5 Mezzanine Financing Case Studies in CRE

Mezzanine debt can push CRE leverage to 75% to 90%, but the extra debt only works if the exit can pay off every layer. That is the main lesson I take from these five cases across multifamily, office, retail, hotel, and industrial.

If I boil the article down, here’s what matters most:

- Multifamily: high leverage, thin debt coverage, refinance risk if rents miss

- Office development: draw risk, cost overrun risk, heavy reliance on cure and step-in rights

- Retail repositioning: lease-up timing matters, and exit value has to clear mezz plus preferred equity

- Hotel: highest pricing, common use of PIK interest, and stricter intercreditor terms

- Industrial: lower cash-flow swings, short-term recap use, often tied to a later permanent refinance

A few numbers stand out right away:

- Senior lenders often stop near 60% to 70% LTV

- Mezz can lift total leverage to 75% to 85%, and sometimes 90%

- Common pricing in the cases ran about 10% to 15%

- Standstill periods often fell in the 90- to 180-day range

- Combined DSCR tests were often around 1.10x to 1.20x

Watch Me Build a Capital Stack with Mezzanine Debt for Real Estate Development

sbb-itb-df8a938

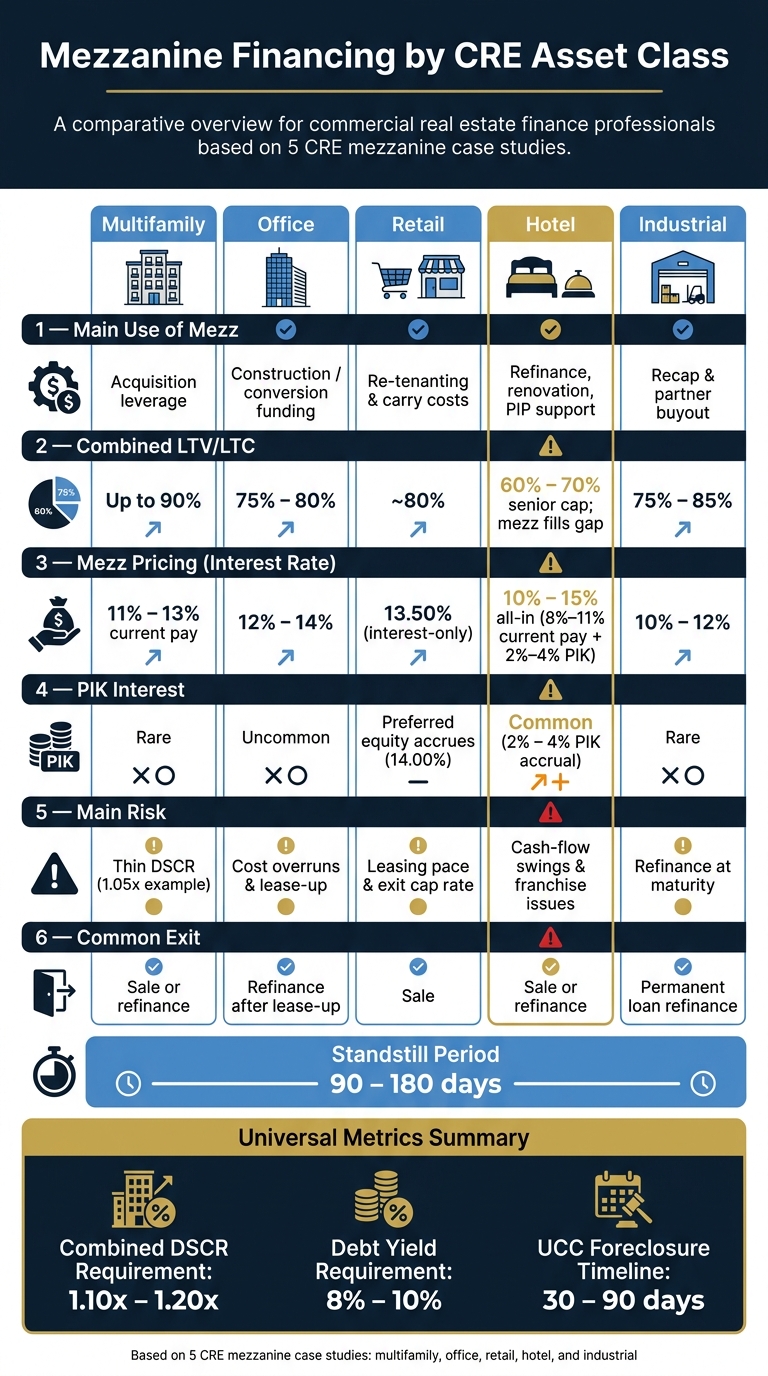

Quick Comparison

| Asset type | Main use of mezz | Main risk | Common exit |

|---|---|---|---|

| Multifamily | Acquisition leverage | Thin DSCR | Sale or refinance |

| Office | Construction/conversion funding | Cost overruns and lease-up | Refinance after lease-up |

