Best Practices for Maximizing Mezzanine Returns

Mezzanine returns are set by structure first, rate second. If I want better mezz returns, I focus on entry leverage, intercreditor rights, covenant control, cash-pay vs. PIK mix, and the exit plan before I focus on the headline coupon.

Here’s the short version:

- I underwrite for a 15%–25% value drop

- I test exit rates +200 bps

- I watch refinance risk closely, especially with $875 billion of commercial mortgages maturing in 2026

- I match pricing to the spot in the stack, not to sponsor wish lists

- I use fees, PIK, and extension terms carefully because they can change IRR more than the stated rate

- I push for strong cure rights, buyout rights, cash sweeps, and reserve controls

- I make sure the loan term fits the actual business plan, with time for delays

- I tailor structure to the asset and the sponsor

- I keep servicing tight after closing, because paper rights mean little if no one tracks them

A simple example shows why this matters. In a $50,000,000 value-add multifamily deal, adding a $7,500,000 mezz piece on top of a $32,500,000 senior loan lifted projected 5-year equity IRR from about 15% to 24%. That upside is the draw. But the same leverage can hurt fast if value, lease-up, or refinance timing slips.

Quick comparison

| Area | What I focus on | Why it matters |

|---|---|---|

| Underwriting | Stress value, timing, rates, and takeout | Tests whether principal can get out cleanly |

| Pricing | Match return target to attachment point and asset risk | Stops thin pricing on thin equity cushions |

| Interest structure | Balance cash-pay, PIK, and fees | Changes current yield, exit pressure, and IRR |

| Upside | Add kickers only when base economics fall short | Adds return, but only if the deal performs |

| Intercreditor rights | Cure rights, buyout rights, standstill limits | Drives control in a senior workout |

| Covenants | Cash sweeps, reserve triggers, distribution limits | Helps stop cash leakage before default |

| Business plan | Use lower occupancy and slower lease-up | Filters out weak exit assumptions |

| Term | Add buffer beyond stabilization | Lowers maturity pressure |

| Asset/sponsor fit | Match structure to cash flow and sponsor depth | Keeps payment burden in line with deal risk |

| Servicing | Track notices, covenants, and PIK balance | Protects return after closing |

If I had to reduce the whole article to one line, it would be this: mezzanine returns come from pricing risk well, controlling downside, and giving the loan enough time and rights to get repaid.

Mezzanine Debt Pricing Explained

sbb-itb-df8a938

Why Mezzanine Returns Are Won or Lost in Structure

Mezzanine returns are set before closing, not after. The coupon matters, sure. But it doesn't drive returns on its own.

What moves the needle is the structure of the deal: leverage limits, loan documents, covenants, and the remedies a lender can use if performance slips. The next sections break those levers into specific actions.

Take a simple case. Two lenders can both quote 14%. The lender with tighter intercreditor rights, an Article 9 equity pledge, and stronger covenants will usually end up with better risk-adjusted returns. Structure is the edge, not just a higher coupon.

When a deal starts to weaken, recovery speed becomes part of the return story. In other words, downside speed matters as much as coupon. A mezzanine lender with a UCC Article 9 pledge on the equity interests can typically foreclose in 30–60 days, versus 9–18 months for judicial real estate foreclosure [4]. In a downside case, that faster path can preserve more value and improve recovery.

Fees, PIK interest, and minimum-interest protections often move lender IRR more than the headline rate [1][9]. And the attachment point should be set based on downside tolerance, not sponsor appetite. That's the line between a disciplined lender and one that's just buying yield.

Those economics set the baseline for the best practices that follow.

1. Use Institutional-Grade Underwriting and Monitoring Tools

Institutional-grade underwriting starts with one thing: downside modeling before you price the deal.

That means starting with the attachment point and then putting the deal under pressure. Stress-test a 15%–25% drop in stabilized value, a 90-day to 12-month lease-up delay, and an exit refinance at 200 basis points above prevailing rates [5][10][8]. This matters even more now. About $875 billion in commercial mortgages will mature in 2026, so refinance risk is a major issue in mezzanine underwriting [5].

But stress inputs on their own don't tell you much. They need to run through a full return model.

Model the entire return stack, including PIK accrual, exit fees, and compounding, because each one can change realized IRR in a big way [9]. The strongest mezzanine returns don't come from looking at the coupon alone. They come from seeing how every cash flow works together. And once the deal is underwritten, that same level of discipline needs to carry into servicing and compliance tracking.

