Ultimate Guide to Historic Tax Credits for CRE

Historic Tax Credits (HTCs) offer a 20% federal tax credit on qualifying expenses for restoring certified historic buildings. This program, active since 1976, has preserved over 43,000 structures and driven $144.6 billion in private investments. It applies to income-producing properties like offices, rental housing, and retail spaces, but not private residences.

Key Points:

- Eligibility: Buildings must be certified historic structures, either individually listed or contributing to a historic district.

- Qualified Rehabilitation Expenditures (QREs): Covers costs like structural repairs, architectural fees, and construction-period taxes, but excludes land purchase, enlargements, and landscaping.

- Application Process: A 3-step system (Parts 1, 2, and 3) ensures compliance with historic preservation standards.

- Financial Benefits: Credits are claimed over five years and can be paired with state-level programs or other incentives like Low-Income Housing Tax Credits.

Developers can combine HTCs with other tools to make restoration projects financially feasible, while syndication allows unused credits to generate upfront capital. Proper planning and compliance are critical to maximizing returns and avoiding penalties. Utilizing a comparables module can help benchmark these returns against market standards.

Eligibility Requirements for Historic Tax Credits

Property Eligibility Criteria

To qualify for the 20% federal historic tax credit, a property must be certified as a historic structure by the National Park Service (NPS). This means the building must either be listed individually in the National Register of Historic Places or identified as "contributing" to a registered historic district [4][7]. Buildings outside a district's "period of significance" - like a 1950s office building in an 1800s residential district - do not qualify [4][7].

The credit applies strictly to "buildings" as defined by Treasury Regulation 1.48-1(e), which includes enclosed structures with roofs. Other categories listed in the National Register, such as bridges, objects, or sites, are not eligible [4][7]. Additionally, properties must serve an income-producing purpose, such as commercial, industrial, agricultural, or rental residential use. Portions of mixed-use properties, like a home office, may also qualify [4][7].

Before rehabilitation begins, the building must retain enough of its historic fabric. If non-historic materials, like modern siding, cover the structure, these must be removed to confirm that sufficient original materials remain [4][7]. The program aims to preserve authentic historic buildings, not to create replicas that mimic historic appearances.

Project Eligibility Guidelines

After confirming property eligibility, the rehabilitation project itself must meet specific cost and preservation benchmarks.

The project must pass the substantial rehabilitation test, which requires that rehabilitation expenses exceed the greater of $5,000 or the building's adjusted basis within a 24-month period (or a 60-month period for phased projects) [4][8]. Adjusted basis is calculated as the purchase price minus land value and depreciation, plus any previous capital improvements.

For instance, the National Park Service provides an example where Mr. Jones purchased a Victorian rental cottage for $150,000, with $70,000 attributed to the land. After accounting for $41,000 in depreciation and $1,500 in prior improvements, the adjusted basis is $40,500. A $50,000 rehabilitation project, which exceeds the adjusted basis, qualifies for the 20% credit, resulting in $10,000 [4][7].

All rehabilitation work must adhere to the Secretary of the Interior's Standards for Rehabilitation, which are ten principles aimed at preserving a building's historic character. These standards emphasize using the least invasive methods for cleaning and repairs, explicitly prohibiting harmful techniques like sandblasting [5][6]. To avoid disqualifying expenses, the NPS strongly advises submitting Part 2 (Description of Rehabilitation) before starting any construction [8]. Early consultation with the State Historic Preservation Office (SHPO) is also recommended to ensure the project complies with all necessary requirements.

sbb-itb-df8a938

Understanding Qualified Rehabilitation Expenditures (QREs)

What Are QREs?

After determining that a property and project meet eligibility requirements, the next step is understanding and calculating Qualified Rehabilitation Expenditures (QREs). This process is key to meeting rehabilitation standards and claiming the federal historic tax credit.