| Retail | Re-tenanting and carry costs | Leasing pace and exit cap rate | Sale |

| Hotel | Refinance, renovation, PIP support | Cash-flow swings and brand/franchise issues | Sale or refinance |

| Industrial | Recap and partner buyout | Refinance at maturity | Permanent loan refinance |

My short take: mezzanine financing is less about the label and more about asset risk, cash flow, and the payoff plan. If stabilized NOI cannot cover total debt service - including any accrued PIK - the structure can break fast.

That’s the lens I’d use to read the full set of case studies.

Case studies 1–3: Multifamily acquisition, office development, and retail repositioning

Case 1: Value-add multifamily acquisition with mezzanine debt

In July 2022, Continental Partners arranged a $25,000,000 mezzanine loan for a 1,275-unit multifamily portfolio in San Francisco. The senior loan, a $148,000,000 CMBS facility, covered most of the capital stack, but the sponsor needed more proceeds to buy four additional properties. The mezzanine piece pushed combined LTV to 90%, carried a 12.75% interest-only rate, and matched the four-year term of the senior loan.[3]

The lender focused its underwriting on a detailed rental survey. The goal was simple: confirm that stabilized NOI could support a future takeout of both debt layers. Even then, the margin was thin. The DSCR came in at 1.05x, which left very little room if rents slipped. Repayment depended on either a sale or a refinance once the portfolio reached stabilization.[3]

That same leverage trade-off gets even sharper in construction deals, where loan proceeds are funded through draws over time.

Case 2: Ground-up office development with mezzanine construction financing

In March 2024, Mesa West Capital provided a $26,100,000 mezzanine loan to American Real Estate Partners (AREP) for the conversion of a 200,000-square-foot office building into 199 apartments in Alexandria, Virginia. The mezzanine loan sat inside a 67.5% LTC package that also included a $61,800,000 first mortgage from Bank OZK, set up as a 5-year interest-only term.[2]

This deal shows why construction mezzanine debt can feel like walking a tightrope. Exposure grows as draws are funded, and that happens at the stage when project risk is at its highest. The intercreditor agreement gave Mesa West cure rights and step-in rights, which meant it could fix a senior default or take control of the project if the sponsor defaulted. Repayment of the mezzanine loan was tied to lease-up milestones.[4]

"Having a lender in the capital stack with CRE development experience gives the senior lender additional credit support if the sponsor defaults." - Scott Rechler, CEO, RXR[4]

| Capital Layer | Collateral | Priority | Key Risk |

|---|---|---|---|

| Senior Lender (Bank OZK) | First mortgage on the asset | 1st | Construction cost overruns |

| Mezzanine Lender (Mesa West) | Pledge of equity interests | 2nd | Subordination to senior debt |

| Sponsor Equity (AREP) | Residual interest | 3rd | Total loss if the project fails |

In this kind of deal, construction cost overruns are the main risk for the mezzanine lender. If costs climb too far, the leverage cushion can disappear before a permanent takeout loan is available.

Retail repositioning changes the pressure point. Instead of build risk, the focus shifts to cash-flow timing and the sponsor's ability to lease space fast enough.

