affect equity distributions and taxes?

Basis rules decide how much loss a partner can deduct and when a distribution becomes taxable.

A partner’s tax basis usually sets the ceiling on deductible losses. If losses go past that amount, the extra loss is usually suspended until the partner’s basis goes up.

Distributions are usually tax-free up to the partner’s basis. But there’s a catch: if a distribution is more than basis, or if debt is shifted away from a partner, that can trigger a taxable event. In real estate partnerships, a partner’s share of entity debt can increase basis.