On the monitoring side, the job shifts from pricing risk to watching it closely. Your servicing process should track covenant breaches, notice-plus-cure periods, and intercreditor notice obligations in real time [5]. If that sounds like back-office detail, it isn't. It's the stuff that can decide whether a problem stays small or turns into a mess.

These are the core assumptions institutional lenders stress in mezzanine underwriting:

| Stress Variable | Institutional Threshold |

|---|---|

| Value Decline | 15%–25% reduction in stabilized value [5] |

| Exit Cap Rate | 10%–15% expansion from base case [10] |

| Refinance LTV | 10–15 points below base-case projection [5] |

| Interest Rates at Exit | +200 bps over prevailing rates [8] |

| Lease-up Timing | 90-day to 12-month stabilization delay [10][5] |

Better tools help on both sides of the process: downside protection and execution speed. Modern underwriting platforms can shrink multi-scenario capital stack analysis from weeks to minutes [7]. That faster read helps with pricing up front, while active monitoring helps protect the return after closing.

2. Align Return Targets With Capital Stack Risk

Start with the attachment point and detachment point. That’s where pricing usually gets honest.

A mezzanine lender that sits behind a 65% senior loan and tops out at 80% LTC has more equity beneath it than a lender stretching to 85%–90% LTC. That extra cushion matters. With a tighter basis, pricing can often land around 11%–12% current-pay. When that cushion gets thinner, lenders usually want 13%–15%, often with PIK layered in [4].

Sponsor quality matters too. Stronger sponsors can support pricing that is 50–100 bps tighter [4]. That makes sense. If the sponsor has a solid track record, more liquidity, and a history of dealing with rough patches well, the lender may not need as much spread to get comfortable.

Target returns also shift by asset class and risk profile [4]:

| Asset Class | Typical Current-Pay Rate | Total Target IRR |

|---|---|---|

| Multifamily | 11%–13% | 13%–15% |

| Industrial | 11.5%–13.5% | 13.5%–16% |

| Office | 12%–14% | 14%–17% |

| Hotel | 12%–15% | 15%–18% |

| Data Center | 10.5%–13% | 12.5%–15% |

Exit timing can change the math in a hurry. A strong coupon on paper doesn’t always lead to target returns if the loan matures at the wrong moment and the borrower has to refinance into a weak market. Co-terminus maturity can make that problem worse. If the senior lender won’t extend, the mezzanine lender can get pushed into a refinance corner even when the asset itself is doing fine, and that hits realized IRR directly [3].

3. Optimize the Cash-Pay, PIK, and Fee Mix

After you price the risk, the next step is structuring how the return gets paid.

The lender’s return comes from the mix of cash-pay interest, PIK, fees, and participation rights. It does not come from the stated coupon alone. A heavier cash-pay mix improves current yield. A heavier PIK or fee mix can push IRR higher, but it delays when that money is paid.

Cash-pay gives the lender income right away, which sounds good on paper. But it also creates a fixed payment burden for the borrower. In a transitional or construction deal, required cash-pay can squeeze liquidity even when the property is performing as planned. [5][3]

PIK works the other way. It protects near-term cash flow because the borrower doesn’t have to pay that interest in cash right away. But there’s no free lunch here. PIK compounds over time, and as that interest accrues and gets added to the balance, the payoff amount gets bigger. That larger balance then has to be refinanced or paid off at exit. [1][3]

Here’s how each piece tends to affect the deal:

| Component | Impact on Cash Flow | Return Effect | Primary Risk |

|---|---|---|---|

| Cash-Pay Interest | High (Immediate Outflow) | Moderate/Stable | Default if DSCR falls |

| PIK Interest | Low (Deferred) | High (Compounding) | Refinance/Exit pressure |

| Upfront Fee (OID) | Moderate (Reduced Proceeds) | High (Front-loaded) | Higher effective cost |

| Exit Fee | Low (Paid at Exit) | Moderate (Back-loaded) | Depends on sufficient value at exit |

Origination fees and exit fees can lift realized yield without increasing monthly debt service. [9]

A PIK toggle gives the borrower the option to switch between cash-pay and accrued interest when certain triggers are met. [9] That can make the deal harder to execute and monitor, but it also gives both sides more room to work through changing conditions.

The main point is simple: model total exit proceeds, not just the coupon. PIK compounding and back-end fees can turn a deal that looks cheap at first glance into one that is far more expensive by maturity. [9][3] And if the deal has room for it, equity kickers can add upside beyond the coupon.

