Ultimate Guide to Title and Survey Review

When buying property, ensuring you understand its legal status and boundaries is vital. A title review verifies ownership and flags issues like liens or unpaid taxes, while a survey confirms property boundaries and identifies problems like encroachments or easements. These steps are critical to avoid disputes and protect your investment.

Key takeaways:

- Title Commitments: Preliminary documents that outline ownership, liens, and exceptions.

- Surveys: Map property lines and physical features, identifying discrepancies or encroachments.

- Common Issues: Mismatches in legal descriptions, unrecorded easements, or boundary conflicts.

- Fixing Problems: Use new surveys, endorsements like ALTA 25-06, or legal actions to resolve disputes.

- Lender Requirements: Title insurance and updated surveys are often mandatory for financing.

Title and Survey Review Process for Property Buyers

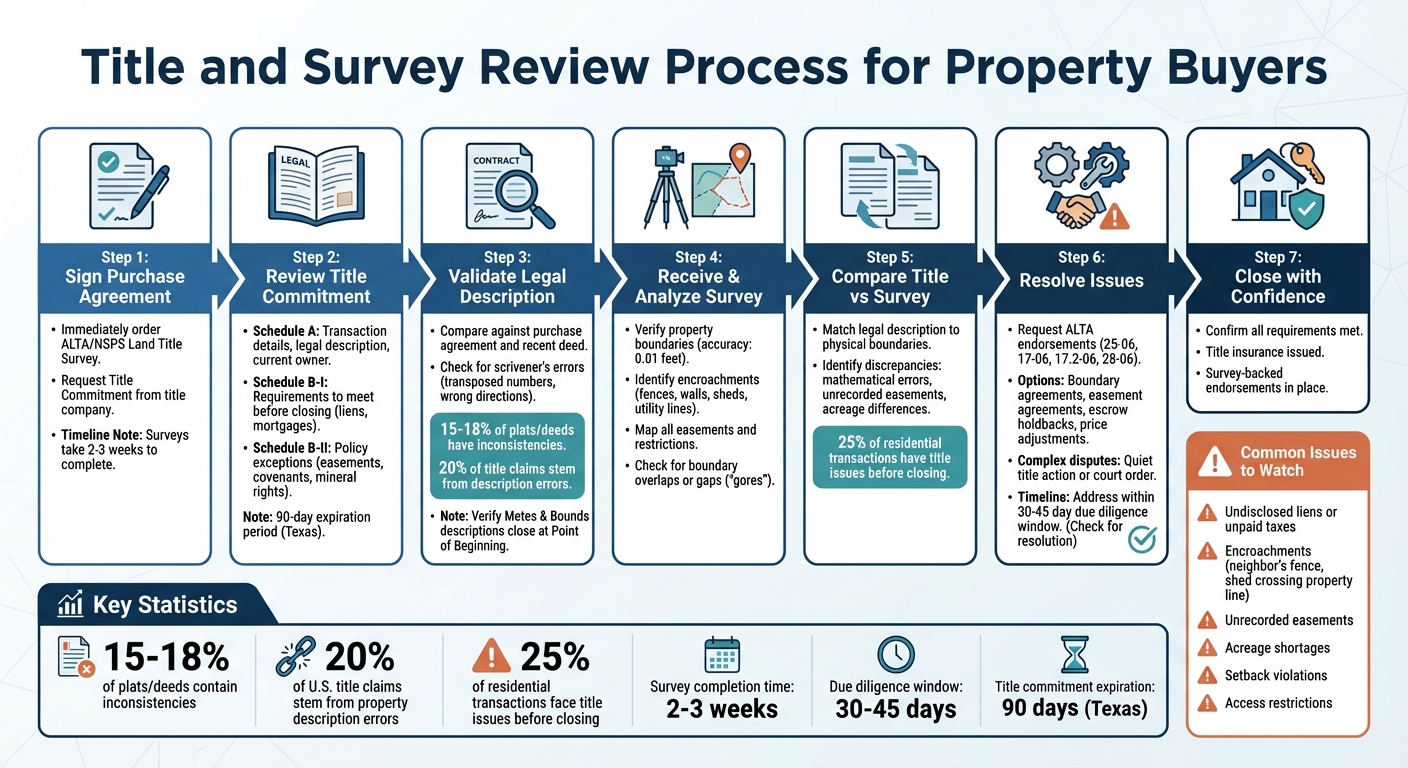

Title Commitments and Legal Descriptions

What's in a Title Commitment

A title commitment is essentially a promise from a title company to issue a title insurance policy once specific conditions are met. It’s not the final insurance policy but serves as a preliminary document to guide the process. Amanda Farrell, Content Marketing Strategist at PropLogix, explains it well:

