1031 Exchange Boot: Tax Planning Tips

If you're selling an investment property and planning a 1031 exchange, avoiding "boot" is critical to deferring taxes. Boot refers to any non-like-kind value received during the transaction, such as cash, debt relief, or personal property. Here's what you need to know:

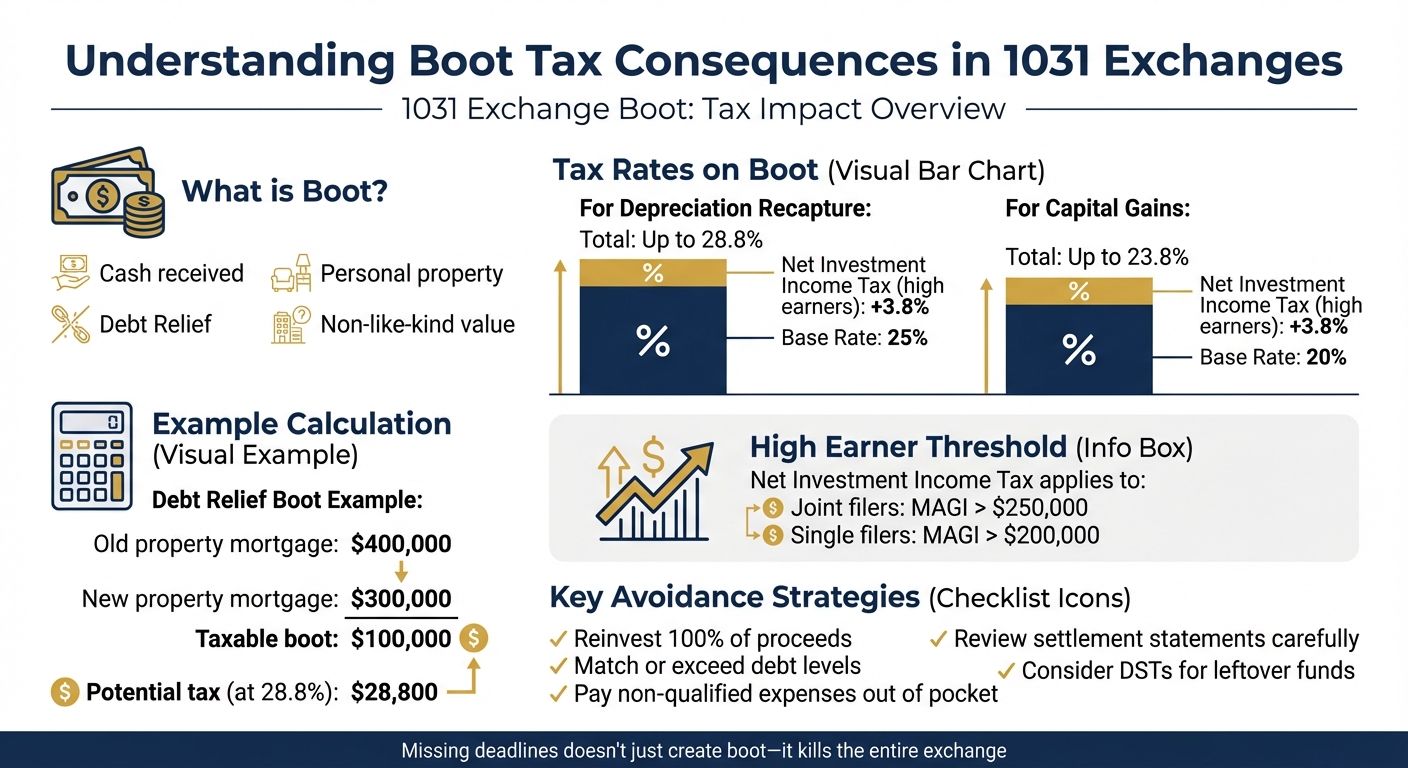

- Boot Triggers Taxes: Any boot received is taxed immediately, with rates up to 25% for depreciation recapture, 20% for capital gains, plus a 3.8% surtax for high earners.

- Avoid Cash Boot: Reinvest all sale proceeds into a replacement property of equal or greater value. Pay non-qualified expenses (e.g., property taxes, HOA dues) out of pocket to prevent taxable boot.

- Manage Debt Levels: Ensure the replacement property's mortgage matches or exceeds the debt on the sold property. You can substitute cash for debt to meet this requirement.

- Check Settlement Statements: Review closing documents carefully to avoid accidental boot caused by improper use of exchange funds for non-qualified expenses.

- Use DSTs as Backup: Delaware Statutory Trusts (DSTs) can help reinvest leftover funds or meet debt requirements, ensuring full tax deferral.