Case 3: Retail power center repositioning with mezzanine debt and preferred equity

In 2021, a regional sponsor acquired a 420,000-square-foot power center in suburban Columbus, Ohio. The asset was anchored by a mix of big-box and junior anchor tenants, with a lot of lease rollover coming up in the near term. To fund the deal, the sponsor used a $52,000,000 senior loan at 65% LTV, a $9,500,000 mezzanine loan priced at 13.50% interest-only, and a $4,200,000 preferred equity tranche with a 14.00% accrued return. That structure kept common equity at about 12% of total capitalization.[5][6]

The mezzanine loan paid for tenant improvement allowances and leasing commissions during the re-tenanting phase. The preferred equity piece helped preserve near-term cash flow because returns accrued instead of being paid currently. Underwriting leaned heavily on exit cap rates and expected refinancing proceeds to make sure stabilized NOI could retire both subordinate layers at sale. The property reached 94% occupancy within 30 months and was sold at a cap rate that matched underwriting, which repaid the mezzanine loan and preferred equity in full at closing.[5][6]

Case studies 4–5: Hotel renovation and industrial portfolio recapitalization

Case 4: Hotel renovation and repositioning with high-yield mezzanine financing

Hotel mezzanine debt works a bit differently from retail repositioning. The big reason is simple: hotels live and die by daily cash flow, and renovation downtime can hit income hard. Because that cash flow can swing so much, hotel mezzanine debt is usually the priciest option in this group. Senior lenders also tend to stay conservative, often capping hotel LTV at 60% to 70%. That leaves mezzanine debt to fill the gap when a hotel needs money for a property improvement plan (PIP) or a renovation ramp-up.[1]

A good example came in June 2026, when Driftwood Capital provided a $35,000,000 mezzanine loan to a joint venture sponsored by Chartres Lodging Group for the refinancing of the 1,841-room Sheraton Dallas Hotel. That mezzanine piece sat within a $335,000,000 capital stack, alongside a $300,000,000 senior loan from Goldman Sachs and JPMorgan Chase. The loan had a two-year term with three one-year extension options.[7]

Hotel mezzanine loans also often carry 2% to 4% PIK interest. Instead of being paid currently in cash, that interest accrues to principal. In plain English, that gives the property some breathing room when current NOI can't fully support total debt service during a renovation or repositioning.

The intercreditor agreement usually matters a lot in hotel deals. In this case, it defined a 90- to 180-day standstill period, along with cure rights and notice rules. There's also a hotel-specific wrinkle here: a mezzanine foreclosure can trigger franchise termination rights. That's why lenders often ask for comfort letters from franchisors, so they can step in without losing the hotel brand. If the hotel falls short of its business plan, lenders may also require interest reserves funded from mezzanine proceeds or sponsor equity to cover the gap.[1] Repayment most often comes from a sale or a permanent refinance once occupancy stabilizes.[1]

Case 5: Industrial portfolio recapitalization using mezzanine debt

Industrial mezzanine sits on the other end of the range. Here, the story is usually steadier cash flow and balance-sheet recapitalization, not daily operating swings. In this case, a sponsor used mezzanine debt to recapitalize an industrial portfolio, unlock trapped equity, and buy out a partner when the current senior loan could not be upsized.[8]

Underwriting centered on a few core lease metrics:

- weighted average lease term (WALT)

- tenant concentration

- the rollover schedule[8]

The mezzanine piece was short-term, typically 24 to 36 months. After that, the sponsor refinanced into a permanent institutional mortgage that paid off both the senior and mezzanine layers.[8] With a 10% to 12% coupon, industrial mezzanine can free up equity without diluting ownership, especially when the assets have already gone up in value.[8]

Taken together, these two cases make the contrast pretty clear: when cash flow is shaky, mezzanine terms get tighter; when rent rolls are steady, lenders tend to offer more flexibility.

Cross-case comparison: How mezzanine financing differs by asset class and deal structure

Mezzanine Financing by CRE Asset Class: Key Metrics Compared

Common underwriting metrics and structural terms across cases

Looking across the five cases, one pattern stands out: mezzanine terms tend to follow asset risk more than top-line leverage. The underwriting playbook stayed fairly similar from deal to deal, but leverage and pricing shifted by asset class.

In practice, multifamily and industrial usually support the highest combined leverage. Office tended to stay closer to 75% to 80%. Hotel usually came with the highest pricing and tighter intercreditor terms. Retail was more mixed, with outcomes tied to anchor quality and lease rollover risk.[1][10]

| Metric | Typical Requirement |

|---|---|

| Combined LTV / LTC | 75% – 85% [1][10] |

| Combined DSCR | 1.10x – 1.20x [1] |

| Debt Yield | 8% – 10% [1] |

| Standstill Period | 90 – 180 days [1] |

| UCC Foreclosure Timeline | 30 – 90 days [11] |

Those tests don't sit on paper by themselves. They are backed by the intercreditor and foreclosure setup. In all five deals, mezzanine debt was secured by a UCC pledge of the property-owning LLC interests, and the intercreditor agreements set the standstill periods and cure rights.[1][10][12]