"The title commitment is the document a title company or real estate law firm creates as a promise to issue a title insurance policy. It’s basically a road map that the title agent uses to cure any defects in order to transfer the title free and clear." [6]

The commitment is divided into three main sections:

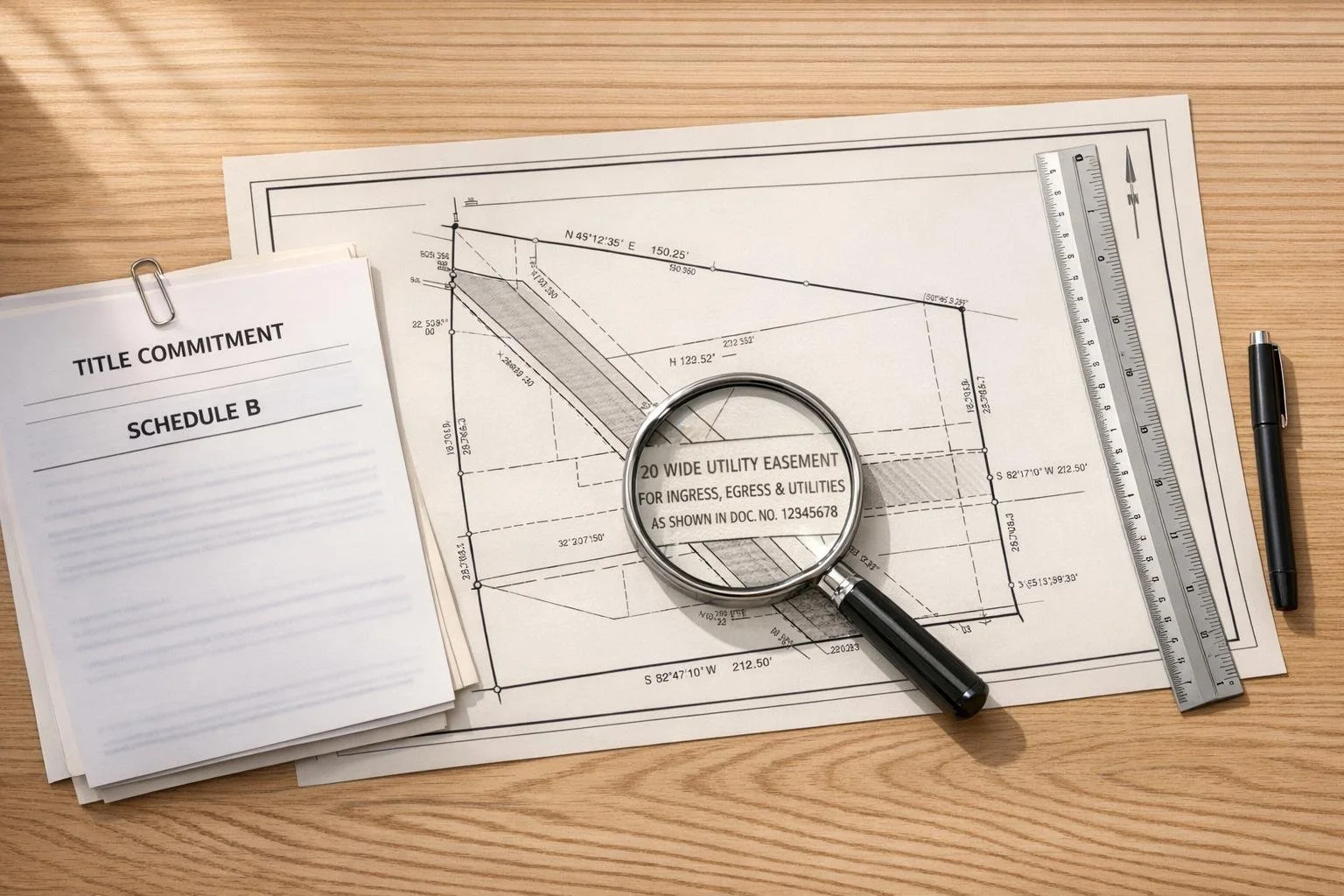

- Schedule A: This section lays out the transaction details, including the effective date, policy amount, proposed insured party, current owner, and the property's legal description.