4. Add Equity Kickers to Capture Upside

When coupon, PIK, and fees still don’t get you to the target IRR, equity kickers can close the gap. They give the lender a share of the residual value at exit after senior debt is paid back. [8][9][1]

Put simply: use equity kickers when coupon and fees still leave an IRR shortfall.

Common kicker structures include warrants, profit participation, and conversion rights. Each one lines up with a different exit profile. Warrants tend to fit deals driven by price appreciation. Profit participation makes more sense for transitional assets with uneven cash flow. Conversion features show up in hybrid structures where the lender might move into a permanent equity stake. [9] But that upside doesn’t happen by magic. You need to model the strike, coverage, and exit math from day one.

There’s a catch here. Kickers do not help on the downside. They only pay when the deal goes well. If a 15%–25% drop in value wipes out the common equity layer, the kicker is worth zero, and the job becomes recovering principal. [5]

That’s why warrant coverage, strike prices, implied dilution, and exit timing need to be modeled directly, not treated like a loose promise of upside. A one-year delay in exit timing can move IRR more than the coupon. [9]

A good model should test:

- Low, base, and high exit cases

- Implied dilution

- Strike price and target ownership written into the term sheet [9]

5. Negotiate Strong Intercreditor Rights

Intercreditor rights decide whether your mezzanine return survives a senior loan workout. If the Intercreditor Agreement (ICA) is weak, the senior lender can foreclose and wipe out your control and recovery position altogether [14].

The main terms to focus on are cure rights, purchase options, standstill periods, and amendment controls.

Cure rights give you a chance to cover missed payments and stop a senior foreclosure. A good target is a 30–60 day window, since many ICAs cap cures at three back-to-back monthly defaults [5][14].

Purchase options matter just as much. If the senior lender begins enforcement, this right lets you buy the senior loan at par plus accrued interest and fees [14]. In plain English, that means you can take the senior lender’s spot and run the workout yourself.

Standstill periods usually block mezzanine foreclosure for 90 to 180 days [12]. Shorter is better. You should also bar principal increases or rate hikes unless you approve them [14]. Otherwise, the senior lender can change the deal while you’re stuck on the sidelines.

One practical point: a full ICA between separate senior and mezzanine lenders often adds 15–30 days to closing [4]. That extra time can feel annoying, but it’s often where the fight over control gets settled.

| Intercreditor Provision | Typical Market Standard | Key Risk Mitigated |

|---|---|---|

| Cash Cure Rights | 3–4 consecutive periods; 5–10 days notice | Senior loan acceleration / foreclosure |

| Standstill Period | 90–180 days | Premature equity foreclosure friction |

| Purchase Option | Par + accrued interest + protective advances | Loss of control during senior enforcement |

| Transfer Rights | Pre-approved "Qualified Transferees" | Due-on-sale / change-of-control defaults |

| Senior Amendments | Prohibited for principal / rate increases | Dilution of mezzanine collateral value |

These rights have more bite when covenants and reserve tests help keep the borrower out of default to begin with.

6. Tighten Covenants, Reserves, and Distribution Controls

Covenants, reserves, and distribution controls can keep a deal out of workout.

DSCR and debt yield covenants help flag stress early. If coverage ratios drop below a set threshold, a well-built deal should trigger a cash sweep, sending operating cash flow to debt service or reserves before a missed payment happens [10]. The key is to tie that sweep to funded interest, tax, and capex reserves, so cash gets trapped before liquidity starts to crack. Then, pair the sweep with reserve funding to protect liquidity before distributions turn back on.

Cure periods matter too. A 30- to 60-day cure period gives people room to fix a delay. A 10-day cure period, by contrast, can turn a minor issue into a technical default even when property performance is still fine.

The same idea carries over to distribution controls. Holding back distributions until the deal reaches a set debt yield or DSCR target helps protect current yield. But those thresholds need to be based on a conservative operating case, not a rosy lease-up forecast [1].

It also helps to use springing subordination. That keeps normal payments in place until there’s an actual default or a senior covenant breach. Add PIK optionality during construction and early stabilization, and the deal can preserve operating cash while still keeping downside protection in place [5].

| Provision | Protective Structure | Risk of Getting It Wrong |

|---|---|---|

| Cure Periods | 30–60 days, notice-plus-cure | 10-day triggers create technical defaults unrelated to property performance |

| Cash Sweep | Triggered by DSCR or debt yield thresholds | Loose triggers allow cash leakage during underperformance |

| Reserve Funding | Interest, tax, and capex reserves funded at sweep | Missing reserve buckets leaves liquidity gaps before distributions resume |

| Distribution Controls | Restricted until debt yield/DSCR targets are met | Early distributions leave the project undercapitalized |

| PIK Toggle | Optional accrual during stabilization | Hard cash-pay creates liquidity strain during lease-up |

| Removal Rights | Limited to material payment defaults or fraud | Technical breaches can trigger premature GP removal |

The point is simple: protect cash flow without pushing the deal into avoidable default. These controls do their job only when the business plan can hold up under stress.