QREs refer to the capitalized costs directly tied to rehabilitating a certified historic building [9][8]. These include hard costs, such as structural components and essential building systems, as well as certain soft costs, like architectural and engineering fees, developer fees, construction management costs, and construction-period interest and taxes [9][1].

However, not every expense qualifies. For example:

- Acquisition costs, such as the building's purchase price or the land it sits on, are excluded [9][1].

- Costs for enlargements that increase the structure's total volume are ineligible [9][1].

- Expenses for related facilities - like sidewalks, parking lots, or landscaping - do not count [9][1].

- Personal property, such as non-permanent furnishings or equipment, is also excluded.

"Generally, costs directly related to repairing and improving the historic building's structural and architectural features will qualify" [1].

Another important distinction: while construction-period interest qualifies as a QRE, interest on acquisition loans does not [11][8][1]. To avoid surprises, it's best to submit Part 2 of the application before construction begins to confirm that planned expenditures are eligible [8][1].

With a clear definition of QREs, the next step is to determine the value of the Historic Tax Credit (HTC).

Calculating the HTC Value

The federal historic tax credit is calculated as 20% of your total QREs [9][8][1]. For example, The Sherbert Group demonstrated this in January 2026 with a hypothetical adaptive reuse project:

- A developer purchased a historic building for $300,000, with $50,000 attributed to the land, leaving an adjusted basis of $250,000.

- The developer then spent $400,000 on rehabilitation within a 24-month measuring period.

- Because the $400,000 in QREs exceeded the $250,000 adjusted basis, the project qualified for an $80,000 HTC.

The $80,000 credit is claimed over five years, with $16,000 applied annually once the building is placed in service [10].

"Certified historic buildings continue to qualify for a credit equal to 20% of QREs, but now the credit must be claimed ratably over a five-year period" [11].

It’s important to note that taxpayers must reduce the QRE basis by any additional first-year (bonus) depreciation taken. In many cases, opting out of bonus depreciation can help maximize the 20% tax credit [8]. Additionally, the HTC can generally only be claimed if the straight-line method of depreciation is used for the building [1].

Historic Preservation Tax Incentives Program Overview

How to Apply for Historic Tax Credits

Historic Tax Credits 3-Part Application Process Timeline

Once you understand how to define and calculate Qualified Rehabilitation Expenditures (QREs), the next step is diving into the application process for historic tax credits.