That shared structure helps explain why the deals looked similar on the surface but played out differently. The main split was pricing. Multifamily came in at 11% to 13% current pay. Industrial was about 11.5% to 13.5%. Office ranged from 12% to 14%. Hotel ran 10% to 15% all-in, often with 8% to 11% current pay plus 2% to 4% PIK accrual.[1][10]

Stuyvesant Town shows what can go wrong when the intercreditor language leaves room for a fight. Mezzanine lenders tried to foreclose, but senior lenders challenged priority. That slowed the process and led to a long dispute.[9]

When mezzanine financing helps and when it adds risk

Mezzanine financing tends to work best when a deal has a believable plan to add value and senior debt can't go far enough on leverage. Put simply, mezz works when the expected return is higher than the blended cost of debt. It becomes a problem on stabilized, lower-return deals, where extra leverage can turn a small miss into a major hit.

At 80% to 85% combined leverage, even a 15% to 20% drop in value can wipe out the equity. On top of that, most mezz loans are interest-only and come with a balloon payment at maturity. If NOI growth stalls, lease-up takes longer than expected, or cap rates move the wrong way, a refinance can stop penciling out.

That's why conservative cap rate assumptions and stress-tested NOI projections matter so much. They're often the line between a deal that stays intact and one that starts to crack.

Conclusion: Key lessons from 5 mezzanine financing case studies in CRE

These five cases land in the same place, even though they get there in different ways. In each one, mezzanine financing filled the gap that senior debt wouldn't cover. But the deal terms didn't move just because a loan was labeled "mezzanine." They moved based on the asset's risk.

That shows up clearly in pricing and structure. Multifamily and industrial deals came in the tightest. Hotel deals priced the highest. Office and retail landed in the middle. Hotel transactions also brought the most moving parts, including franchisor comfort letters, standstill periods of 90 to 180 days, and added renovation risk. [10][1]

Price isn't the whole story. Structure matters just as much. Stuyvesant Town-Peter Cooper Village is a clear example of what can happen when intercreditor language is weak: a default can spiral into litigation. [9]

PIK interest can help in the near term, especially during lease-up or renovation, because it reduces pressure on current cash flow. The catch is that it builds a bigger payoff later. If NOI and valuation don't improve the way the model assumes, that added balance can make refinancing hard. That's why the exit needs to be stress-tested at least 200 basis points above current rates. [1][6]

The decision rule is simple: if stabilized NOI can't carry full debt service, including accrued PIK, walk away from the structure before maturity risk shows up. Mezzanine debt only works when the exit can clear both layers of debt. [1]

FAQs

When does mezzanine financing make sense in CRE?

Mezzanine financing fits when there’s a gap between senior debt and sponsor equity. That usually happens when the senior lender won’t go high enough on leverage for the deal to work on its own.

You’ll see it a lot in ground-up development, value-add multifamily, and transitional bridge takeouts, where sponsors want to push total leverage to around 80% to 90%.

It can also help sponsors:

- Cut the amount of cash equity they need to put in

- Keep more of their promote structure in place

- Pay for capital items a senior lender may not fund, like improvements or tenant build-outs

In plain English, mezzanine financing helps fill the part of the stack that senior debt leaves behind.

How do you know if a mezzanine exit is realistic?

Project the senior debt refinance proceeds at the mezzanine maturity date to make sure they’re enough to pay off the mezzanine loan.

A realistic exit starts with a stabilized NOI that can support a takeout lender’s DSCR and LTV limits. Then push on the numbers a bit. Stress-test cash flow for interest rate swings and cap rate expansion so you can see if the exit still holds up in different market scenarios.

What risks matter most by property type?

Risks change based on the property type and the business plan.

Multifamily tends to be the steadiest option, especially when the asset is already stabilized. The picture shifts with ground-up development, which is usually more volatile. Cost overruns, delays, and budget shortfalls often create the need for mezzanine financing.

Hospitality deals with renovation costs, downtime, and refinancing risk. Retail and office often depend on tenant improvement demands, while industrial usually sits somewhere between multifamily and office on the risk spectrum.

Across every property type, technical triggers can pose the biggest threat if they cause a loss of control.