7. Underwrite Conservative Business Plans and Stress Cases

After covenants, the next test is simple: can the business plan hold up if the exit goes sideways? That’s the point of stress testing. A mezzanine loan only works if the deal can still get out cleanly when things get rough.

Start by pressuring the plan itself. Model a 200 bps rate shock and a 10%–15% cost overrun. If the deal depends on a bridge-to-perm exit, model year-3 agency or CMBS takeout proceeds and make sure the mezzanine piece gets taken out in full. If that refinance doesn’t work on paper, the structure needs to change.

You should also assume lease-up drags out longer than the sponsor expects. A good rule: push lease-up back by 6 to 9 months. And for deals above $10 million, underwrite to 88%–92% stabilized occupancy, not 95%.

Run these stress cases on every deal:

| Underwriting Variable | Conservative Stress Assumption |

|---|---|

| Occupancy | 88%–92% (vs. 95% pro forma) |

| Lease-up Pace | 6–9 months longer than projected |

| Construction Cost | 10%–15% over budget |

| Exit Cap Rate | 200 basis points higher than base case |

| Refinance Rate | 200 basis points above current prevailing rates |

| Asset Value | 15%–25% decline from stabilized projection |

The equity layer has to be thick enough to take a 15% to 25% drop in value before the mezzanine position gets hit [5]. If the common equity can’t handle that kind of loss, senior lenders probably won’t grant extensions [5]. And if the exit gets delayed, the loan term and any extension rights need enough room to carry that delay.

8. Match Loan Term and Extension Options to the Exit Timeline

After you stress-test the deal, line up the loan maturity with the actual exit window. This is the timing lever that protects the structure built in Sections 5–7. If a transitional asset needs 24 months to stabilize, the mezzanine loan should include a 6- to 12-month buffer beyond that period. That extra runway gives the sponsor time to finish the plan and refinance or sell without getting pushed into a distressed transaction.

One common trap is co-terminus maturity. Mezzanine loans often mature at the same time as the senior loan. If the senior lender refuses to extend, the mezzanine lender usually can't extend by itself, no matter how well the asset is doing [3]. The way around that is simple in theory, but not always easy in practice: negotiate mezzanine extension rights that run co-terminus with, or a bit longer than, the senior loan's extension options [3].

Extension terms matter just as much as day-one maturity. Debt yield tests, DSCR hurdles, and no-default certifications can all make sense. But they need to be set against a conservative operating case, not the sponsor's best lease-up story [1]. In a high-rate market, an aggressive debt yield test can trigger a technical default even when the project is still sound [1]. For transitional deals, model projected agency or CMBS takeout proceeds in year 3 to make sure the mezzanine piece can be paid off [15].

The exit plan has to drive the maturity profile. A one-year delay in payoff can hurt realized IRR more than a small shift in coupon. And PIK can make that pain worse, because unpaid interest keeps compounding into the final payoff amount. Run that compounding through the full term in your model [1].

| Mezzanine Use Case | Typical Term | Extension Conditions |

|---|---|---|

| Transitional/Value-Add | 2–5 years | Debt yield tests, lease-up milestones, extension fees [1][2] |

| Stabilized/Core | 5–10 years | Co-terminus with senior, no-default certifications [2] |

| Construction Bridge | 2–3 years | Completion guarantees, certificate of occupancy hurdles [13][2] |

| Maturity Recap | 3–7 years | Minimum DSCR hurdles, cash flow sweeps [2] |

Term should also reflect asset type and sponsor quality.

9. Tailor Mezzanine Structure to Asset Type and Sponsor Quality

Once the term lines up with the exit timeline, the next step is structure. And this is where mezzanine deals start to split apart fast. A mezzanine loan on a stabilized industrial asset should not be built the same way as one on a ground-up development.

The biggest line between asset types is cash flow predictability. If the property throws off stable cash flow, a current-pay structure can work. If cash flow is uneven, thin, or missing during lease-up or stabilization, the deal usually needs more PIK or accrual. Ground-up development is the clearest case. There’s no current cash flow during construction, so accrual- or PIK-heavy structures are the standard approach. And for agency-financed multifamily, agency execution often blocks mezzanine debt, which makes preferred equity the cleaner option [4][8][3].