1031 Exchange Boot Tax Rates and Consequences for Investment Property Owners

1. Avoiding Cash Boot

Reinvest 100% of Sale Proceeds

The easiest way to steer clear of cash boot during a 1031 exchange is to reinvest all the proceeds from the sale into the replacement property. To meet this requirement, the replacement property must have a purchase price that’s at least equal to the net sale price of the property you’re selling [6]. For example, if your net proceeds from the sale are $1,000,000, the replacement property must cost no less than $1,000,000. This ensures you maintain the full tax deferral benefits of a 1031 exchange.

"The reinvestment goal of any 1031 tax deferred exchange should be to buy replacement property of equal or greater value and to use up all the exchange proceeds in the closing of the replacement property without getting any cash back."

If the replacement property doesn’t use up all the proceeds, consider putting the remaining funds into a Delaware Statutory Trust (DST). DSTs allow for fractional ownership, making it possible to reinvest leftover funds instead of receiving taxable cash boot [5].

For situations where reinvesting all proceeds in a single property isn’t practical, alternative structures like DSTs can help you maximize tax deferral.

Pay Non-Qualified Expenses Out of Pocket

Another key strategy to avoid cash boot is ensuring that non-qualified expenses are paid from your personal funds - not exchange proceeds. These expenses include things like property taxes, insurance premiums, inspection fees, HOA dues, rent credits, security deposits, loan origination fees, or repair costs. Using exchange funds for these costs could trigger taxable boot, even for small amounts [4].

To avoid this, carefully review your settlement statement well before closing. Look for any charges that could mistakenly use exchange funds. If you find non-qualified expenses, ask your settlement agent to mark them as "paid outside closing" or have the seller handle these costs [4]. This small but important step can help ensure your exchange funds remain untaxed.

sbb-itb-df8a938

What Is "Boot" In a 1031 Exchange? A Simple Rule to Remember

2. Managing Debt Levels

Beyond avoiding cash boot, keeping a close eye on your mortgage debt is just as important when trying to steer clear of taxable boot.

Replace Debt Dollar-for-Dollar

The IRS considers any reduction in mortgage debt as taxable income. This is called mortgage boot (or debt relief boot) and is treated as though you’ve pocketed the difference[1]. To sidestep this tax burden, your replacement property’s mortgage must at least match the debt level of the property you’re selling (which you can calculate using a multifamily model)[1].

For instance, if you sell a property with a $400,000 mortgage, your replacement property must assume at least $400,000 in debt. If the new mortgage is less - say $300,000 instead of $400,000 - you’ll be taxed on the $100,000 difference. To avoid this, you can contribute personal funds at closing to make up the gap. The IRS allows you to substitute cash for debt on a dollar-for-dollar basis[1].

"The IRS treats that reduction [in mortgage balance] as if you pocketed the savings."

- LegalClarity Team[4]

It’s worth noting that while taking on more debt than your original mortgage won’t trigger taxes, it does increase your financial exposure and risk[9]. That’s why it’s essential to plan your financing carefully and ensure it aligns with these debt requirements.

Coordinate with Your Lender Early

The 1031 exchange process gives you 180 days to complete the transaction, so securing financing early is critical[1]. Talk to your lender about specialized loan products, like DSCR loans, that can help you meet the required debt levels within this tight timeframe.

Be cautious with refinancing, though. If you refinance within six months of starting your 1031 exchange, the IRS might view it as a tax avoidance tactic, which could jeopardize the entire transaction[1]. To avoid surprises, review your preliminary closing statements with your tax advisor just a few days before closing to catch any potential issues that could lead to unexpected boot[1].

3. Structuring Transactions

Getting the structure of your exchange right is essential if you want to avoid any unintended taxable boot. A well-structured 1031 exchange ensures you maintain full tax deferral. Every part of the transaction should be aligned to achieve this goal.

Review Settlement Statements Line-by-Line

Settlement statements are a common place where taxable boot can sneak in. For instance, using exchange funds to cover non-qualified expenses - like loan origination fees, property tax prorations, or rent credits - can result in taxable boot [4][7]. To avoid this, go over your draft closing statements with your tax advisor several days before closing. This allows you to clearly separate valid exchange expenses (like commissions, qualified intermediary fees, and title insurance) from financing-related costs (such as appraisals and loan fees) that could create boot [10]. Make sure any non-qualified expenses are paid outside of the exchange, as previously mentioned.

"Small details at closing can have major financial impacts. Address them early to safeguard your transaction and long-term plans."

If adjustments in the settlement statement still leave you with excess funds, there are alternative strategies to handle the situation, such as using Delaware Statutory Trusts (DSTs).

Use Delaware Statutory Trusts as a Backup

DSTs are a practical option for reinvesting leftover funds and meeting debt ratio requirements. They offer flexibility during the 45-day identification period [8][11][12][3]. By allowing precise reinvestment down to the last penny, DSTs can help you avoid taxable cash boot [8][11]. This ensures you complete your exchange within the 180-day timeframe while staying compliant with boot rules.