3-Part Application Process

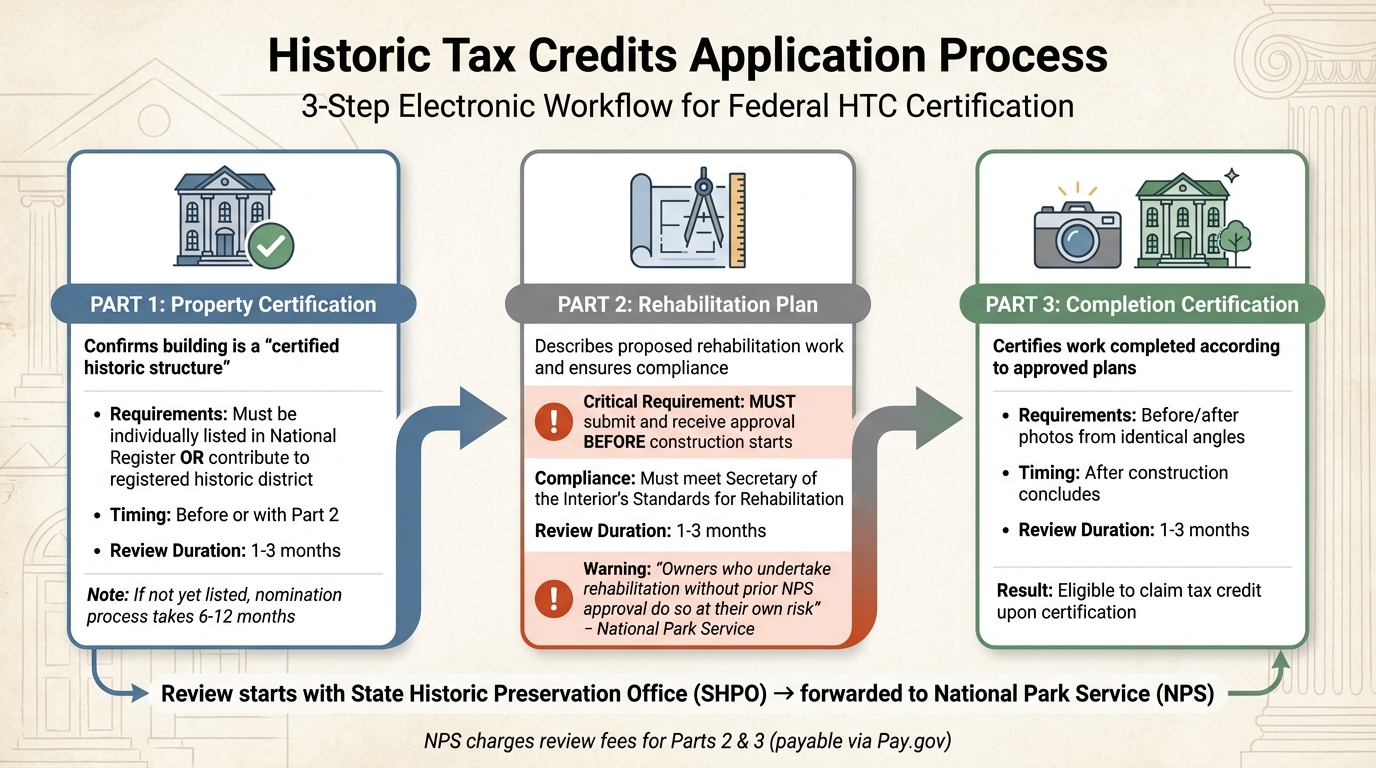

The process for applying for historic tax credits follows a three-step, fully electronic workflow (introduced in June 2023).

Part 1: This step confirms that your property qualifies as a "certified historic structure." To meet this requirement, the building must either be individually listed in the National Register of Historic Places or contribute to a registered historic district. You’ll need to provide documentation of the building’s historical significance and current appearance. If your property isn’t listed yet, you’ll need to go through a nomination process, which typically takes 6 to 12 months.

Part 2: Here, you’ll describe the building’s current condition and outline the rehabilitation work you plan to undertake. It’s critical to submit this part and receive approval before starting any construction. This ensures your project complies with the Secretary of the Interior’s Standards for Rehabilitation, which is essential for maintaining eligibility for the tax credit.

"Owners who undertake rehabilitation projects without prior NPS approval do so at their own risk." – National Park Service

Part 3: This final step certifies that the rehabilitation work has been completed according to the approved plans from Part 2. You’ll need to provide "before" and "after" photos taken from identical angles to demonstrate compliance. Once this certification is issued, you’re eligible to claim the tax credit.

The process starts with your State Historic Preservation Office (SHPO), which reviews your submission before forwarding it to the National Park Service (NPS) for final certification. Keep in mind that the NPS charges review fees for Parts 2 and 3, payable through Pay.gov.

| Application Part | Purpose | Timing | Review Duration |

|---|---|---|---|

| Part 1 | Confirms the building is a "certified historic structure" | Before or with Part 2 | 1–3 months |

| Part 2 | Describes proposed rehabilitation work and ensures compliance | Before construction starts | 1–3 months |

| Part 3 | Certifies that work was completed as proposed | After construction concludes | 1–3 months |

Compliance and Reporting Requirements

Once your project is certified, a five-year compliance period begins. During this time, the property must remain an income-producing, depreciable asset under the same ownership. If you sell or transfer the property within the first year, you’ll face a 100% recapture of the tax credit. This recapture rate decreases by 20% annually over the five-year period.