Sponsor quality matters just as much as the asset. A sponsor with a strong track record will often get more room on leverage, standard bad-boy carveouts, and lighter reporting. A newer sponsor, or one doing its first deal, usually gets the reverse:

- Lower advance rates

- Tighter upfront reserves

- Stricter cash sweep triggers

- More frequent financial reporting

Here’s a quick look at how this tends to play out across common asset and sponsor pairings [4][8][3]:

| Asset Type | Sponsor Profile | Combined LTC | Key Structure |

|---|---|---|---|

| Stabilized Multifamily | Institutional | 75%–80% | Preferred equity (agency lenders often exclude mezzanine) |

| Value-Add Multifamily | Middle-Market | 80%–85% | Current-pay interest with senior bridge debt |

| Office (Lease-up) | Institutional | 70%–75% | Heavy PIK; strict debt yield covenants |

| Hospitality | Institutional | 70%–80% | Seasonal cash reserves; FF&E reserves |

| Ground-up Development | Institutional | 80%–85% | Full accrual/PIK; no current-pay during build |

Features like PIK and equity kickers can make sense, but only when both the asset and the sponsor can carry that kind of structure. On paper, protections may look fine. In practice, they only matter if they hold up when property performance shifts.

10. Manage the Investment Through Active Servicing

Once the loan closes, servicing is what keeps the deal structure in place. It protects the covenants, cure rights, and extension options negotiated at the start. If that work slips, those protections can lose force fast.

Keep a close eye on DSCR, debt yield, lease-up pace, and senior loan notices. When a breach shows up, early action matters. It protects cure rights and helps prevent value loss. But that only works if the servicer catches the issue in time to act. This is where covenant design, intercreditor rights, and exit timing either support the return model or start to crack.

PIK accrual needs the same kind of attention. It adds to the payoff balance and can push takeout debt past the refinance limit. So track PIK in real time and make sure the final payoff still fits the planned takeout.

Active servicing also helps when the exit gets delayed. Pair it with extension tests tied to realistic stabilization milestones, and you give the loan more room to protect yield if timing slips. That discipline is much easier to maintain with active reporting and real-time monitoring tools.

How The Fractional Analyst Supports Mezzanine Execution

These best practices only matter if underwriting, servicing, and reporting stay tight after closing. That’s where The Fractional Analyst comes in.

Its free models let teams test IRR, value decline, budget overruns, and rate shocks before closing. You can also model exit timing and PIK during underwriting. That matters because both can move IRR more than coupon.

Once underwriting is done, the focus shifts to active monitoring. Its analyst team tracks cash traps, debt yield, and extension tests after closing. CoreCast gives in-house teams a self-service platform for monitoring and reporting. That support works best when it ties back to the structure, covenant, and exit assumptions shown in the tables below.

The platform also covers pitch deck creation, market research, and investor and lender reporting. That reporting support helps keep lenders aligned on downside risk, payoff timing, and recovery paths.