4. Tax Reporting and Planning

Once you've structured your exchange to avoid boot, the next step is accurate tax reporting to complete your deferral strategy.

File Form 8824 and Track Your Recognized Gain

Every 1031 exchange must be reported using IRS Form 8824 during the tax year the exchange occurs [4][3]. This form helps calculate any taxable gain resulting from boot. Specifically:

- Line 15: Report any boot received.

- Line 19: Show your total realized gain.

- Line 20: Indicate your recognized (taxable) gain, which is the smaller amount between your total realized gain and the boot received [4][3].

The IRS uses a specific ordering rule to determine how boot is taxed. Depreciation recapture, taxed at 25%, is applied first. For high-income investors (those with a modified adjusted gross income exceeding $250,000 for joint filers or $200,000 for single filers), an additional 3.8% Net Investment Income Tax applies, bringing the federal tax rate on boot to as much as 28.8% for depreciation recapture and 23.8% for other capital gains [4].

"Boot is generally taxable in the year the exchange is completed, regardless of when the investor actually receives the cash."

- Thomas Wall, Partner, Anchor1031 [3]

For added flexibility, installment reporting can help spread out the tax liability, reducing immediate cash-flow pressure.

Use Installment Reporting to Defer Tax Liability

If boot is received as a promissory note through seller financing, you can defer tax payments over several years using Form 6252 [4][3]. This method allows you to pay taxes only as payments are received, rather than being taxed on the full amount in the exchange year. This approach is particularly useful if you're financing the buyer of your replacement property or structuring a deal with deferred payments.

Proper documentation is crucial for accurate reporting. Retain settlement statements, qualified intermediary agreements, loan payoff records, and all correspondence related to fund handling [2]. If your 180-day exchange period extends beyond the typical tax filing deadline (usually April 15), file Form 4868 to request an extension and preserve your full 180-day timeframe [4].

Conclusion

To wrap up, we've explored key strategies to help avoid boot in a 1031 exchange and ensure a smooth process. Success here hinges on careful planning: match your debt levels, personally cover non-qualified expenses, and secure a replacement property of equal or greater value. As the LegalClarity Team cautions, "Missing either deadline doesn't merely create boot. It kills the entire exchange" [4]. These steps are the backbone of minimizing tax liabilities and preserving your investment.

Boot can lead to hefty taxes - up to 25% for depreciation recapture, 20% on long-term capital gains, and an additional 3.8% surtax for high-income earners. Combined, these rates can climb to nearly 28.8% [4]. To mitigate this, it's critical to review preliminary settlement statements with your tax advisor and use financial modeling tools to anticipate potential pitfalls.

Advanced tools can further streamline the process. For instance, CoreCast offers real-time sensitivity analysis and automated underwriting to ensure your replacement property meets the necessary value and debt thresholds. By consolidating all your deal data into one platform, you reduce manual errors and avoid the distractions that can derail decisions during the critical 180-day exchange period [24,25]. Early adopters can access this platform for just $50 until September 1, 2026 [13].

Ultimately, the choice is clear: either accept some cash now and pay taxes on the boot, or structure the exchange properly to preserve your full capital for future growth [3]. Partnering with experts - Qualified Intermediaries, CPAs, and financial analysts - ensures you navigate complex rules like depreciation recapture ordering and constructive receipt with confidence. Their guidance turns intricate regulations into actionable strategies that safeguard your wealth.

Be proactive: mark your 45- and 180-day deadlines right after closing, model different debt and equity scenarios, and keep exchange funds separate from personal accounts. With discipline, the right tools, and expert advice, you can turn tax deferral into a practical, long-term wealth-building strategy.

FAQs

What counts as boot in a 1031 exchange?

In a 1031 exchange, boot refers to any cash or property that doesn’t qualify as like-kind and isn’t reinvested into a like-kind property. This could include leftover proceeds, non-qualifying assets, or even a reduction in debt. Receiving boot can lead to taxable gains, so structuring the exchange thoughtfully is key to reducing potential tax obligations.

How do I avoid debt (mortgage) boot?

When navigating a 1031 exchange, it's essential to handle your debt carefully to avoid what's called a mortgage boot. To steer clear of this, make sure the debt on your replacement property matches or exceeds the debt on the property you're giving up. If the replacement property has less debt, the IRS might classify the difference as taxable income. Keeping an eye on these debt levels is key to deferring taxes and maximizing the benefits of your exchange.

Which closing costs can create boot?

Closing costs can lead to taxable boot if they include transactional expenses paid at closing that aren't reinvested into the replacement property or classified as like-kind property. Examples of these expenses include brokerage fees, escrow fees, and other similar charges. Since these costs aren't directly tied to the property exchange, they may trigger a tax liability.