- Schedule B-I: Lists requirements that must be met before closing, such as resolving tax liens, paying off existing mortgages, or providing necessary documentation like corporate resolutions.

- Schedule B-II: Covers exceptions that the insurance policy won’t protect against, such as utility easements, restrictive covenants, or mineral rights.

In states like Texas, the obligations outlined in the title commitment generally expire 90 days after the effective date or when the final policy is issued - whichever happens first [5]. This document is critical for securing financing. As Triumph Title Group points out:

"Without a title commitment a bank will not lend you money to purchase the property. They want to know the risks upfront prior to agreeing to fund the purchase." [10]

How to Validate Legal Descriptions

The legal description in Schedule A is the ultimate identifier of a property, far more precise than a street address. Akkad Bakhsh from First Choice Surveying stresses this point:

"Surveyors should never use an address to survey because an address could be wrong. Using the legal description tells us exactly where the property is at by locating those certain permanent reference points, or monument points, to find the property." [9]

To ensure the legal description is accurate, compare it against the purchase agreement and the most recent deed in the chain of title. Watch out for "scrivener’s errors", such as transposed numbers (e.g., 59 feet instead of 95 feet) or incorrect directional indicators (e.g., NW instead of NE). Research indicates that 15% to 18% of plats or deeds have inconsistencies that could lead to legal disputes, and up to 20% of title claims in the U.S. stem from errors or ambiguities in property descriptions [8].

For Metes and Bounds descriptions, confirm that the measurements form a closed loop, returning exactly to the Point of Beginning (POB). If they don’t, the description is flawed and could create title issues. For Lot and Block descriptions, refer to the recorded plat map to check for easements, setbacks, or public rights-of-way that might not be mentioned in the deed. Finally, avoid relying on outdated surveys. Request a new professional land survey to confirm the legal description matches the physical property boundaries and to identify potential encroachments, like a neighbor’s fence or shed crossing onto your land [9][7].

sbb-itb-df8a938

Survey Review: Boundaries, Encroachments, and Easements

Verifying Property Boundaries

When you receive the title commitment, the first step should be ordering a professional ALTA/NSPS Land Title Survey. This survey is widely regarded as the standard for commercial transactions because it ensures consistency and reliability for lenders, buyers, and title companies. As Wendy S. Gibbons and Vincent Macauda explain:

"The ALTA Survey has become the gold standard for [deleting survey exceptions]. When provided to title underwriters, they will remove the general exception and list only exceptions they find in the ALTA Survey." [4]

Start the survey process as soon as you have a signed purchase agreement and title commitment, as these surveys typically take 2 to 3 weeks to complete [11]. The surveyor will locate original monuments and compare field findings with the property's record description, noting any discrepancies with an accuracy of up to 0.01 feet [12]. Additionally, they’ll map out every easement and restriction listed in the title commitment onto the survey itself [11][4].

To confirm that the property described in Schedule A of your title policy matches the surveyed land, request the ALTA 25-06 "Same as Survey" endorsement [4]. If you're considering using an older survey to save money, make sure the seller provides a "no-change-since-the-date-of-the-last-survey" affidavit. Keep in mind, though, that title companies may reject surveys older than the adverse possession period in your state, which ranges from 5 years in California to 21 years in Pennsylvania [4][12].

Once boundaries are verified, the next step is to check for any structures or easement issues that could complicate the transaction.

Finding and Fixing Encroachments

Encroachments occur when physical structures cross property lines, and they’re surprisingly common. Examples include fences, walls, patios, roof eaves, sheds, garages, utility lines, or even overhanging tree branches and roots that can damage foundations [13][14]. The only reliable way to identify these is through a professional boundary survey or an ALTA/NSPS survey, which accurately maps out any intrusions [13][14][4].

If an encroachment is identified, you can resolve it through boundary agreements, revocable licenses, easement agreements, or legal actions like Quiet Title, Ejectment, or Injunction [14][12][15][13]. Timing is critical here: if an encroachment remains unchallenged for the statutory period in your state (5 to 21 years, depending on location), the encroacher could gain legal ownership through adverse possession [14][12].