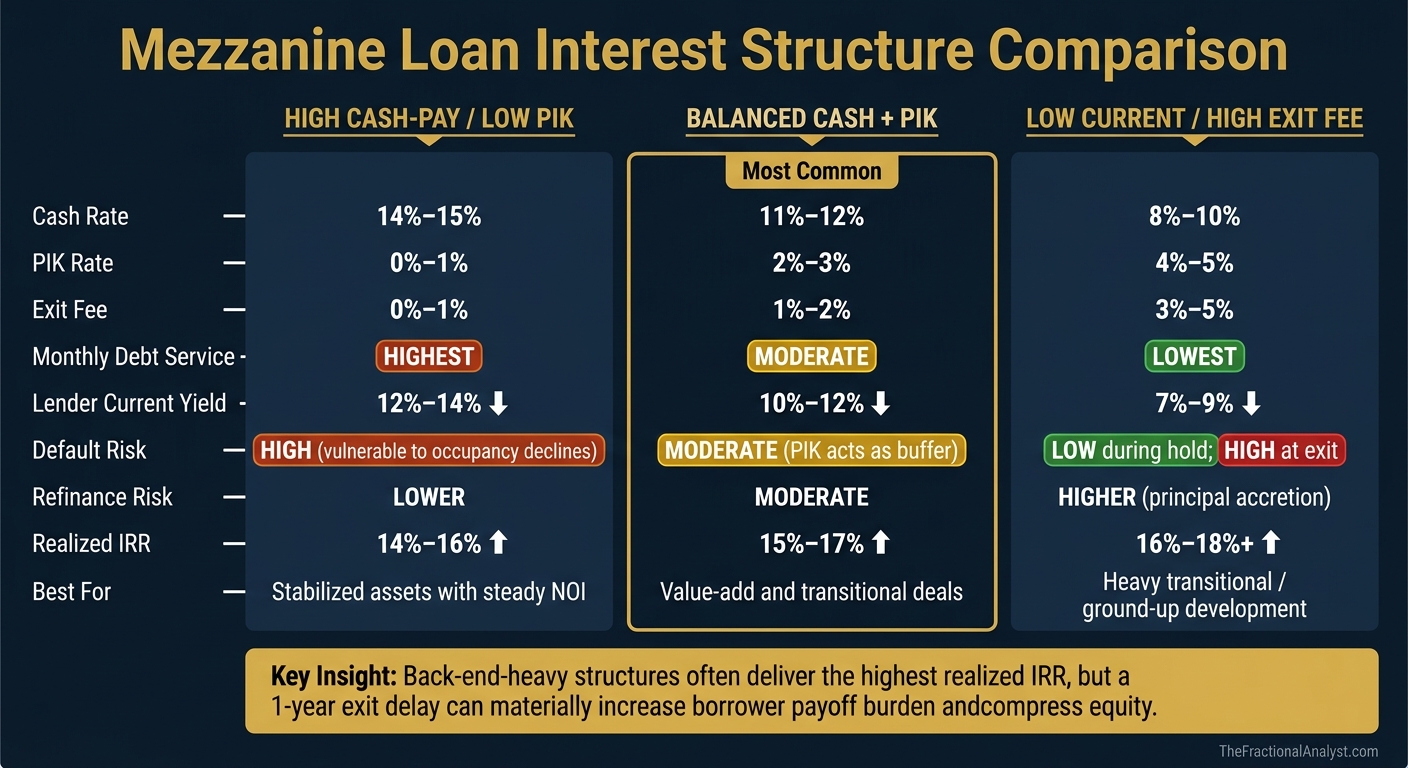

Interest Structure Comparison Table

Mezzanine Loan Structure Comparison: Cash-Pay vs. PIK vs. Exit Fee

This table shows how each structure shifts current yield, borrower burden, and exit IRR. The goal is simple: match the coupon mix to the asset’s cash-flow pattern and expected exit timing.

Cash-pay, PIK, and fees shape both the borrower’s payment load and the lender’s return. High cash-pay with low PIK tends to fit stabilized assets with steady NOI, but it pushes monthly debt service up. A balanced mix of cash-pay and PIK lands in the middle. It lets part of the interest build over time while keeping current payments at a more manageable level. Low current-pay with a high exit fee keeps monthly debt service light during heavy transition periods, but there’s a catch: the loan balance grows, and back-end fees can create real pressure when it’s time to refinance.

The table below shows how structure changes borrower pressure and lender return, using current-pay rates of 11%–15% and PIK adding another 1%–3% on top [4].

| Feature | High Cash-Pay / Low PIK | Balanced Cash + PIK | Low Current / High Exit Fee |

|---|---|---|---|

| Cash Rate | 14%–15% | 11%–12% | 8%–10% |

| PIK Rate | 0%–1% | 2%–3% | 4%–5% |

| Exit Fee | 0%–1% | 1%–2% | 3%–5% |

| Borrower Monthly Debt Service | Highest | Moderate | Lowest |

| Lender Current Yield | High (12%–14%) | Moderate (10%–12%) | Low (7%–9%) |

| Default Risk | High; vulnerable to occupancy declines | Moderate; PIK acts as a buffer | Low during hold; high at exit |

| Refinance Risk at Maturity | Lower | Moderate | Higher (principal accretion) |

| Indicative Realized IRR | 14%–16% | 15%–17% | 16%–18%+ |

The back-end-heavy setup often delivers the highest realized IRR, especially when the hold runs longer. That sounds great on paper for the lender. For the borrower, though, it can turn into a tight squeeze. A one-year delay in exit timing can materially increase the payoff amount and compress borrower equity [9].

From there, it helps to look at how much extra upside each structure can add beyond the base coupon.

Upside Participation Comparison Table

Once the coupon mix is set, the next call is simple: should the lender also get a piece of the upside? In mezzanine deals, that upside usually shows up in one of three forms.