Throughout the project, it’s crucial to maintain thorough records of all QREs. These records are necessary when claiming the credit using IRS Form 3468. This form requires your NPS-assigned project number and the certification date. Most developers file this form within 1 to 3 months after receiving Part 3 approval.

If your project plans change during construction, you’ll need to submit an Amendment/Advisory Determination form as soon as possible. Each year, about 1,200 projects are approved for the federal historic tax credit program, driving nearly $6 billion in private investments toward historic preservation [1].

With the application process and compliance requirements in place, the next section will explore how to integrate these credits into your commercial real estate financing strategy.

Maximizing Financial Benefits of HTCs

Monetizing Historic Tax Credits

The federal Historic Tax Credit (HTC) allows developers to reduce their federal income taxes by 20% of Qualified Rehabilitation Expenditures (QREs). This credit can be directly applied to federal tax liabilities, with the option to carry it back one year or forward for up to 20 years. This flexibility gives developers plenty of time to take full advantage of the benefit [14][16].

For those who may not be able to use the credits fully, syndication provides a way to turn future credits into immediate equity. By partnering with a third-party investor - typically a bank or corporation - developers can secure upfront capital in exchange for the tax credits. On average, this arrangement yields around $0.70 for every dollar of HTC allocated [16].

"The Historic Tax Credit program is important to the firm, and most of our investments of tax credit for historic preservation are in areas that are changing, developing or undergoing some renaissance" [13].

Federal investors are required to remain partners for at least five years after construction to avoid credit recapture. Some state programs allow certificated credits to be bought and sold directly, while others follow a partnership model similar to the federal program. These options provide flexibility for developers to incorporate HTCs into broader financing plans.

Integrating HTCs Into CRE Financing

Developers often combine HTCs with other tax credits to bridge funding gaps. The 20% federal HTC can be paired with Low-Income Housing Tax Credits (LIHTC) for multifamily housing projects or New Markets Tax Credits (NMTC) for commercial developments in low-income areas. If a project is located in a historic district within a Qualified Opportunity Zone, developers can also leverage capital gains tax deferrals alongside HTC benefits [12].

It’s important to avoid aggressive cost segregation studies on HTC projects. Accelerating depreciation on building components can reduce the total QREs, which lowers the value of the tax credit. Opting for straight-line depreciation helps preserve the credit’s value. Additionally, bridge financing can help cover construction costs until the credits are fully realized over the five-year claim period [1].

State‑Level HTC Programs

As of 2024, 39 states offer their own historic tax credit programs [15]. These state-level incentives complement federal credits, further enhancing project returns. For example, Connecticut provides a base 25% tax credit on QREs, which increases to 30% if the project is located in a federally designated Opportunity Zone or includes affordable housing (with at least 20% of rental units or 10% of for-sale units qualifying as affordable). However, the state caps annual reservations at $31.7 million, with a per-project limit of $4.5 million [19].

Wisconsin offers a 20% state tax credit for QREs exceeding $50,000 on certified historic structures [18]. By stacking state and federal credits, developers can significantly boost their project returns. The federal HTC program alone has driven over $235 billion in private investment, generating approximately $1.20 in tax revenue for every $1.00 invested [15].

Using CoreCast and Custom Analysis for HTC Projects

Using CoreCast for HTC Modeling

CoreCast's Underwriter Module simplifies financial modeling for historic tax credit (HTC) projects. It connects seamlessly with accounting systems like QuickBooks, RealPage, and Buildium to automate the tracking of qualified rehabilitation expenditures (QREs) [21].

The platform uses machine learning to provide performance projections and conduct stress testing [21][20]. It also handles phased substantial rehabilitation tests to ensure compliance with National Park Service (NPS) standards [16]. Meanwhile, the Pipeline Tracker keeps tabs on compliance deadlines and offers real-time updates on deal progress, from initial evaluation to final disposition [21].