When drafting your purchase contract, include clauses that address responsibility for resolving encroachments. For commercial properties, the ALTA 28-06 endorsement can provide protection against forced removal of buildings encroaching on easements [4].

Beyond encroachments, easements play a significant role in determining how a property can be used.

Easements and What They Mean for Your Property

Easements grant others the right to use specific parts of your property for purposes like utility maintenance, shared driveways, or conservation [15]. They directly influence where you can build, how parking layouts are designed, and whether future expansions are feasible [2][4]. Title companies require surveys to identify unrecorded easements and to remove standard survey exceptions from your title policy [4]. Catching these issues early can save you from the costly problem of having to remove improvements that encroach on an easement area [4].

| Easement Type | Use | Property Impact |

|---|---|---|

| Utility | Access for power, water, or sewage | Restricts building over underground or overhead lines [15]. |

| Access | Shared driveways or paths | Limits privacy or fencing; shared use of land [15]. |

| Conservation | Preserves land in its natural state | Prohibits future development or construction [15]. |

| Easement in Gross | Benefits a specific person/entity | Specific to the holder; may not transfer with the property [15]. |

Always compare the physical survey with the title commitment to identify unrecorded easements or discrepancies between the legal description and on-site conditions [2][4]. Use the survey data to secure endorsements like ALTA 17-06 (Access and Entry) or ALTA 17.2-06 (Utility Facility), which ensure access to public roads and utilities [4]. When ordering an ALTA/NSPS survey, request "Table A" optional items - such as utility locations or flood zone data - to address specific risks tied to your project [4]. Be cautious of "blanket easements" that lack defined boundaries, as they can impact the entire property until a specific route is determined [4].

Thoroughly identifying these survey issues is key to assessing risks and ensuring smooth financing.

CRE Legal Minute Episode 11 - Title and Survey Review

Comparing Title and Survey Documents

A title commitment identifies the legal owner of a property and any claims or liens against it, while a survey defines the property's physical boundaries and features. Ideally, these documents should match. However, discrepancies are common. Texas real estate attorney Nixon Daughtrey puts it bluntly:

"Survey problems kill more Texas real estate deals than financing failures. They surface at the worst possible moment" [16].

Title issues affect around 25% of residential real estate transactions before closing [17]. This section dives into the differences between title commitments and surveys, setting the groundwork for addressing discrepancies and their resolutions later.

Typical Mismatches Between Title and Survey

Several common issues arise when comparing title and survey documents:

- Mathematical errors: These may include deviations in bearings from the recorded plat or missing boundary markers [12]. For instance, a property marketed as 5 acres might measure only 4.2 acres [16]. Such discrepancies can shift negotiations, potentially leading to price reductions or canceled deals.

- Encroachments and easements: A survey might reveal structures like fences, sheds, or driveways crossing property lines - issues not reflected in the title commitment [16][17]. Similarly, unrecorded easements, such as utility lines or access paths, may appear on the survey but not in the title documents [16][4].

- Boundary overlaps or gaps: Some properties may have "gores" - strips of land that either fall outside any ownership chain or are claimed by conflicting plats [12][4]. Lenders often refuse to fund loans until such disputes are resolved, and title underwriters won't insure properties with unresolved boundary conflicts [12][17].

How to Fix Discrepancies Before Closing

Addressing these discrepancies early can prevent delays or deal failures. Start by ordering an ALTA/NSPS survey immediately after signing the purchase agreement [16]. Survey issues often emerge within two weeks of closing [16]. Ensure that the legal description in Schedule A matches the survey findings, and request the ALTA 25-06 "Same as Survey" endorsement to align the title policy with the survey [4].

For unresolved issues, consider the following strategies:

- Escrow holdbacks: If a problem can't be resolved before closing, negotiate to set aside funds for post-closing fixes [16].

- Acreage adjustments: When surveys reveal acreage shortages, buyers may negotiate price reductions or seller credits [16].

- Complex disputes: For issues like adverse possession claims or overlapping plats, a quiet title action or court order may be necessary. Resolving these typically requires both a licensed land surveyor and a real estate attorney [12][17].

These proactive measures help address the risks tied to title-survey conflicts, paving the way for smoother transactions and clearer property boundaries.

Using Title and Survey Review in Financial Analysis

Risk Assessment with Title and Survey Data

Title and survey findings play a crucial role in evaluating risks and shaping financial projections. A thorough title review ensures fee simple ownership, minimizing the chances of future disputes[3]. Issues like undisclosed liens, outdated mortgages, mechanics liens, or unpaid taxes can significantly impact a property's value and should be factored into acquisition pricing[2].