A coupon-only structure is the cleanest option. The lender earns current-pay interest and, when the deal allows it, PIK accruals under standard debt covenants. This setup tends to fit stabilized assets, core-plus deals, and short-term bridge loans.

Add warrants, and the return profile changes. The lender still gets the coupon, but now also has equity upside through warrant coverage or option value. That makes sense in LBOs, growth financings, and transitional deals where exit value could move in a big way.

Profit-sharing or sale-proceeds participation goes a step further. Here, the lender gets a preferred return plus a share of leftover profits or sale proceeds. The trade-off is more moving parts: more consent rights, a more layered exit waterfall, and more friction when it’s time to sell or distribute cash.

| Feature | Coupon Only | Coupon + Warrants | Coupon + Profit Participation |

|---|---|---|---|

| Return Potential | Capped at interest and fees | Moderate upside through equity value at exit | Highest; participates in cash flow or sale proceeds |

| Governance Complexity | Low; standard debt covenants and UCC pledge | Moderate; requires anti-dilution and exercise mechanics | High; consent rights, audit rights, and waterfall complexity |

| Sponsor Alignment | High; sponsor retains all residual upside | Moderate; sponsor gives up some upside on exercise | Lower; adds friction on exits and distributions |

| Enforcement Position | UCC foreclosure (30–60 days) [4] | UCC foreclosure plus equity rights | Contractual remedies such as GP removal or forced sale [3] |

| Best Deal Types | Stabilized, core-plus, short-term bridges | LBOs, growth financings, transitional deals | Heavy transitional, opportunistic, redevelopment |

One practical point matters here: many agency lenders limit equity-like participation features. So before adding warrants or profit-sharing, check for senior-lender consent [3][4]. And as the lender’s upside share grows, control rights matter more too.

Covenant and Intercreditor Protection Snapshot

Once the upside is priced in, the next job is simple: protect it with covenants and intercreditor rights that shape who gets to act, and when. The coupon, PIK, and kickers set the return on paper. This package determines whether that return is ever collected.

At the center of it all is timing of control. Weak protections can slow action while collateral value slips away. Strong protections can shift control back to the mezzanine lender before that slide gets worse.

The key issue isn't whether a default happens. It's who controls the response.

| Protection Feature | Weak Protection | Strong Protection |

|---|---|---|

| DSCR / Debt-Yield Triggers | Low thresholds; no cash sweep; distributions allowed during stress | Tight triggers (e.g., 1.25x); automatic cash sweep to reserves or principal [12] |

| Debt Restrictions | Large permitted-indebtedness baskets; loose covenants | No additional debt allowed; strict SPE requirements |

| Reserve Requirements | Minimal or no CapEx/TI/LC reserves; borrower-controlled | Fully funded reserves; lender-controlled; replenished via cash sweeps |

| Cure Rights | Short (10 days); monetary defaults only; limited occurrences | Long (30–60 days); covers monetary and non-monetary defaults; multiple occurrences [5][11] |

| Standstill Period | Long (180+ days); blocks all mezzanine action | Short (90 days); allows mezzanine lender to act if the senior lender is not proceeding [12] |

| Transfer Control | Senior consent required for equity transfer; no pre-approved buyer | Pre-approved "Qualified Transferee" status; no due-on-sale trigger [11] |

| Transfer / Workout Rights | No right to purchase senior debt | Right to buy senior debt at par; control of the workout [6] |

The stronger the intercreditor rights, the faster the path to recovery and the more say the mezzanine lender has in a default. One term stands out here: the senior buyout right. If the senior lender starts moving toward foreclosure, that right can hand workout control to the mezzanine lender.

This matters most when the business plan starts to drift off course. That's when return preservation comes down to one thing: control.

Exit Path and Duration Planning

Once control rights are in place, the next step is picking the payoff path. Exit timing can shift mezzanine IRR more than the coupon itself. And the exit route shapes where the lender’s return comes from: current pay, PIK accretion, fees, or upside participation.

Use the table below to line up the exit path with the main return source.

| Exit Path | Main Lender Risk | Effect on Lender Return |

|---|---|---|

| Refinance | Prepayment risk | Pays coupon and fees; usually caps upside. |

| Asset Sale | Low reinvestment risk | Best path for kicker realization and full principal recovery. |

| Recapitalization | Extension risk | May add new capital and dilute junior claims. |

| Cash Flow | Longest-hold risk | Uncommon; PIK accrual typically outpaces cash flow growth. |

Refinancing is the standard exit for bridge-to-stabilization deals. In that setup, mezzanine capital gets taken out by lower-cost permanent financing once the asset hits a target debt yield or occupancy level. [13][1] Asset sales are where equity kickers tend to pay off, with the return showing up at sale rather than building during the hold. [13]

In plain terms, underwrite the loan on the assumption that a refinance or sale will take it out. Operating cash flow usually won’t.