"With the Pipeline Tracker, we reduced deal slippage by 30% over two quarters." – Director of Acquisitions, REIT [21]

CoreCast's Reports module enables users to create branded, customizable reports. These reports clearly outline how HTCs impact a project's capital stack and returns, making them invaluable when presenting to tax credit syndicators and equity partners. This is particularly critical for explaining the project's five-year compliance period and its income-generating potential [21]. CoreCast is available at approximately $105 per user per month [21]. For more detailed project insights, additional analysis services can complement the platform's features.

Custom Analysis Services for HTC Projects

While CoreCast automates much of the modeling process, custom analysis services provide an extra layer of precision for HTC project optimization. The Fractional Analyst service offers on-demand expertise, helping developers maximize HTC benefits in commercial real estate (CRE) projects. This service is particularly helpful when internal teams are stretched thin or when projects involve complex tax credit combinations, such as integrating HTCs with Low-Income Housing Tax Credits or New Markets Tax Credits. The team also delivers tailored Excel models for both multifamily and commercial properties, designed to reflect HTC-specific debt and equity structures [17].

The service has supported a wide range of clients and maintains an extensive library of financial models [17]. It is particularly effective for optimizing complex tax credit structures, ensuring accurate basis adjustments and depreciation schedules to boost project returns. Custom research can also model scenarios that address credits being claimed ratably over five years, along with the property's adjusted basis reduction [1]. This level of detail helps developers sidestep common pitfalls, such as overly aggressive cost segregation studies that may reduce QREs and, ultimately, the value of the credits [1].

Conclusion

Historic tax credits (HTCs) have been a powerful tool for financing real estate projects while preserving historic structures. Since the program's inception in 1976, it has helped restore over 43,000 buildings and attracted $144.6 billion in private investments. Today, it continues to generate nearly $6 billion annually across approximately 1,200 approved projects [2][1].

To qualify, your building must be a certified historic structure, the project must meet the substantial rehabilitation test, and Qualified Rehabilitation Expenditures (QREs) must be accurately calculated. The 20% federal credit applies to both hard costs, like structural repairs, and soft costs, such as architectural fees [1][3][8]. However, improper cost segregation or bonus depreciation can reduce QRE values, potentially lowering the credit amount [1][8].

HTCs become even more impactful when combined with other financing strategies. By layering federal credits with state-level programs - offered in 39 states as of 2024 - and pairing them with incentives like Low-Income Housing Tax Credits, New Markets Tax Credits, or Opportunity Zone benefits, you can significantly improve project returns [1][2][3]. Engaging early with your State Historic Preservation Office is crucial to ensure compliance with the Secretary of the Interior's Standards and avoid costly setbacks [1][8].

The credit is claimed over five years, and the property must remain income-producing under the same ownership to avoid recapture penalties [1][22]. Leveraging advanced tools like CoreCast and insights from platforms such as The Fractional Analyst can help you optimize your historic rehabilitation investments and maximize the benefits of HTCs.

FAQs

How do I know if my building is “certified historic”?

A building earns the title of "certified historic" if it is included in the National Register of Historic Places or recognized as a contributing structure within a registered historic district. Beyond that, the National Park Service must confirm that the building has preserved its historic integrity.

What costs qualify as QREs (and what don’t)?

Qualified rehabilitation expenditures (QREs) cover costs that are properly capitalized for the rehabilitation of a certified historic building. This includes work like renovation, restoration, or reconstruction that aligns with the building's historic character. To qualify, these expenses must directly relate to the building's structural components. However, costs associated with enlarging the building or new construction are not eligible.

How can I monetize HTCs if I can’t use all the credits?

If you find yourself unable to use all your historic tax credits (HTCs), there’s an option to monetize them by selling or transferring the unused portion. Programs such as the Texas Historic Preservation Tax Credit Program allow you to sell these credits at their market value. On a federal level, unused credits offer flexibility - they can be carried back one year, carried forward for up to 20 years, or sold/transferred to investors or eligible entities.