Surveys, on the other hand, help identify potential boundary encroachments - like buildings or fences - that could result in costly legal disputes or even forced removals[1]. They also highlight zoning and setback compliance issues that might restrict future development or lead to fines. Additionally, surveys confirm whether the property has legal access to public roadways and essential utilities, which are critical for its usability and value[4]. These findings directly influence financial modeling and guide pricing strategies.

When underwriting deals, it’s essential to ensure the title's legal description aligns with the survey boundaries. ALTA endorsements come in handy to mitigate risks. For instance, ALTA 17-06 ensures access rights, ALTA 17.2-06 covers utility access, ALTA 19-06 confirms contiguity between parcels, and ALTA 25-06 verifies that the title policy matches the survey[4]. This alignment between title, survey data, and financial modeling forms the foundation for sound investment decisions.

Tools and Platforms for Streamlined Analysis

Given the risks involved, using reliable tools is key to accurate financial forecasting. The Fractional Analyst (https://thefractionalanalyst.com) provides both direct analyst support and self-service tools through its CoreCast platform. This platform allows you to seamlessly integrate title and survey findings into your underwriting and risk assessments. Their team translates survey findings - like setback violations, unrecorded easements, and access issues - into measurable financial impacts. This could involve adjusting the purchase price, budgeting for easement acquisitions, or modeling the costs of legal resolutions.

CoreCast also offers custom analyses that incorporate title risks, such as mechanics liens or boundary disputes, into financial projections. For teams managing multiple acquisitions, the platform simplifies the process of verifying site metrics from ALTA surveys. This includes metrics like building footprints, parking counts, and flood zone classifications, ensuring they align with underwriting assumptions. By streamlining these processes, CoreCast supports both acquisition and ongoing asset management efforts.

Conclusion

Title and survey reviews aren't just procedural steps - they're essential tools to protect your financial interests when acquiring property. These reviews confirm ownership, verify boundaries, and reveal potential legal or physical challenges that could jeopardize your investment.

Issues like undisclosed liens, boundary disputes, or access restrictions can derail transactions and lead to unexpected expenses. To avoid this, order your ALTA survey as soon as the purchase agreement is signed, and work with an experienced real estate attorney to review any title exceptions. With the due diligence window typically lasting 30–45 days, addressing problems early gives you the opportunity to renegotiate terms or require the seller to resolve issues before you commit funds. Acting quickly and resolving discrepancies ensures your investment is safeguarded from unpleasant surprises after closing.

Survey-related endorsements, such as ALTA 17-06 for access rights and ALTA 25-06 to align your title policy with the survey, provide extra protection by addressing specific risks that could impact your property's value or usability.

Whether you're purchasing your first property or managing a portfolio, thorough title and survey reviews are key to making informed decisions and managing assets effectively. The upfront costs pale in comparison to the legal disputes and development challenges you can avoid. By incorporating these reviews into your financial planning, you ensure each acquisition is based on accurate information and reduced risk.

FAQs

When should I order an ALTA/NSPS survey?

When dealing with commercial real estate transactions, refinancing, or development projects, ordering an ALTA/NSPS survey is a critical step. This survey provides detailed information about property boundaries, easements, and improvements - essential details for title insurance or addressing legal requirements.

What if the survey doesn’t match the legal description?

If a survey doesn't match the legal description of a property, it can lead to disputes, misunderstandings, and even financial risks. Misplaced boundary lines might cause ownership conflicts or disagreements over property limits. To prevent these issues, it's crucial to identify and address any inconsistencies early during the review process.

Which ALTA endorsements do I actually need?

When it comes to ALTA endorsements, the ones you need will vary based on the property's risks and what the lender requires. Some of the more commonly used endorsements include:

- ALTA 3 Zoning Endorsement: Offers coverage related to zoning compliance issues.

- ALTA 8.1 Environmental Lien Endorsement: Protects against losses from environmental liens that could affect the property.

- ALTA 9 Restrictions, Encroachments, and Minerals Endorsement: Addresses concerns like encroachments, property restrictions, and mineral rights.

These endorsements go beyond the standard title insurance, offering extra protection for specific risks tied to zoning, environmental factors, and encroachments.