The mezzanine term and any extension rights should match the actual exit window, not the sponsor’s base case. One risk lenders often underrate is same-maturity risk. Mezzanine loans often mature at the same time as the senior loan, so if the senior lender doesn’t extend, the mezzanine lender runs into that same refinancing wall. [3]

That’s why extension options should be tied to conservative operating cases. Prepayment premiums also matter, because they help protect yield if the borrower gets out early. [9] And this isn’t some edge-case issue. With about $875 billion in commercial mortgages maturing in 2026, refinancing pressure is very real, and extension flexibility needs to be built into the structure. [5]

After timing, the remaining task is matching structure to asset type and sponsor quality.

Mezzanine Structure by Asset Type and Sponsor Profile

Once timing is set, the next step is structure. The right setup should fit both the asset's cash flow pattern and the sponsor's track record. Put simply: a steady asset can support a different mezzanine structure than a shaky one.

Use this table to match the structure to cash-flow swings and sponsor quality.

| Asset Type | Risk Level | Recommended Structure | Key Protection |

|---|---|---|---|

| Stabilized Multifamily | Low | Current-pay mezz or preferred equity | High DSCR (1.25x+) |

| Hospitality | Moderate/High | Current-pay + PIK | Lower attachment point (max 75–80% LTC) |

| Lease-up Office | High | PIK-heavy preferred equity | Cash trap triggers and lease-up hurdles |

| Ground-up Development | Very High | PIK-heavy or soft preferred equity | Cash flow preservation |

Sponsor strength matters just as much as the asset itself. A sponsor with deep resources and a solid track record usually gets more lender comfort, which can tighten pricing by 50 to 100 bps and come with tighter intercreditor terms plus quarterly reporting. That often applies to institutional sponsors with $50 million+ in AUM. [4]

Weaker sponsors get a very different deal. First-time groups or thinly capitalized borrowers, especially those putting in less than 5%–10% equity, are often steered toward joint-venture equity or asked to co-invest 10%–20%. [4][8]

If mezzanine is extended to a weaker sponsor, controls need to do more work. That usually means:

- Monthly reporting

- Broader consent rights

- Cash-trap triggers

- Removal rights tied to technical or operating covenant breaches [5][1]

This is where structure stops being theory and starts acting like a guardrail. A strong sponsor may earn more flexibility. A weaker one usually needs tighter checks built into the deal from day one.

Conclusion

Mezzanine returns come from the structure of the deal: underwriting, pricing, controls, and exit timing. In practice, attachment point, PIK, intercreditor rights, and maturity timing often have more impact on realized IRR than the stated rate itself. [1][9]

That only works if the loan is watched closely after closing. Active servicing helps keep the original deal terms in place and can protect returns when a sponsor’s plan starts to drift. [1]

Build the structure right on day one, then monitor it closely.

FAQs

What is the biggest driver of mezzanine returns?

The main force behind mezzanine returns is financial leverage.

By adding a mezzanine tranche between senior debt and common equity, sponsors can push leverage past what senior lenders usually allow. In many cases, that means moving from about 65% of project cost to 85% or 90%.

That can lift returns when a property’s unlevered returns are higher than the cost of mezzanine capital. The math is pretty simple: the sponsor puts in less equity, gives up less ownership, and can drive a higher IRR on that smaller equity check.

When should mezz debt use PIK instead of cash-pay?

Mezzanine debt should use PIK instead of cash-pay when preserving liquidity is critical and the asset can’t support full current-pay obligations.

This comes up most often during construction, lease-up, capex cycles, or market downturns. PIK can ease near-term cash flow because interest gets deferred and added to principal instead of being paid in cash each period.

That said, there’s a tradeoff. The deferred interest increases the amount due at maturity, which can put more pressure on the refinance or exit.

How do I know if refinance risk is too high?

Refinance risk gets high when a property’s stabilized value may not produce enough loan proceeds at maturity to pay off both the senior debt and the accrued mezzanine balance.

That risk gets worse if the exit cap rate goes up. A higher cap rate can push the property value down, which can also shrink the size of a new senior loan. PIK interest adds pressure too, because it keeps increasing the total payoff over time.

When you model the exit, use conservative valuation scenarios instead of best-case projections.